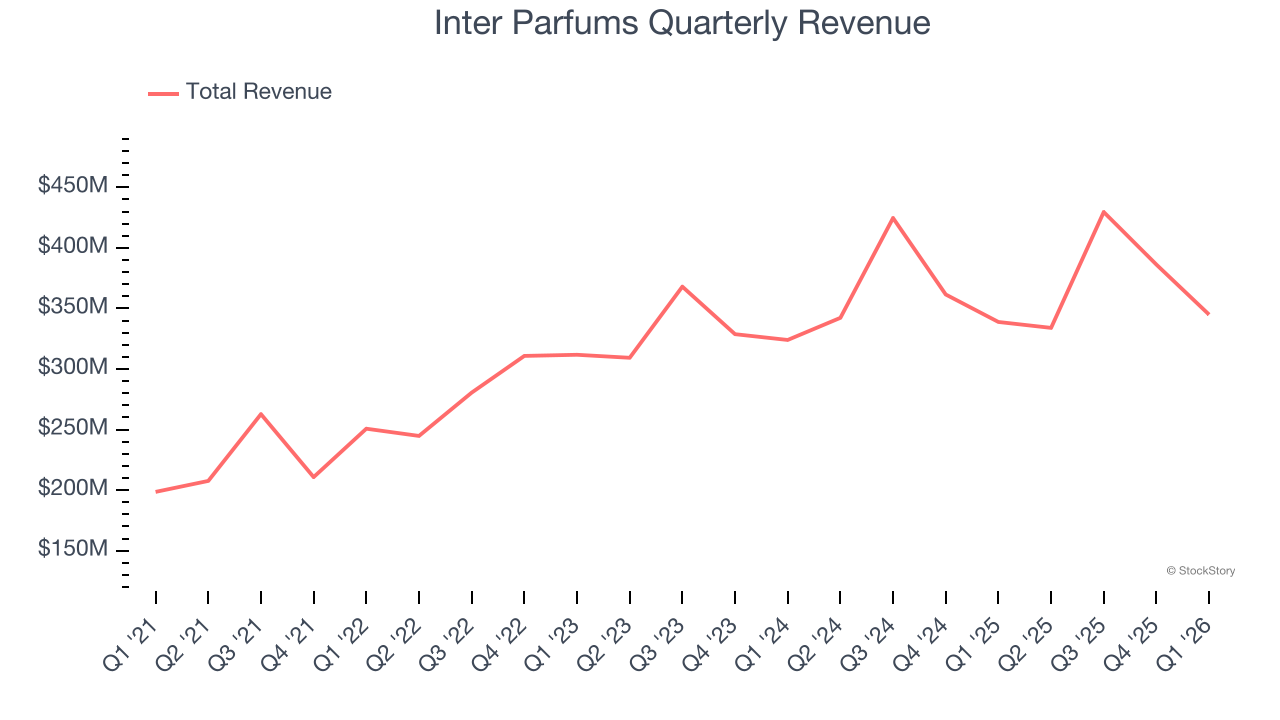

Fragrance and perfume company Inter Parfums (NASDAQ: IPAR) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 1.8% year on year to $344.9 million. On the other hand, the company’s full-year revenue guidance of $1.48 billion at the midpoint came in 1.3% below analysts’ estimates. Its GAAP profit of $1.35 per share was 14.4% above analysts’ consensus estimates.

Is now the time to buy Inter Parfums? Find out by accessing our full research report, it’s free.

