What a time it’s been for RPC. In the past six months alone, the company’s stock price has increased by a massive 50.4%, reaching $7.16 per share. This run-up might have investors contemplating their next move.

Is now the time to buy RPC, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is RPC Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about RPC. Here are three reasons you should be careful with RES and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks.

RPC’s $1.63 billion of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

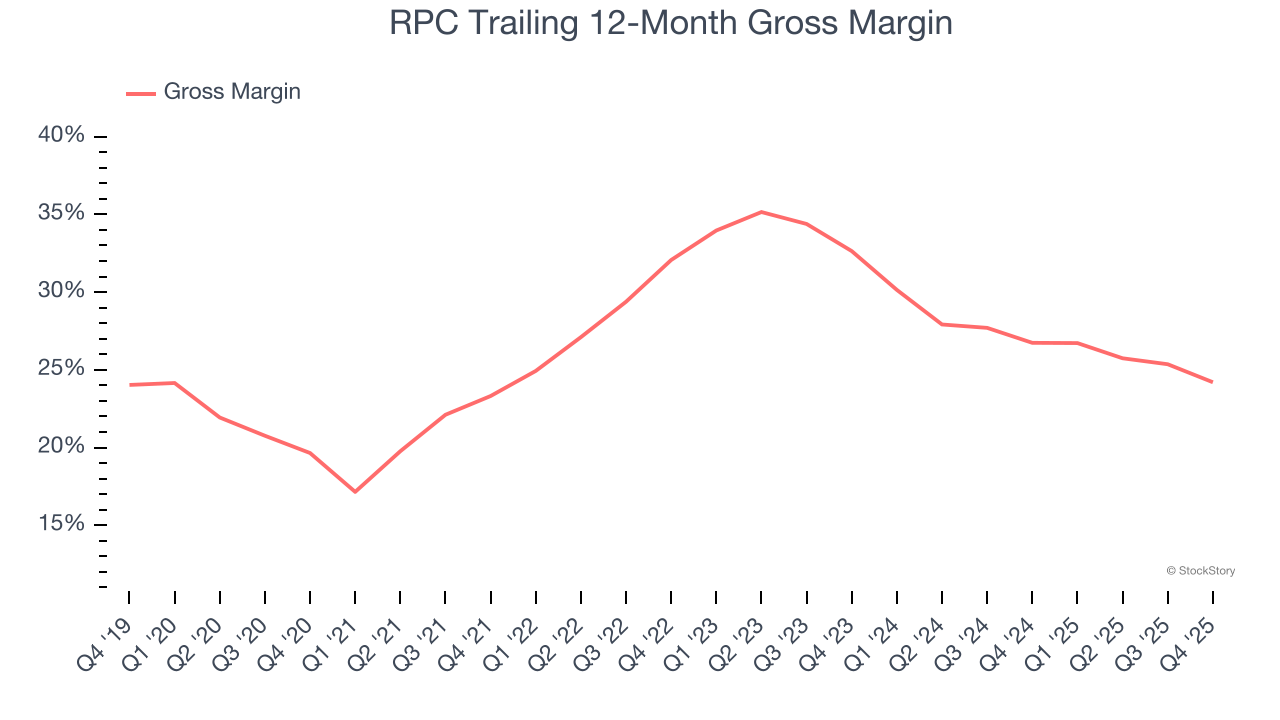

2. Low Gross Margin Reveals Weak Structural Profitability

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

RPC, which averaged 28.3% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

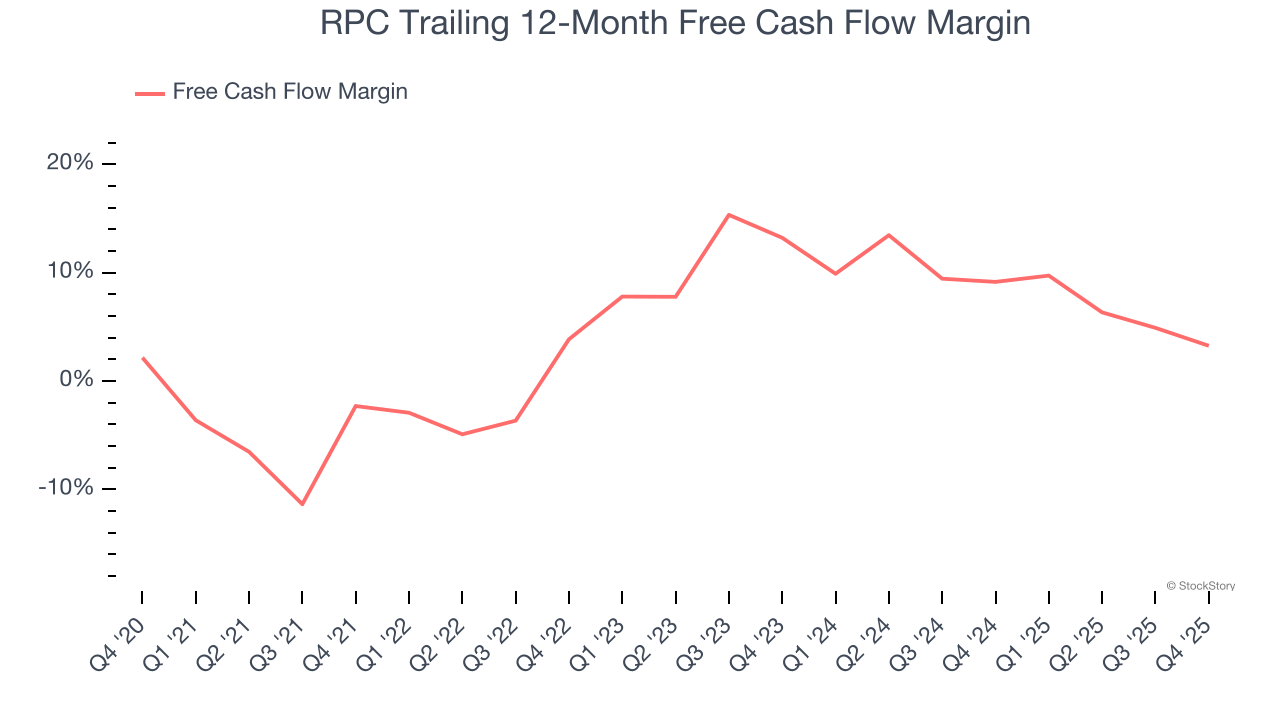

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

RPC has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.1%, below what we’d expect for an upstream and integrated energy business.

Final Judgment

RPC isn’t a terrible business, but it doesn’t pass our quality test. After the recent rally, the stock trades at 33.8× forward P/E (or $7.16 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d recommend looking at one of our top software and edge computing picks.

Stocks We Would Buy Instead of RPC

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.