Kimberly-Clark has been treading water for the past six months, recording a small loss of 3.3% while holding steady at $140.43.

Is there a buying opportunity in Kimberly-Clark, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Kimberly-Clark for now. Here are three reasons why you should be careful with KMB and a stock we'd rather own.

Why Is Kimberly-Clark Not Exciting?

Originally founded as a Wisconsin paper mill in 1872, Kimberly-Clark (NYSE: KMB) is now a household products powerhouse known for personal care and tissue products.

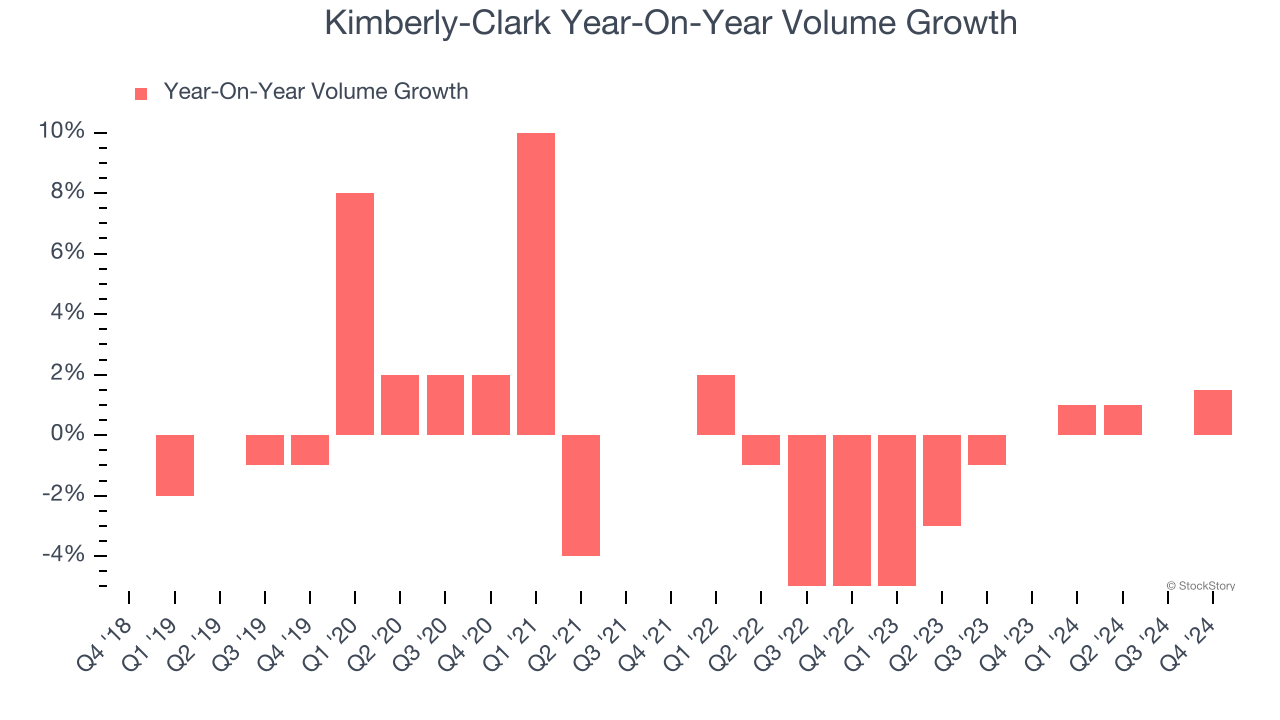

1. Sales Volumes Stall, Demand Waning

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Kimberly-Clark’s quarterly sales volumes have, on average, stayed about the same over the last two years. This stability is normal because the quantity demanded for consumer staples products typically doesn’t see much volatility.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Kimberly-Clark’s revenue to drop by 3.1%, a decrease from its 1% annualized growth for the past three years. This projection doesn't excite us and implies its products will face some demand challenges.

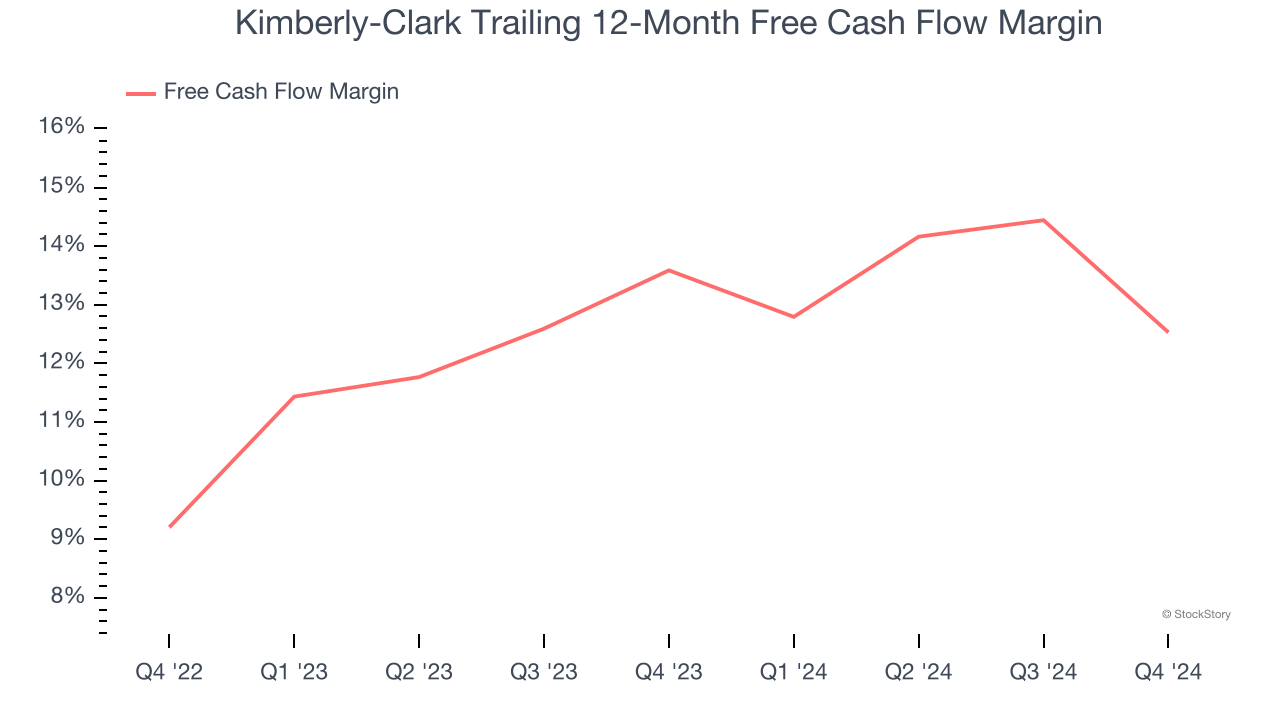

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Kimberly-Clark’s margin dropped by 1.1 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. Kimberly-Clark’s free cash flow margin for the trailing 12 months was 12.5%.

Final Judgment

Kimberly-Clark isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 18.9× forward price-to-earnings (or $140.43 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Kimberly-Clark

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.