Over the past six months, Keurig Dr Pepper’s stock price fell to $27.76. Shareholders have lost 15.8% of their capital, which is disappointing considering the S&P 500 has climbed by 8.2%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Keurig Dr Pepper, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Keurig Dr Pepper Not Exciting?

Even with the cheaper entry price, we're swiping left on Keurig Dr Pepper for now. Here are three reasons there are better opportunities than KDP and a stock we'd rather own.

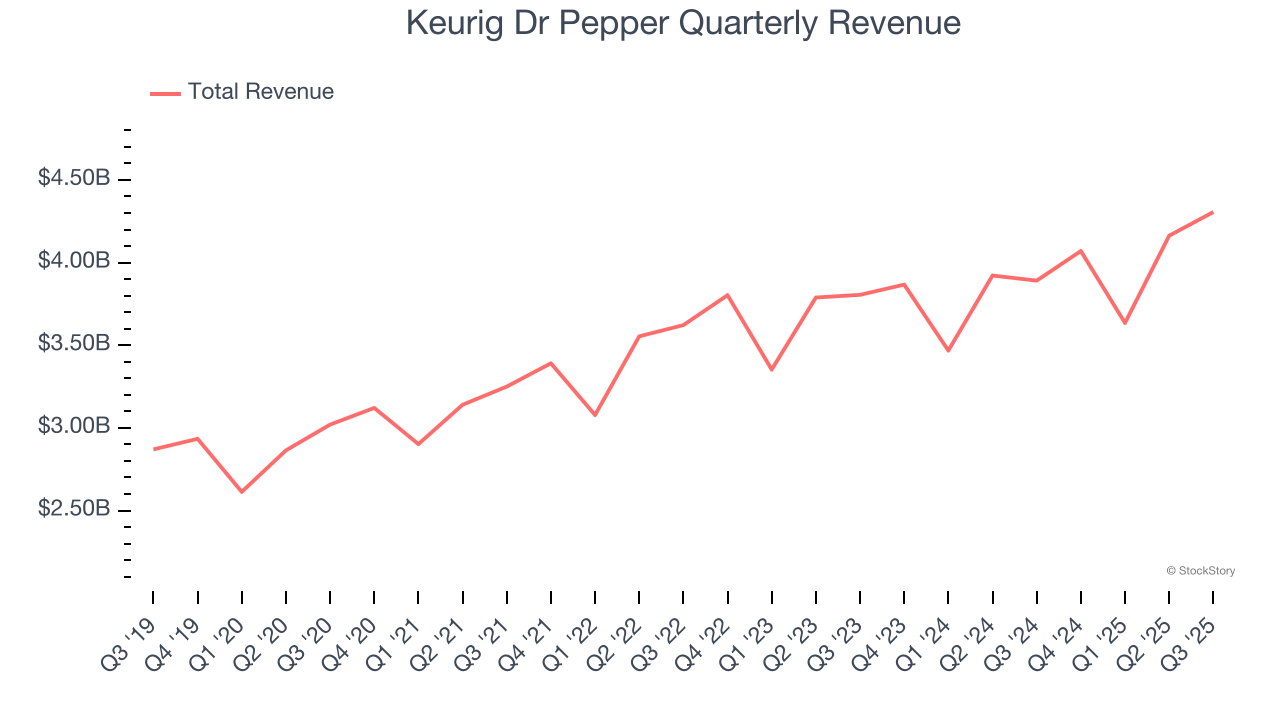

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Keurig Dr Pepper grew its sales at a mediocre 5.8% compounded annual growth rate. This fell short of our benchmark for the consumer staples sector.

