Littelfuse has gotten torched over the last six months - since October 2024, its stock price has dropped 45.2% to a new 52-week low of $142.64 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Littelfuse, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Even with the cheaper entry price, we're cautious about Littelfuse. Here are three reasons why LFUS doesn't excite us and a stock we'd rather own.

Why Do We Think Littelfuse Will Underperform?

The developer of the first blade-type automotive fuse, Littelfuse (NASDAQ: LFUS) provides electrical protection and control components for the automotive, industrial, electronics, and telecommunications industries.

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Littelfuse’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.6% over the last two years. Littelfuse isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

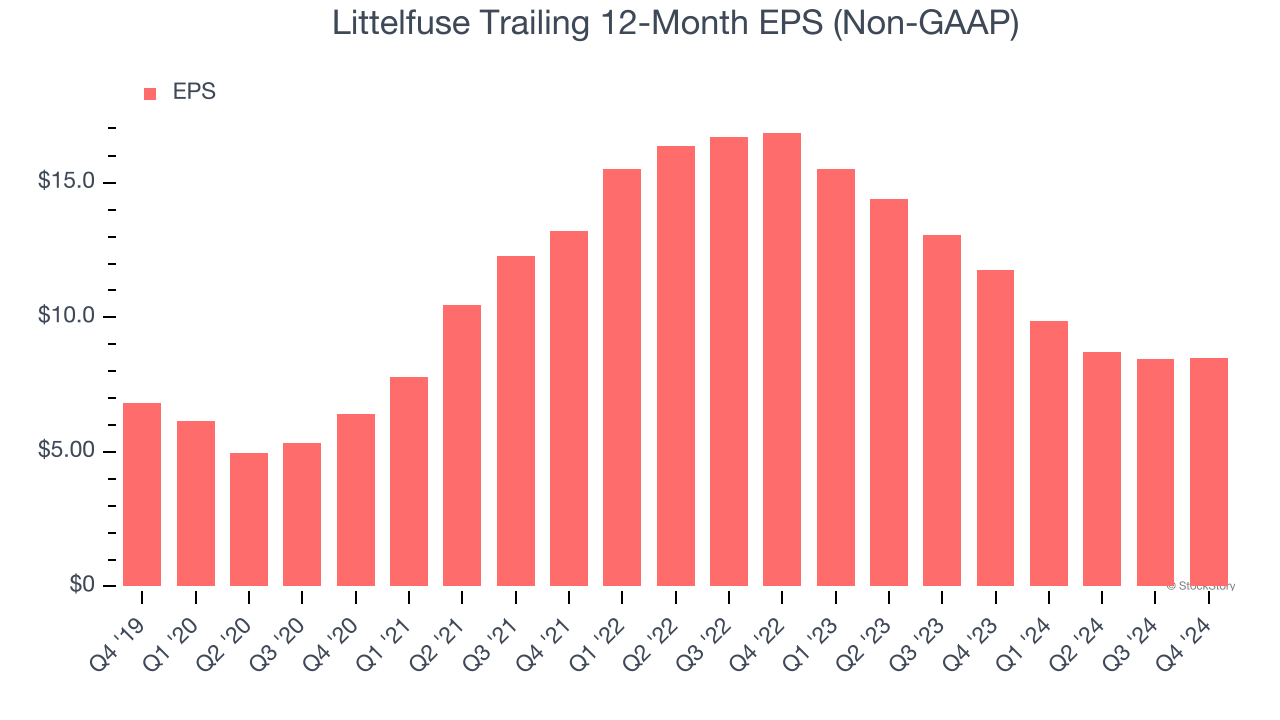

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Littelfuse’s EPS grew at an unimpressive 4.5% compounded annual growth rate over the last five years, lower than its 7.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Littelfuse’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Littelfuse, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 15× forward price-to-earnings (or $142.64 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Littelfuse

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.