USANA currently trades at $18.88 per share and has shown little upside over the past six months, posting a small loss of 4.1%. The stock also fell short of the S&P 500’s 9% gain during that period.

Is now the time to buy USANA, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is USANA Not Exciting?

We’re cautious about USANA. Here are three reasons why USNA doesn’t excite us, plus one stock we’d rather own.

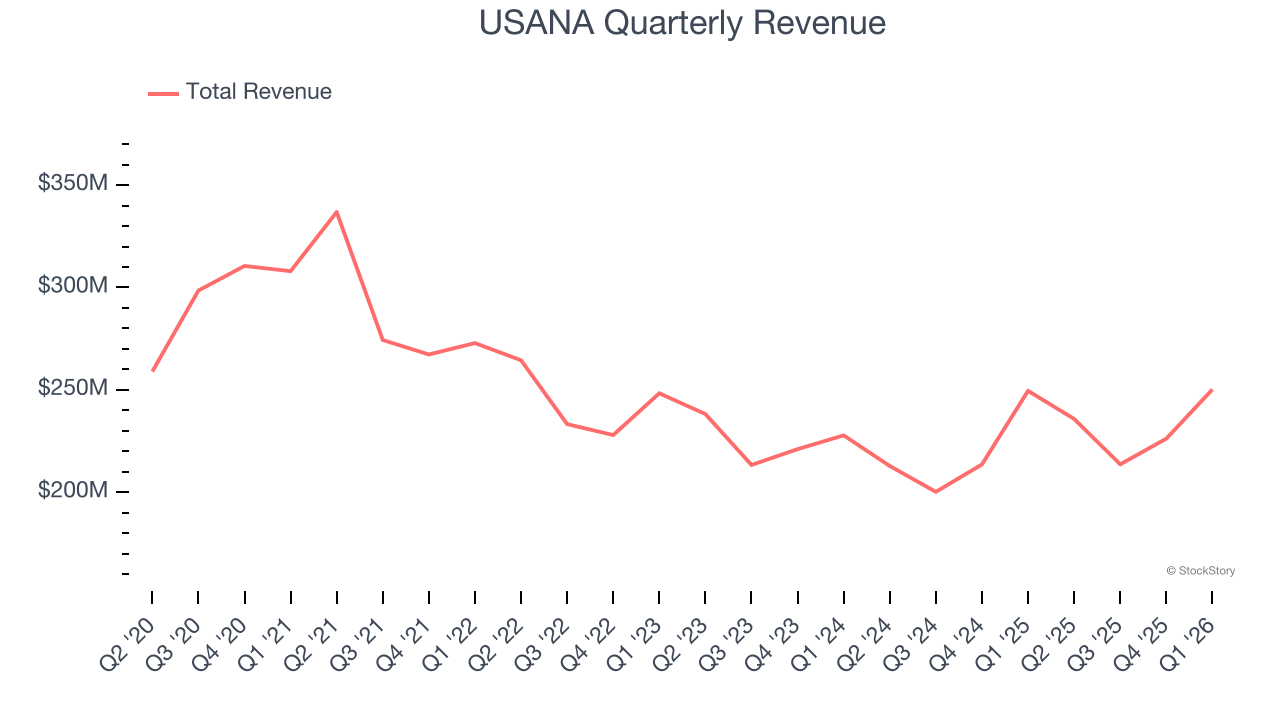

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. USANA’s demand was weak over the last three years as its sales fell at a 1.7% annual rate. This was below our standards and signals it’s a lower quality business.

2. Fewer Distribution Channels Limit Its Ceiling

With $925.9 million in revenue over the past 12 months, USANA is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

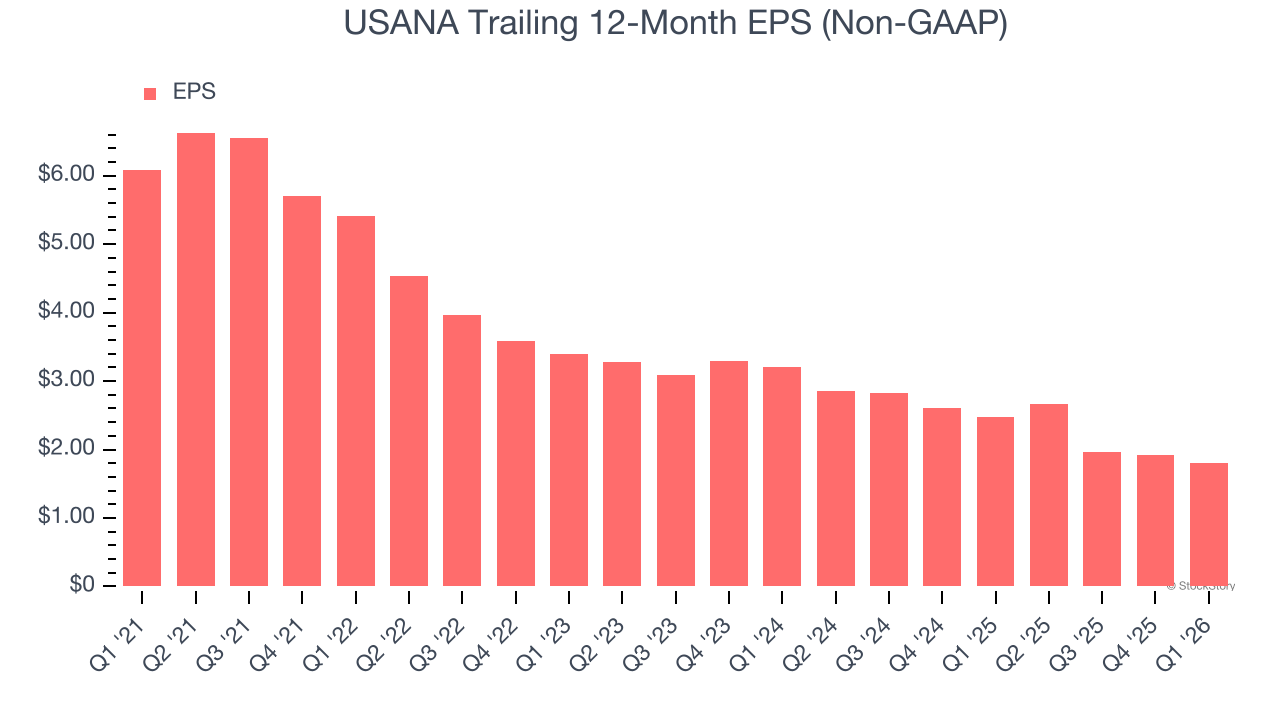

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for USANA, its EPS declined by 19% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

USANA isn’t a terrible business, but it doesn’t pass our quality test. With its shares trailing the market in recent months, the stock trades at 8.8× forward P/E (or $18.88 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re fairly confident there are better stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.