Lemonade has had an impressive run over the past six months as its shares have beaten the S&P 500 by 16.3%. The stock now trades at $62.65, marking a 19.4% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Lemonade, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Lemonade Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why LMND doesn't excite us and a stock we'd rather own.

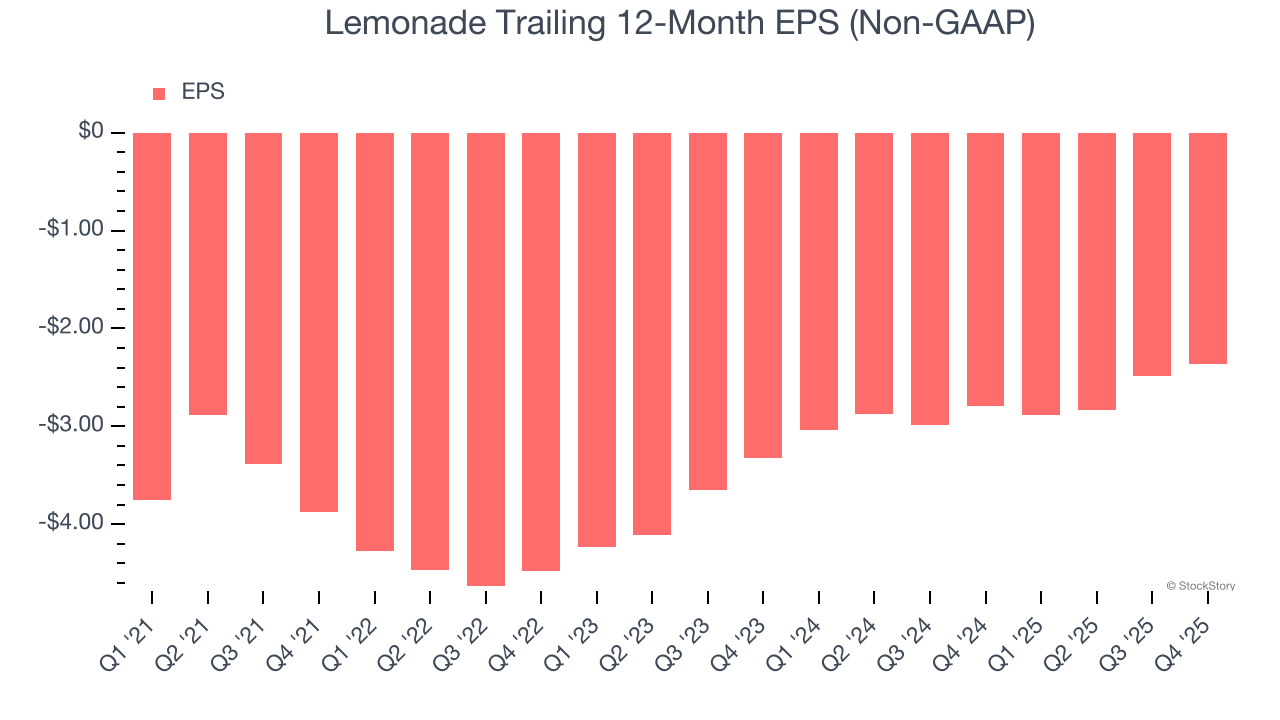

1. EPS Barely Improving Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

For Lemonade, its two-year annual EPS growth of 15.8% was higher than its five-year trend. Its improving earnings is an encouraging data point, but a caveat is that its EPS is still in the red.

