SunOpta’s 11.9% return over the past six months has outpaced the S&P 500 by 8.7%, and its stock price has climbed to $6.49 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in SunOpta, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think SunOpta Will Underperform?

Despite the momentum, we're cautious about SunOpta. Here are three reasons we avoid STKL and a stock we'd rather own.

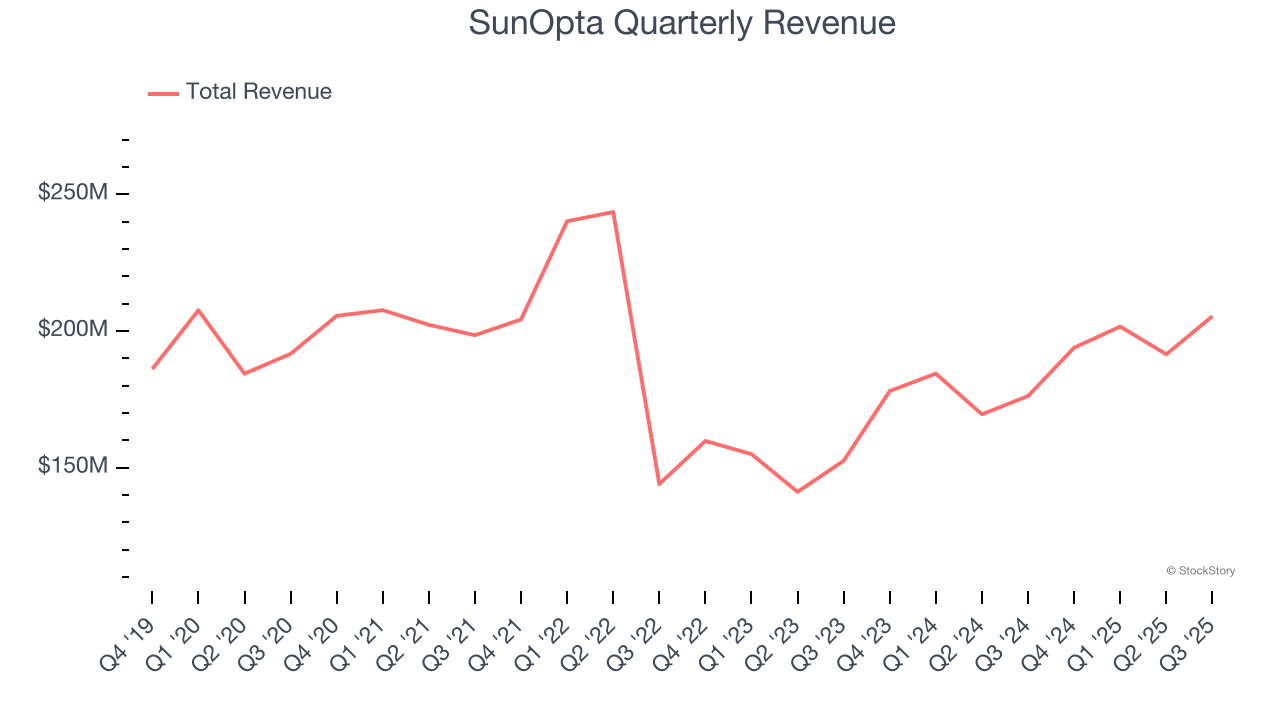

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. SunOpta’s demand was weak over the last three years as its sales fell at a 1.6% annual rate. This wasn’t a great result and is a sign of poor business quality.

2. Fewer Distribution Channels Limit its Ceiling

With $792.4 million in revenue over the past 12 months, SunOpta is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

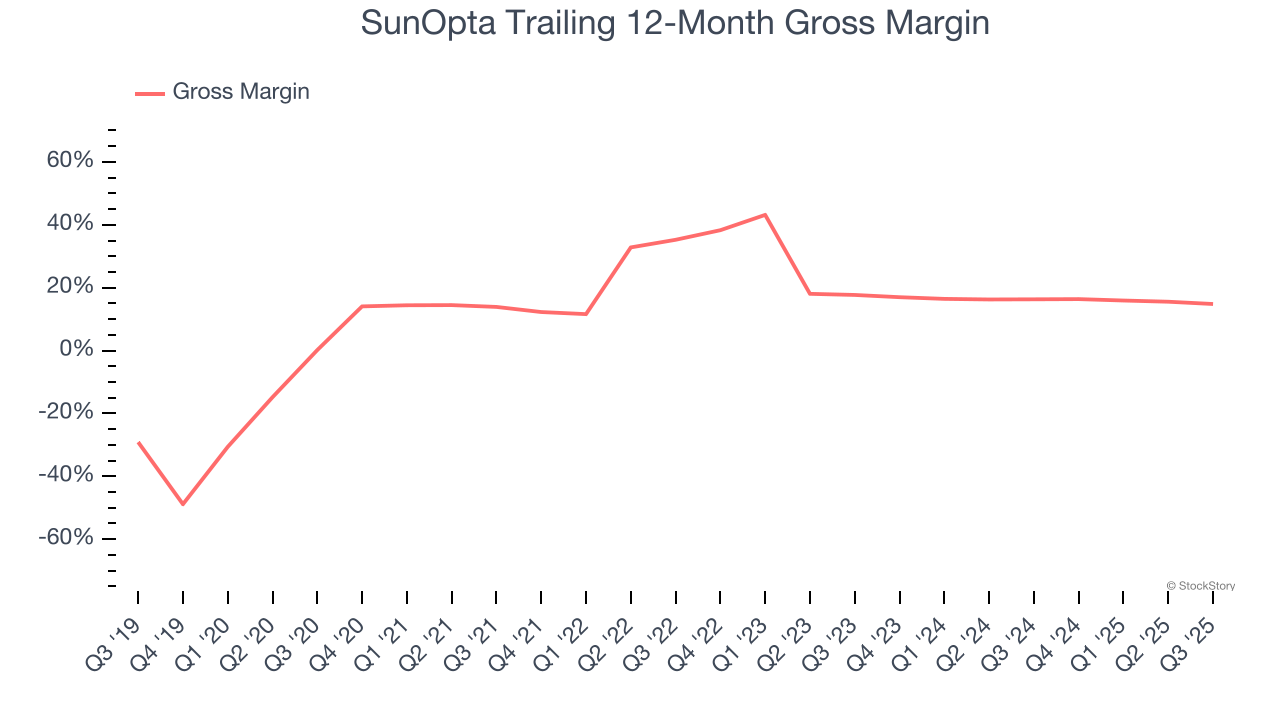

3. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

SunOpta has bad unit economics for a consumer staples company, signaling it operates in a competitive market and lacks pricing power because its products can be substituted. As you can see below, it averaged a 15.5% gross margin over the last two years. Said differently, for every $100 in revenue, a chunky $84.48 went towards paying for raw materials, production of goods, transportation, and distribution.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of SunOpta, we’ll be cheering from the sidelines. With its shares outperforming the market lately, the stock trades at 36.6× forward P/E (or $6.49 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of SunOpta

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.