Over the past six months, Western Alliance Bancorporation’s stock price fell to $81.50. Shareholders have lost 6.7% of their capital, which is disappointing considering the S&P 500 has climbed by 8.4%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Western Alliance Bancorporation, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Western Alliance Bancorporation Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons we avoid WAL, plus one stock we’d rather own.

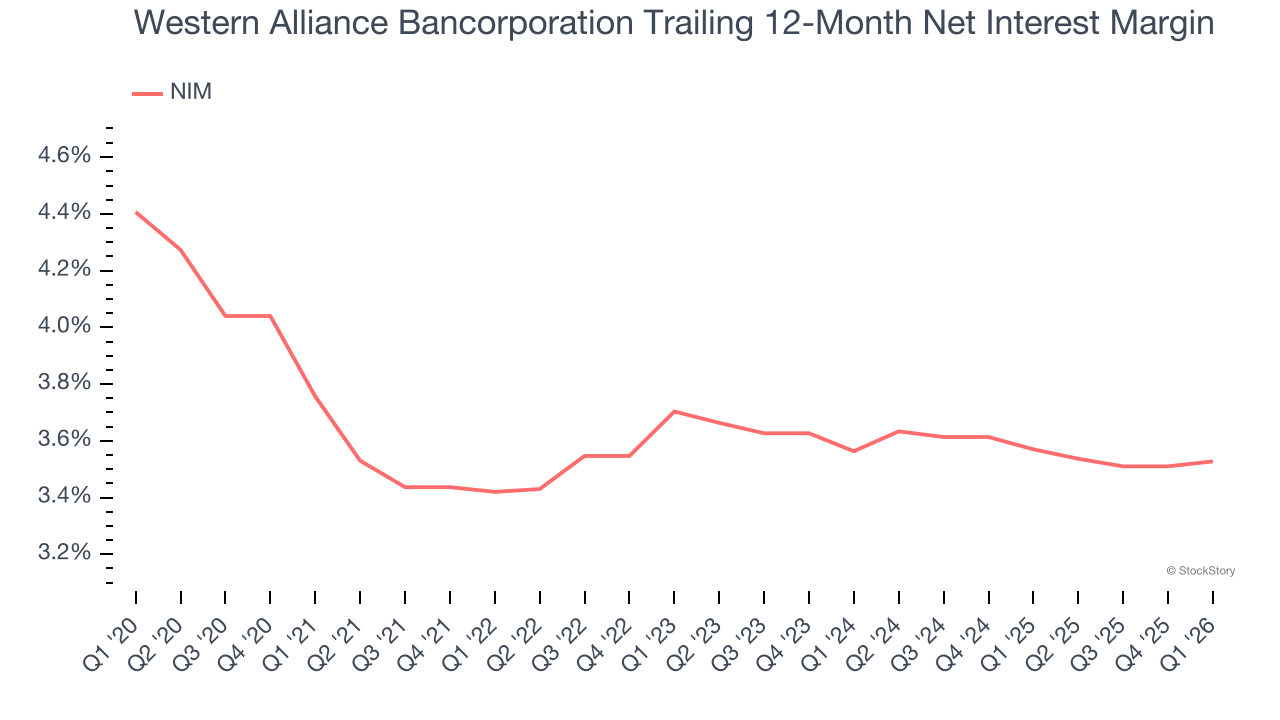

1. Net Interest Margin Dropping

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It’s one of the most important metrics to track because it shows how a bank’s loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Western Alliance Bancorporation’s net interest margin averaged 3.5%. However, its margin contracted by 3.6 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Western Alliance Bancorporation either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

