Shareholders of Gevo would probably like to forget the past six months even happened. The stock dropped 34.6% and now trades at $1.44. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the drawdown, is now a good time to buy GEVO? Find out in our full research report, it’s free.

Why Does GEVO Stock Spark Debate?

Operating one of the largest dairy-based renewable natural gas facilities in the United States, Gevo (NASDAQ: GEVO) produces sustainable aviation fuel and other renewable hydrocarbon fuels from plant-based feedstocks like corn.

Two Things to Like:

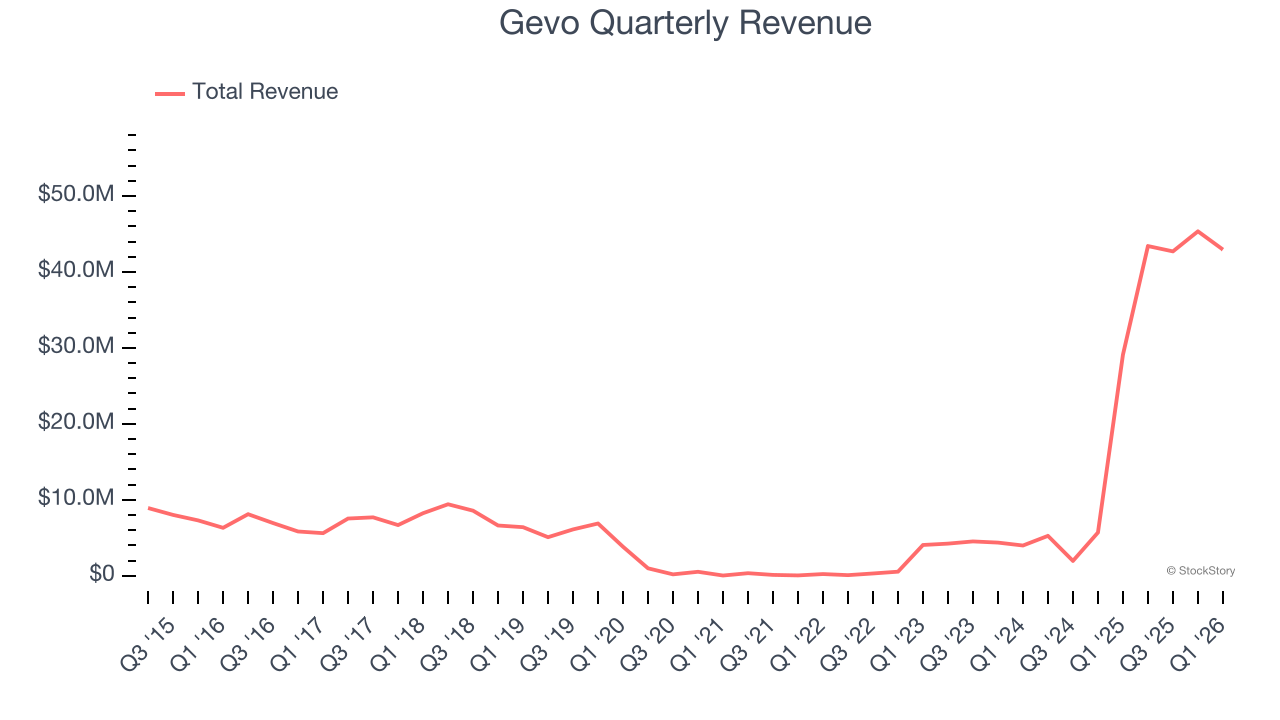

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Luckily, Gevo’s sales grew at an incredible 151% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Gevo’s EBITDA margin rose over the last year, as its sales growth gave it operating leverage. Its EBITDA margin for the trailing 12 months was 23.1%.

One Reason to Be Careful:

Cash Burn Ignites Concerns

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Gevo’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 214%, meaning it lit $213.84 of cash on fire for every $100 in revenue.

Final Judgment

Gevo’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 10.8× forward EV-to-EBITDA (or $1.44 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Gevo

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.