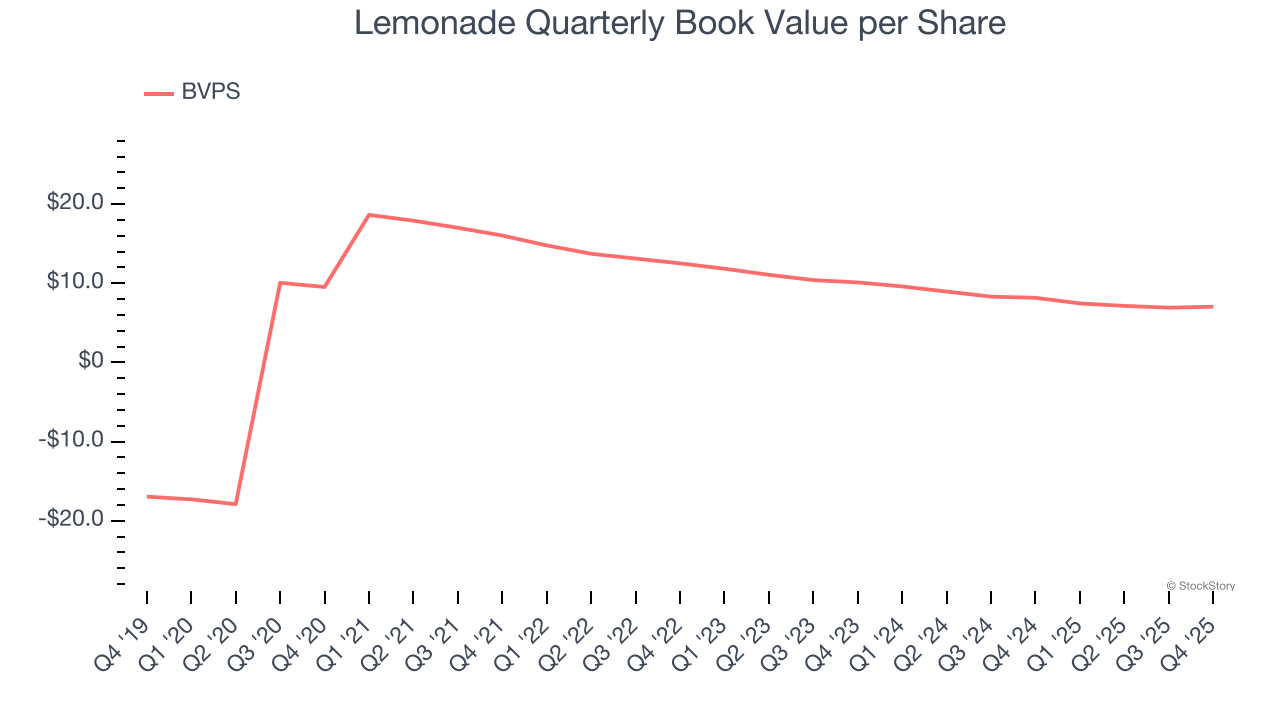

2. Declining BVPS Reflects Erosion of Asset Value

In the insurance industry, book value per share (BVPS) provides a clear picture of shareholder value, as it represents the total equity backing a company’s insurance operations and growth initiatives.

To the detriment of investors, Lemonade’s BVPS continued freefalling over the past two years as BVPS declined at a -16.6% annual clip (from $10.10 to $7.03 per share).

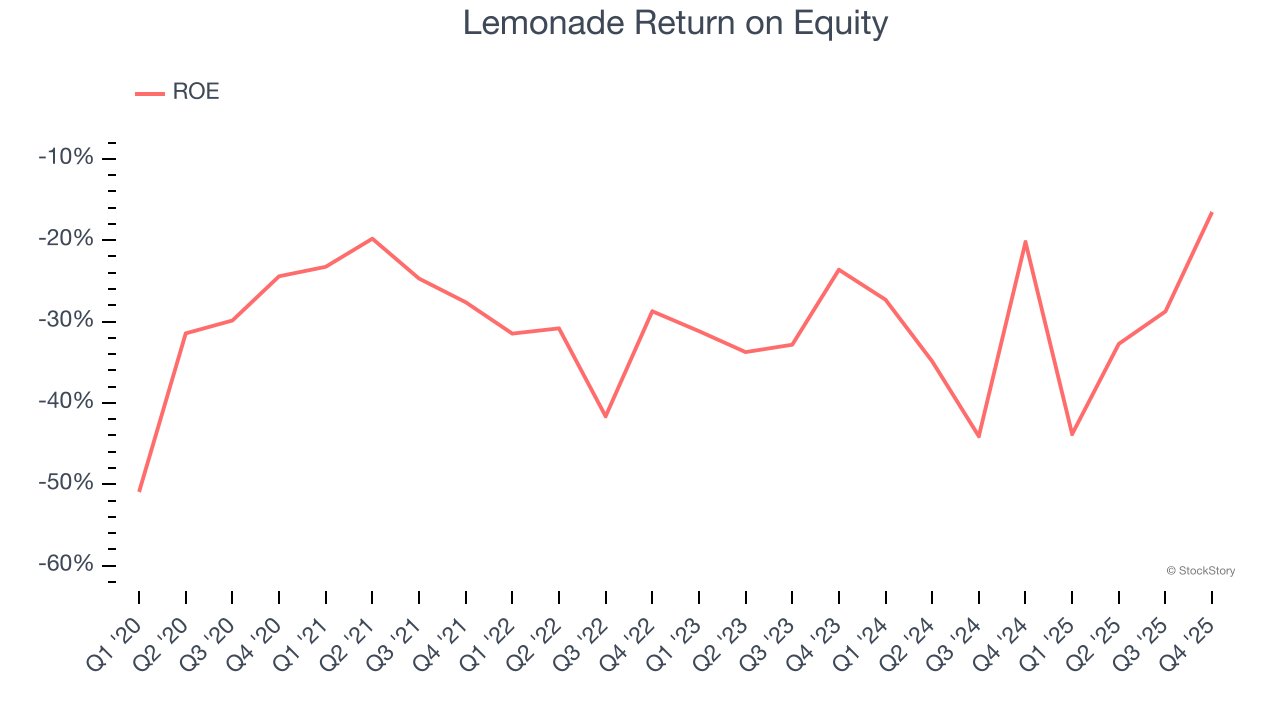

3. Previous Growth Initiatives Have Lost Money

Return on equity, or ROE, represents the ultimate measure of an insurer's effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Lemonade has averaged an ROE of negative 29.9%, a bad result not only in absolute terms but also relative to the majority of insurers putting up 20%+. It also shows that Lemonade has little to no competitive moat.

Final Judgment

Lemonade isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 9.7× forward P/B (or $62.65 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of Lemonade

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.