UL Solutions has had an impressive run over the past six months as its shares have beaten the S&P 500 by 5.5%. The stock now trades at $87.75, marking a 13.8% gain. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy ULS? Find out in our full research report, it’s free.

Why Does UL Solutions Spark Debate?

Founded in 1894 as a response to the growing dangers of electricity in American homes and businesses, UL Solutions (NYSE: ULS) provides testing, inspection, and certification services that help companies ensure their products meet safety, security, and sustainability standards.

Two Things to Like:

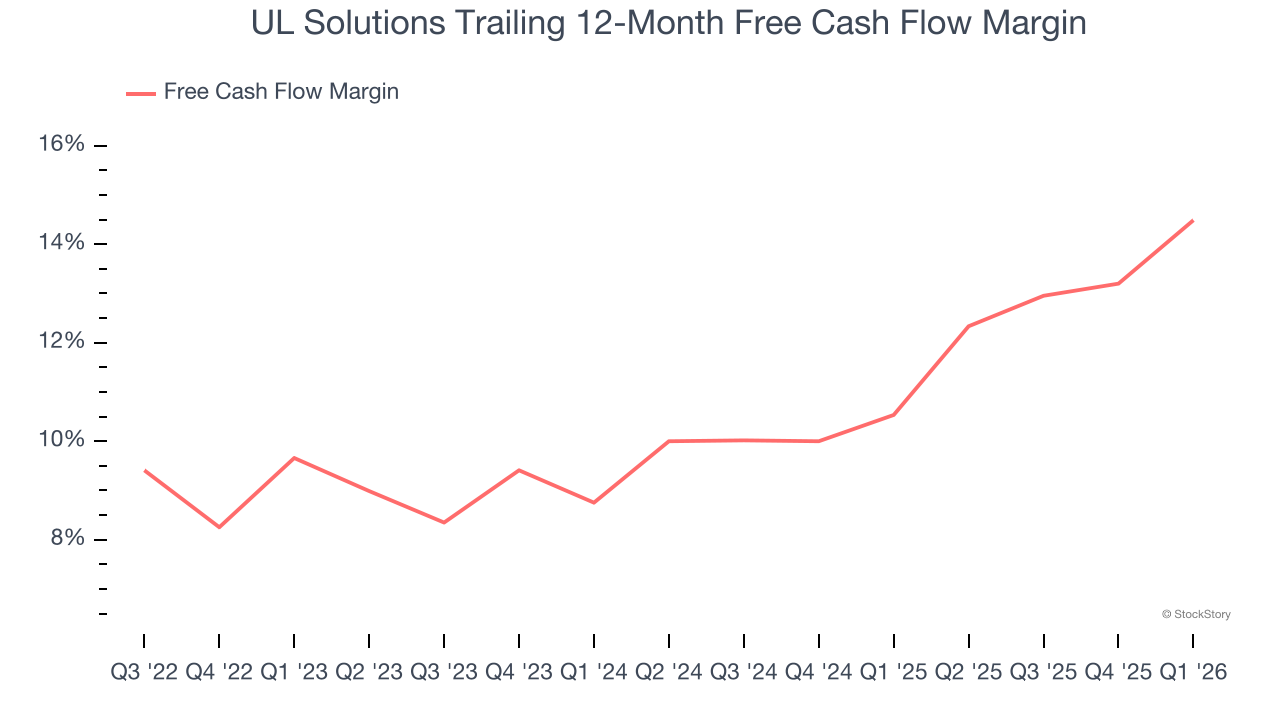

1. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, UL Solutions’s margin expanded by 5.3 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell. UL Solutions’s free cash flow margin for the trailing 12 months was 14.5%.

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

UL Solutions’s four-year average ROIC was 27.8%, placing it among the best business services companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to Be Careful:

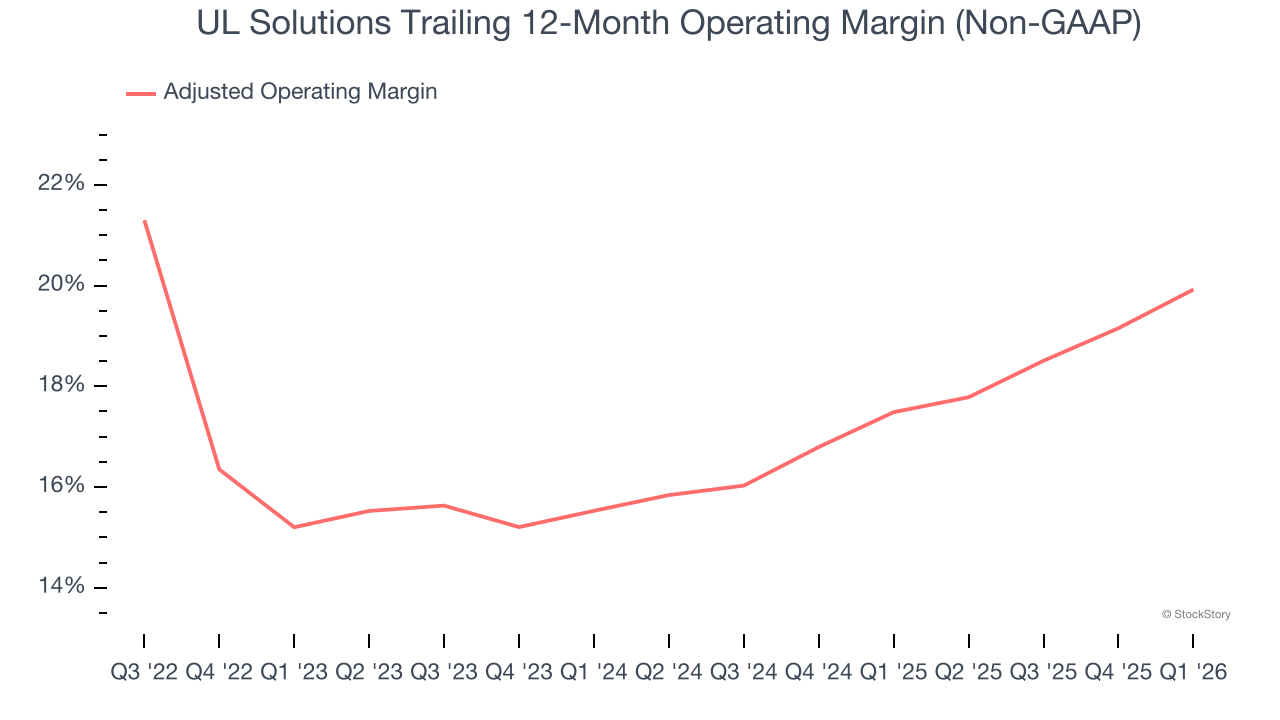

Shrinking Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

Looking at the trend in its profitability, UL Solutions’s adjusted operating margin decreased by 6.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 19.9%.

Final Judgment

UL Solutions’s positive characteristics outweigh the negatives, and with its shares beating the market recently, the stock trades at 37.3× forward P/E (or $87.75 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+271% between June 2020 and June 2025). Find your next big winner with StockStory today.