Starbucks has had an impressive run over the past six months as its shares have beaten the S&P 500 by 9.9%. The stock now trades at $102.24, marking a 17.9% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Starbucks, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Starbucks Not Exciting?

Despite the momentum, we’re cautious about Starbucks. Here are three reasons why there are better opportunities than SBUX, plus one stock we’d rather own.

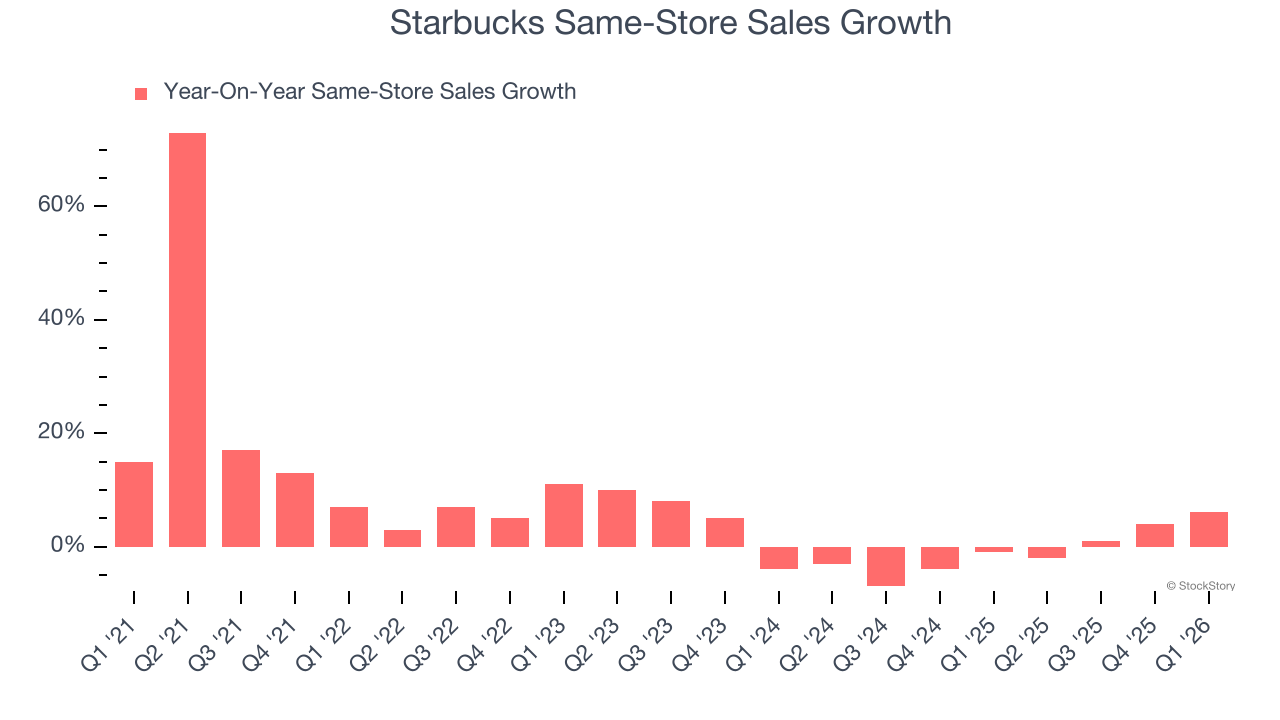

1. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is an industry measure of whether revenue is growing at existing restaurants, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Starbucks’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Starbucks’s revenue to drop by 2.8%. This projection is underwhelming and suggests its menu offerings will face some demand challenges.

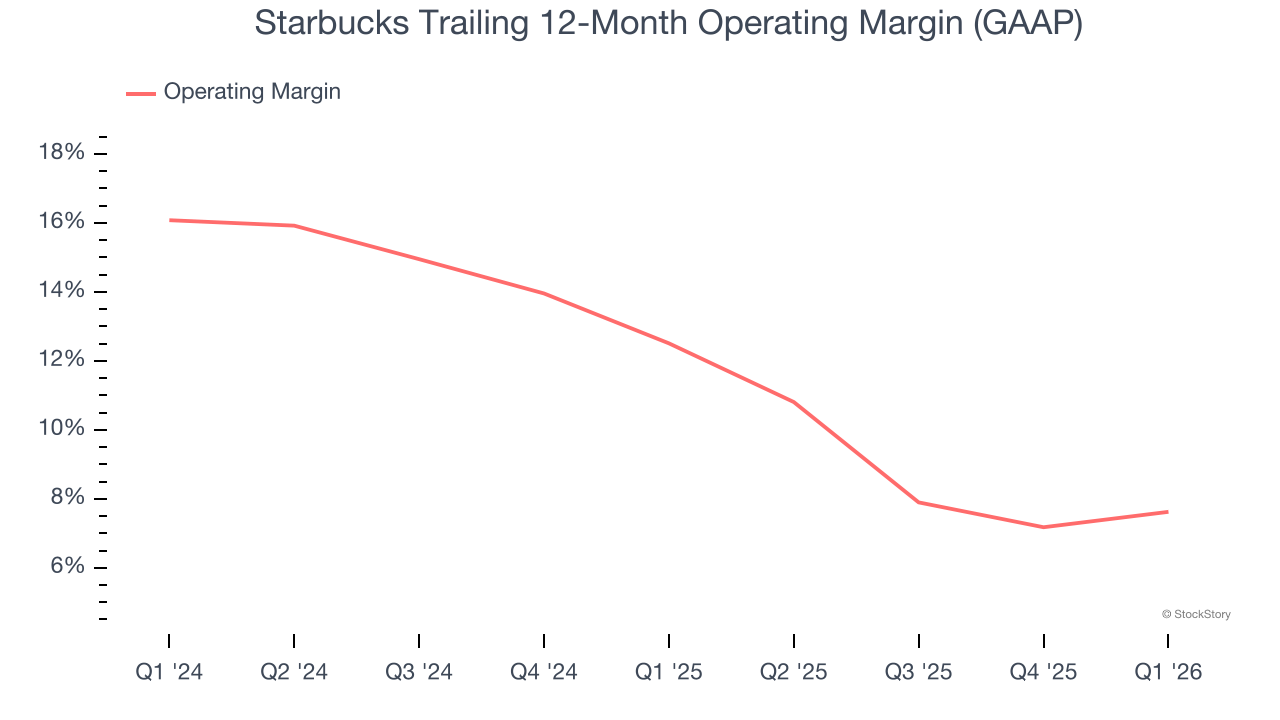

3. Shrinking Operating Margin

Operating margin is an important measure of profitability for restaurants as it accounts for all expenses keeping the business in motion, including food costs, wages, rent, advertising, and other administrative costs.

Looking at the trend in its profitability, Starbucks’s operating margin decreased by 4.9 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 7.6%.

Final Judgment

Starbucks isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 38.5× forward P/E (or $102.24 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at a dominant aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Starbucks

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.