Over the past six months, First Busey has been a great trade, beating the S&P 500 by 5.4%. Its stock price has climbed to $28.23, representing a healthy 14.5% increase. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy First Busey, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is First Busey Not Exciting?

We’re happy investors have made money, but we’re sitting this one out for now. Here are three reasons you should be careful with BUSE, plus one stock we’d rather own.

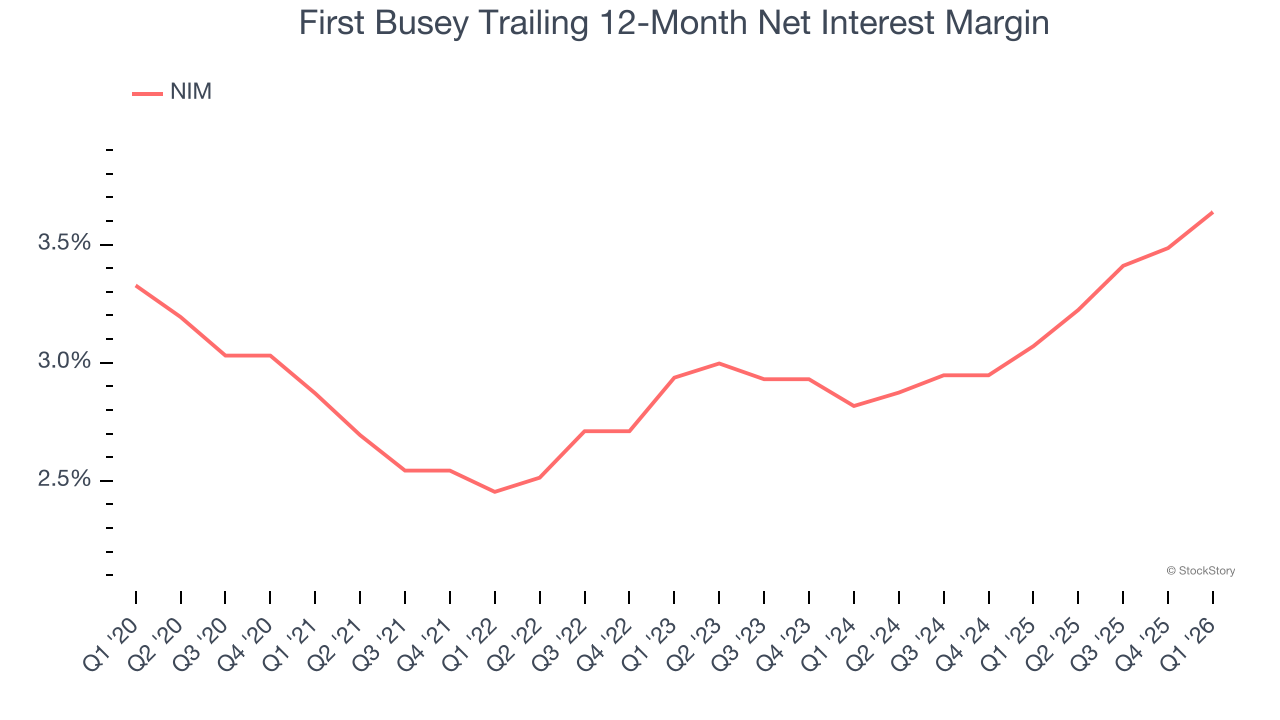

1. Low Net Interest Margin Hinders Flexibility

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently it can generate income from its core lending activities.

Over the past two years, we can see that First Busey’s net interest margin averaged a subpar 3.4%. This metric is well below other banks, signaling its loans aren’t very profitable.