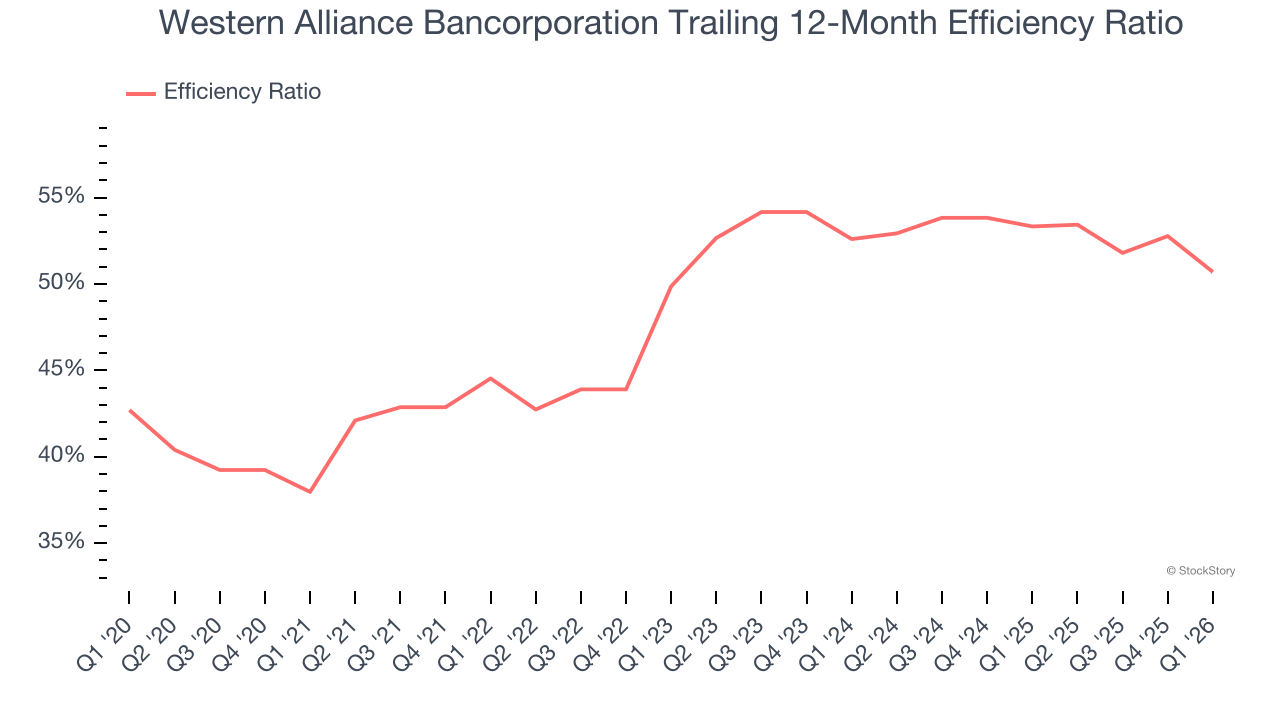

2. Efficiency Ratio Expected to Falter

Topline growth alone doesn’t tell the complete story — the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Markets emphasize efficiency ratio trends over static measurements, recognizing that revenue compositions drive different expense bases. Lower efficiency ratios signal superior performance by indicating that banks are controlling costs effectively relative to their income.

For the next 12 months, Wall Street expects Western Alliance Bancorporation to become less profitable as it anticipates an efficiency ratio of 56.7% compared to 50.7% over the past year.

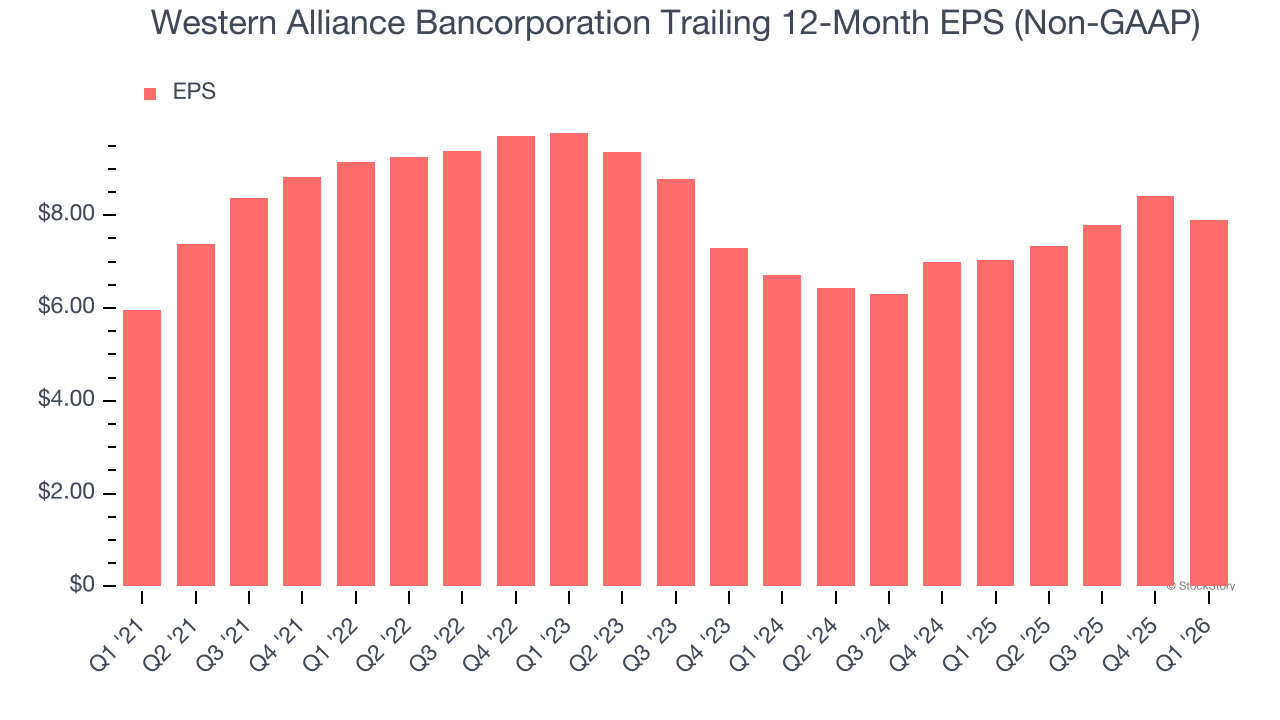

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Western Alliance Bancorporation’s EPS grew at a weak 5.8% compounded annual growth rate over the last five years, lower than its 23.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Western Alliance Bancorporation isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 1.1× forward P/B (or $81.50 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re fairly confident there are better investments elsewhere. We’d recommend looking at one of our top digital advertising picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.