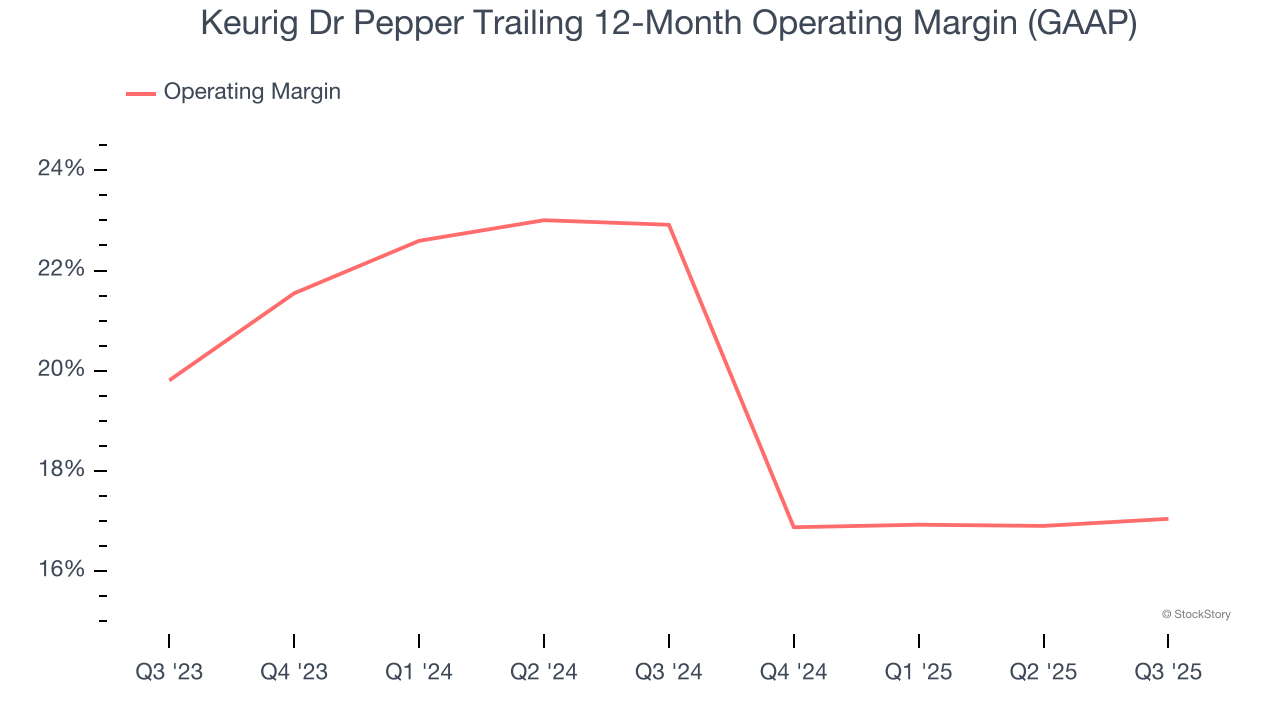

2. Shrinking Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Keurig Dr Pepper’s operating margin decreased by 5.9 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 17%.

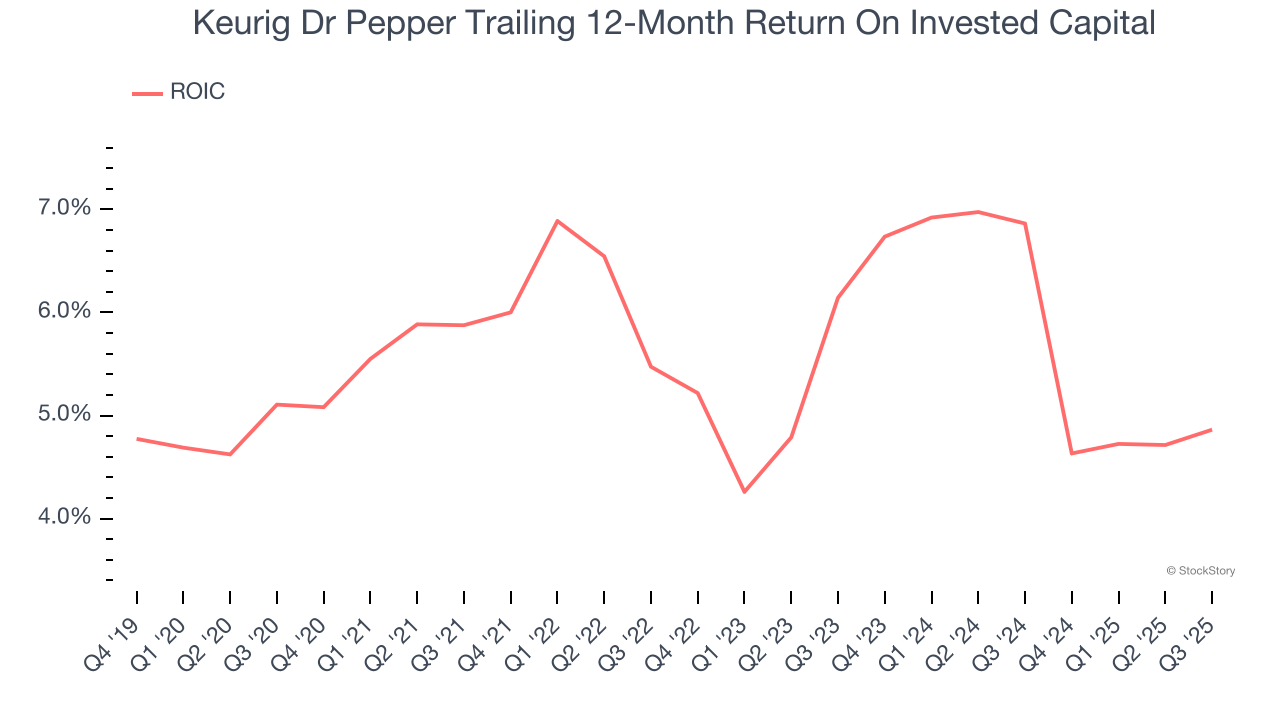

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Keurig Dr Pepper historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.8%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

Final Judgment

Keurig Dr Pepper’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 13× forward P/E (or $27.76 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Keurig Dr Pepper

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.