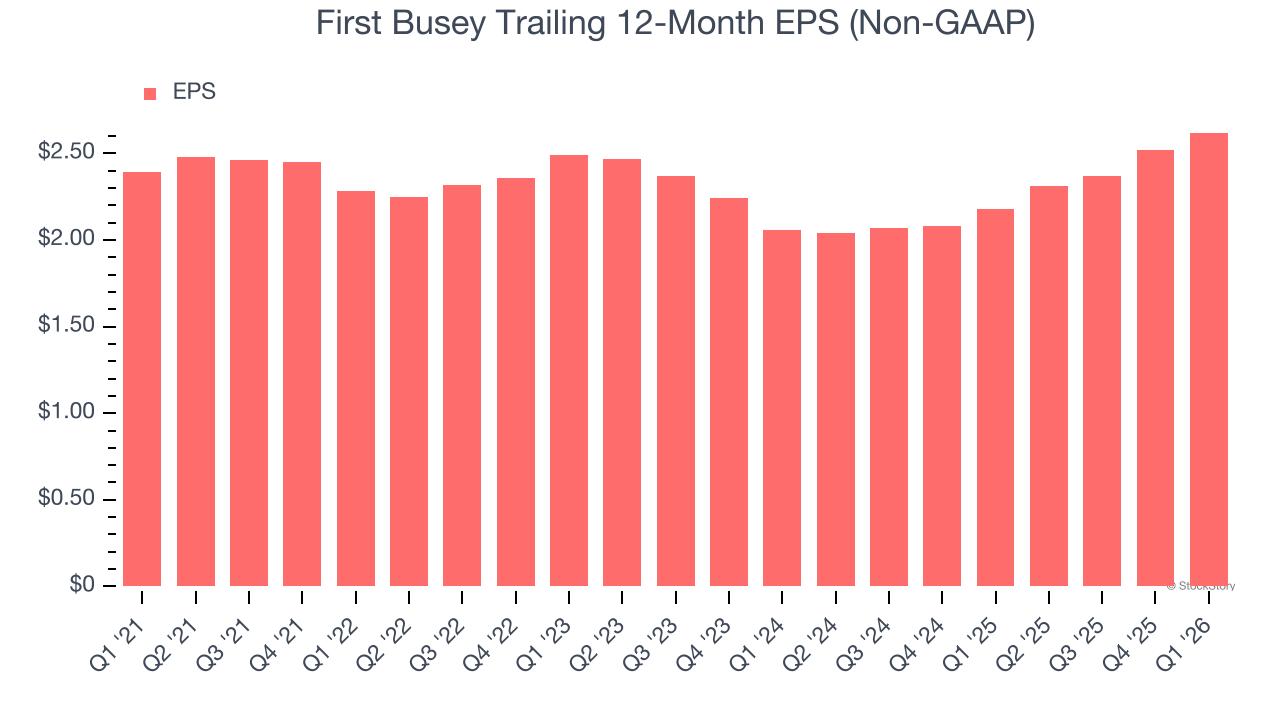

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

First Busey’s EPS grew at a weak 1.9% compounded annual growth rate over the last five years, lower than its 14.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

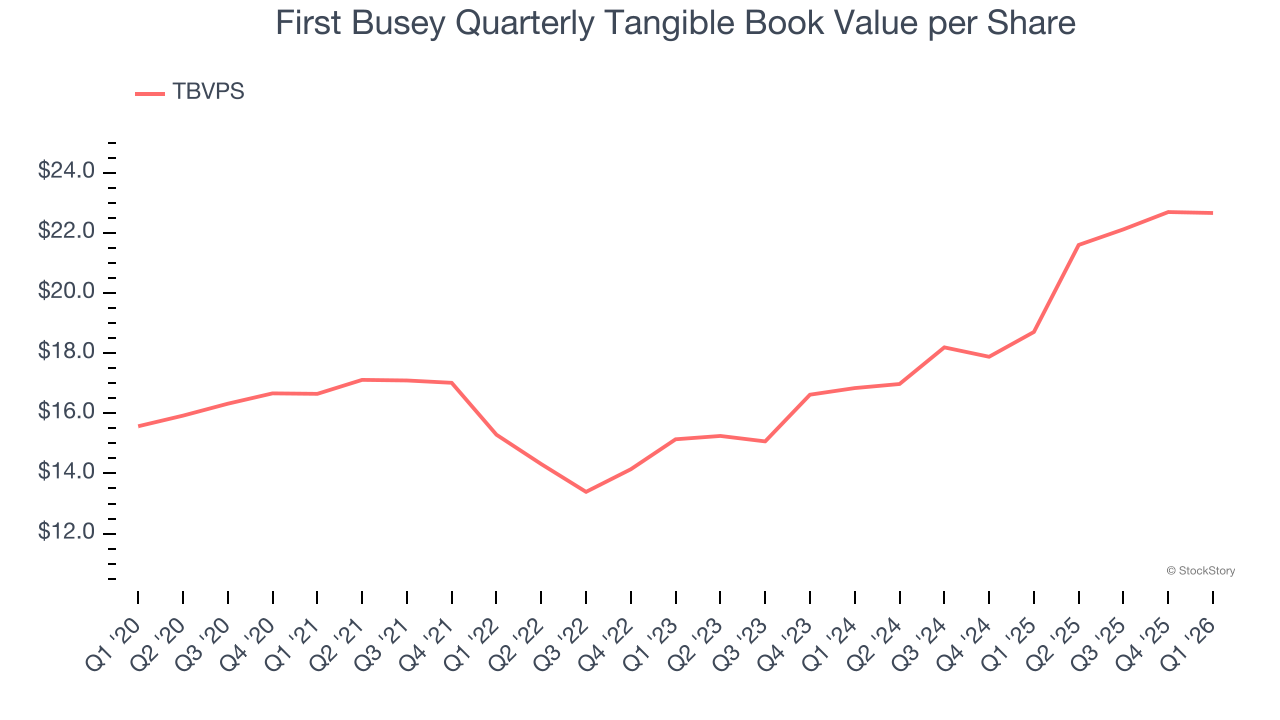

3. TBVPS Projections Show Stormy Skies Ahead

A bank’s tangible book value per share (TBVPS) increases when it generates higher net interest margins and keeps credit losses low, allowing it to compound shareholder value over time.

Over the next 12 months, Consensus estimates call for First Busey’s TBVPS to shrink by 3.1% to $21.96, a sour projection.

Final Judgment

First Busey’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 1× forward P/B (or $28.23 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.