Inter Parfums (IPAR) Q1 CY2026 Highlights:

- Revenue: $344.9 million vs analyst estimates of $345 million (1.8% year-on-year growth, in line)

- EPS (GAAP): $1.35 vs analyst estimates of $1.18 (14.4% beat)

- Adjusted Operating Income: $74.13 million vs analyst estimates of $71.15 million (21.5% margin, 4.2% beat)

- The company reconfirmed its revenue guidance for the full year of $1.48 billion at the midpoint

- EPS (GAAP) guidance for the full year is $4.85 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 21.5%, in line with the same quarter last year

- Market Capitalization: $2.88 billion

Company Overview

With licenses to produce colognes and perfumes under brands such as Kate Spade, Van Cleef & Arpels, and Abercrombie & Fitch, Inter Parfums (NASDAQ: IPAR) manufactures and distributes fragrances worldwide.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.49 billion in revenue over the past 12 months, Inter Parfums is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Inter Parfums’s 9.2% annualized revenue growth over the last three years was decent. This shows its offerings generated slightly more demand than the average consumer staples company, a useful starting point for our analysis.

This quarter, Inter Parfums grew its revenue by 1.8% year on year, and its $344.9 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

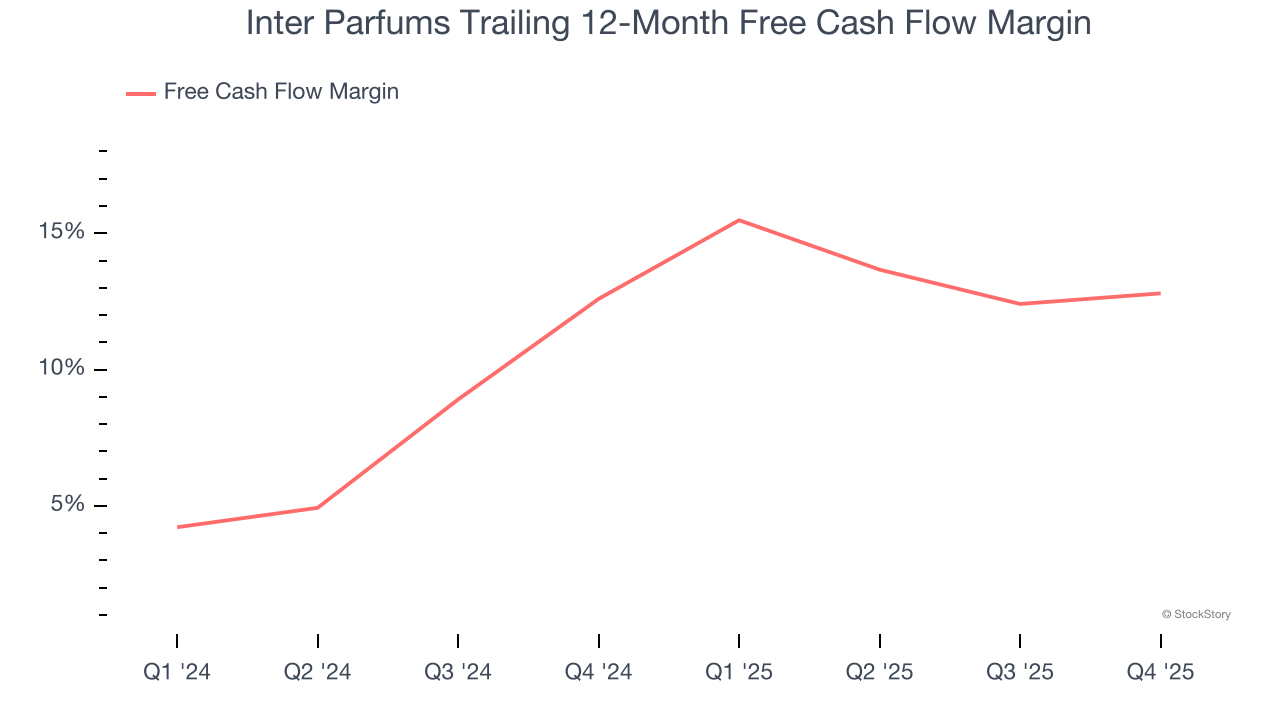

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Inter Parfums has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 16.3% over the last two years.

Key Takeaways from Inter Parfums’s Q1 Results

It was encouraging to see Inter Parfums beat analysts’ gross margin expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $91.64 immediately after reporting.

Is Inter Parfums an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).