Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Nelnet (NYSE: NNI) and its peers.

Consumer finance companies provide loans and credit products to individuals. Growth drivers include increasing consumer spending, financial inclusion initiatives in developing markets, and digital lending platforms reducing distribution costs. Challenges include credit risk during economic downturns, regulatory scrutiny of lending practices, and intensifying competition from traditional banks and fintech firms offering innovative credit solutions.

The 20 consumer finance stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 0.7% above.

Luckily, consumer finance stocks have performed well with share prices up 13.1% on average since the latest earnings results.

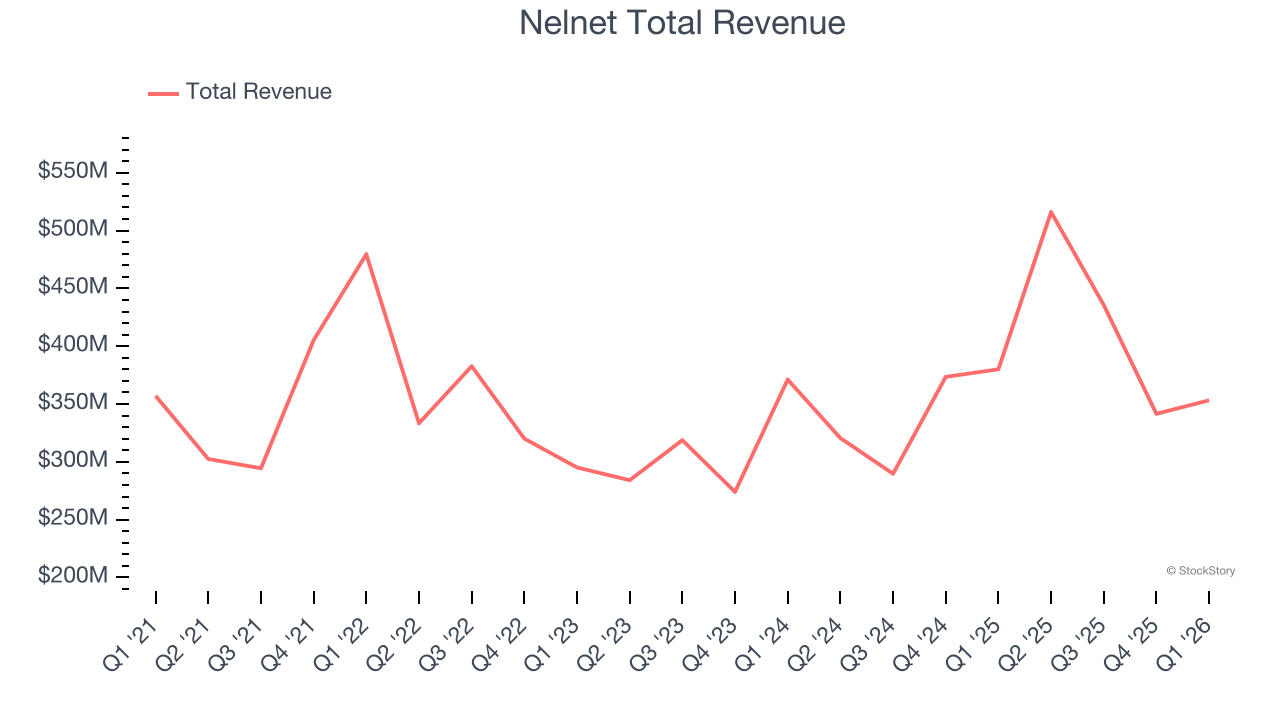

Weakest Q1: Nelnet (NYSE: NNI)

Starting as a student loan servicer in the 1970s and evolving through the changing landscape of education finance, Nelnet (NYSE: NNI) provides student loan servicing, education technology, payment processing, and banking services while managing a portfolio of education loans.

Nelnet reported revenues of $353.2 million, down 7.1% year on year. This print fell short of analysts’ expectations by 20.4%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ net interest income and EPS estimates.

"We're off to a strong start in 2026, with every business segment performing at a high level," said Jeff Noordhoek, chief executive officer of Nelnet.

Nelnet delivered the weakest performance against analyst estimates of the whole group. The market seems disappointed with the results as the stock is down 6.1% since reporting and currently trades at $132.78.

Is now the time to buy Nelnet? Access our full analysis of the earnings results here, it’s free.

