Redwire’s 9.5% return over the past six months has outpaced the S&P 500 by 6.4%, and its stock price has climbed to $9.79 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Redwire, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Redwire Not Exciting?

Despite the momentum, we're swiping left on Redwire for now. Here are three reasons there are better opportunities than RDW and a stock we'd rather own.

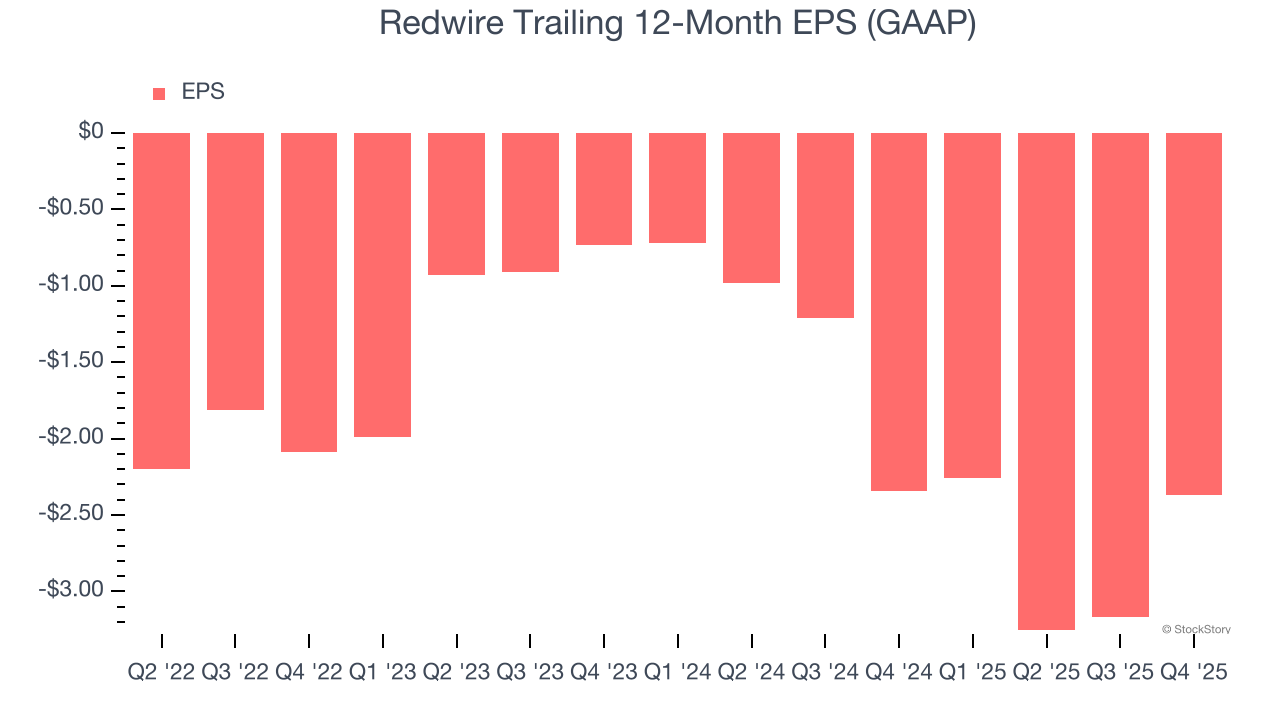

1. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Redwire’s earnings losses deepened over the last four years as its EPS dropped 5.6% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Redwire’s low margin of safety could leave its stock price susceptible to large downswings.