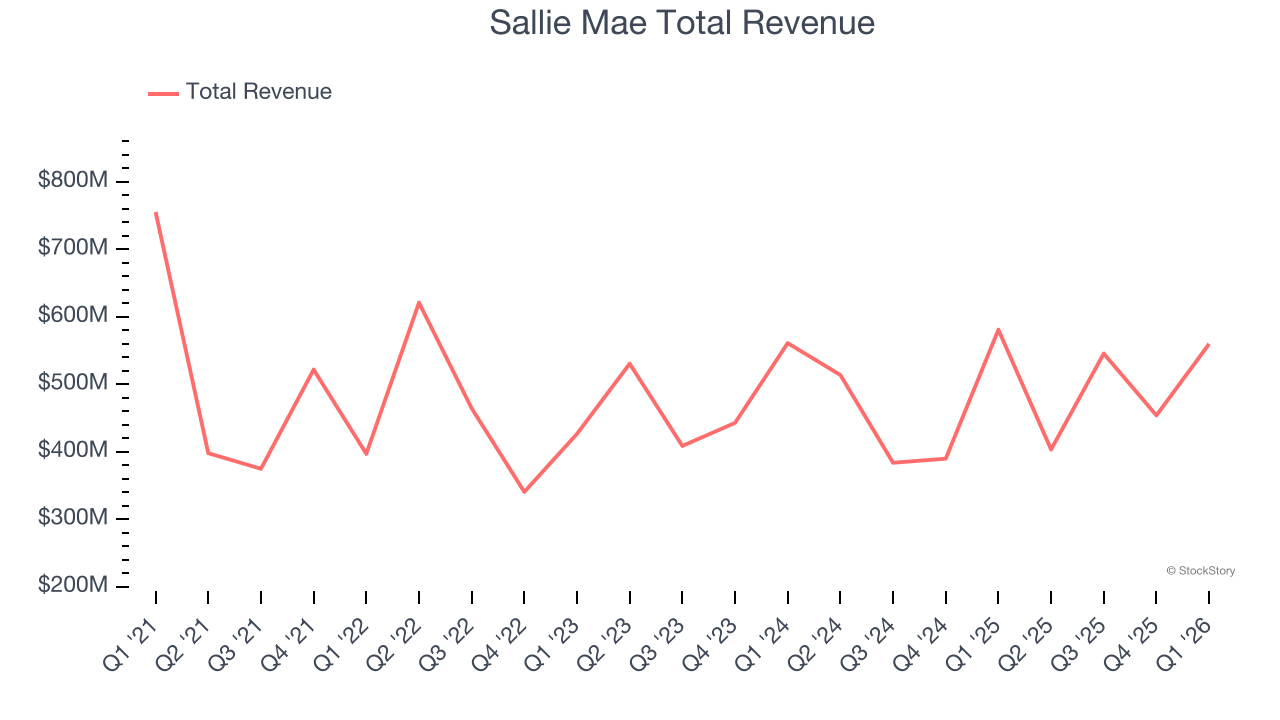

Best Q1: Sallie Mae (NASDAQ: SLM)

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ: SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

Sallie Mae reported revenues of $560 million, down 3.6% year on year, outperforming analysts’ expectations by 3.9%. The business had a stunning quarter with a beat of analysts’ EPS estimates and full-year EPS guidance exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 6.5% since reporting. It currently trades at $24.94.

Is now the time to buy Sallie Mae? Access our full analysis of the earnings results here, it’s free.

Credit Acceptance (NASDAQ: CACC)

Founded in 1972 by Donald Foss to serve customers overlooked by traditional lenders, Credit Acceptance (NASDAQ: CACC) provides auto financing solutions that enable car dealers to sell vehicles to consumers with limited or impaired credit histories.

Credit Acceptance reported revenues of $406 million, up 1.4% year on year, falling short of analysts’ expectations by 13.1%. It was a softer quarter as it posted a significant miss of analysts’ EBITDA estimates.

Interestingly, the stock is up 22.9% since the results and currently trades at $645.90.

Read our full analysis of Credit Acceptance’s results here.

Atlanticus Holdings (NASDAQ: ATLC)

Using data analytics to serve the millions of Americans with less-than-perfect credit scores, Atlanticus Holdings (NASDAQ: ATLC) provides technology and services that help lenders offer credit products to consumers often overlooked by traditional financing providers.

Atlanticus Holdings reported revenues of $556.8 million, up 87.2% year on year. This print lagged analysts’ expectations by 7.6%. Overall, it was a mixed quarter for the company.

Atlanticus Holdings achieved the fastest revenue growth among its peers. The stock is up 24.1% since reporting and currently trades at $97.21.

Read our full, actionable report on Atlanticus Holdings here, it’s free.

FirstCash (NASDAQ: FCFS)

Offering a financial lifeline to the unbanked and credit-constrained since 1988, FirstCash (NASDAQ: FCFS) operates pawn stores across the U.S. and Latin America while also providing retail point-of-sale payment solutions for credit-constrained consumers.

FirstCash reported revenues of $1.05 billion, up 25.7% year on year. This number beat analysts’ expectations by 4.8%. Overall, it was an exceptional quarter as it also recorded a solid beat of analysts’ EBITDA estimates and a beat of analysts’ EPS estimates.

The stock is up 4.1% since reporting and currently trades at $221.00.

Read our full, actionable report on FirstCash here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.