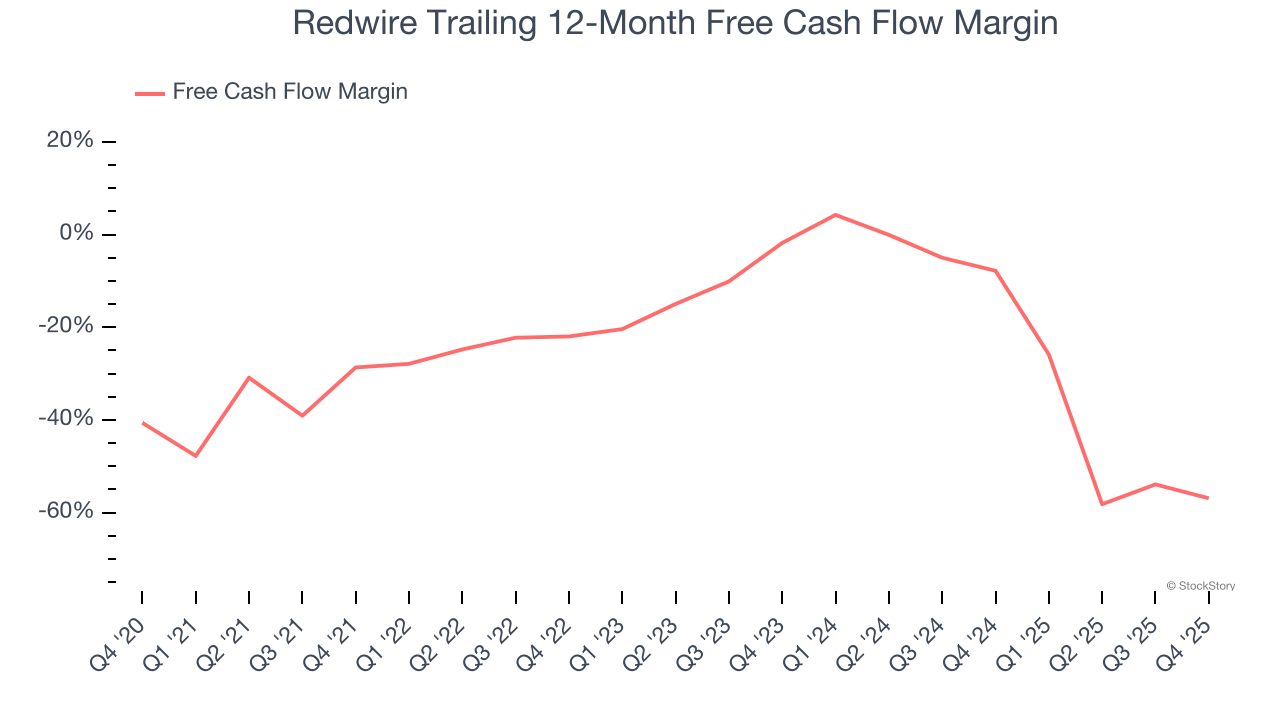

2. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Redwire’s margin dropped by 28.2 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business. Redwire’s free cash flow margin for the trailing 12 months was negative 56.9%.

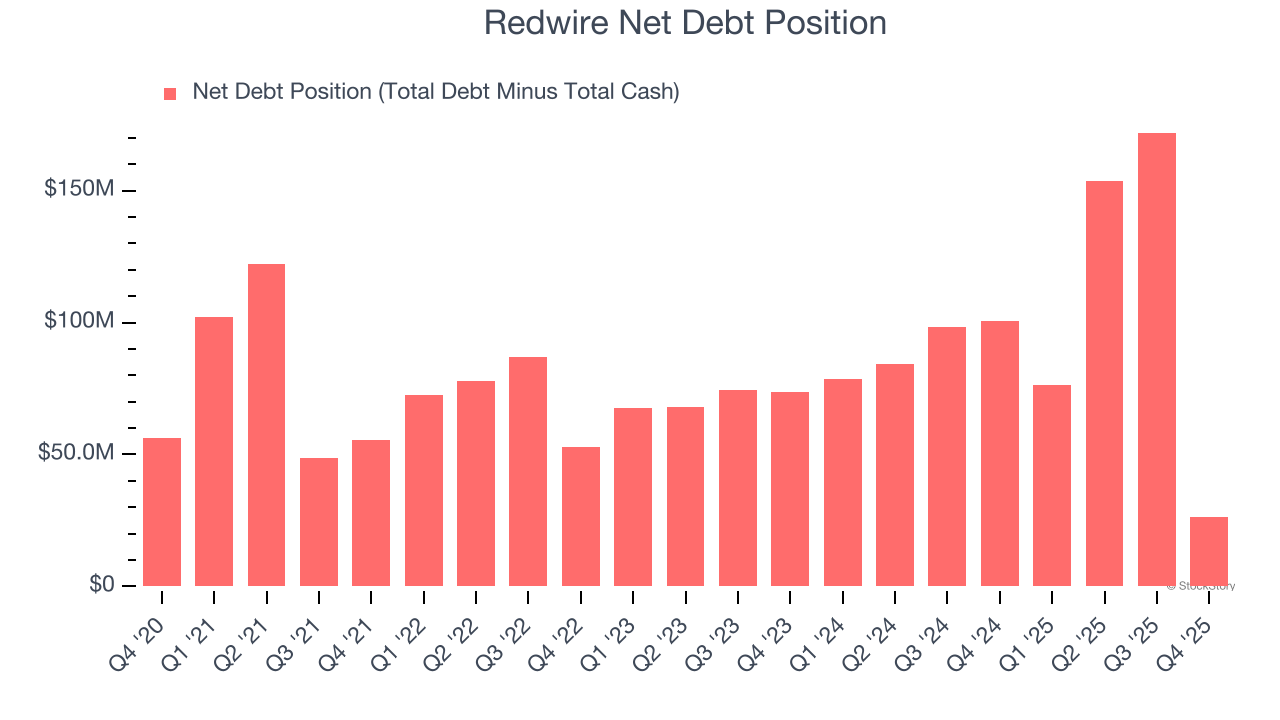

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Redwire burned through $190.8 million of cash over the last year, and its $121.4 million of debt exceeds the $95.18 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Redwire’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Redwire until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Redwire’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 1,662.5× forward EV-to-EBITDA (or $9.79 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.