While the broader market has struggled with the S&P 500 down 7.3% since October 2024, Vita Coco has surged ahead as its stock price has climbed by 8.4% to $31.20 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy COCO? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does COCO Stock Spark Debate?

Founded in 2004 followed by a 2021 IPO, The Vita Coco Company (NASDAQ: COCO) offers coconut water products that are a natural way to quench thirst.

Two Things to Like:

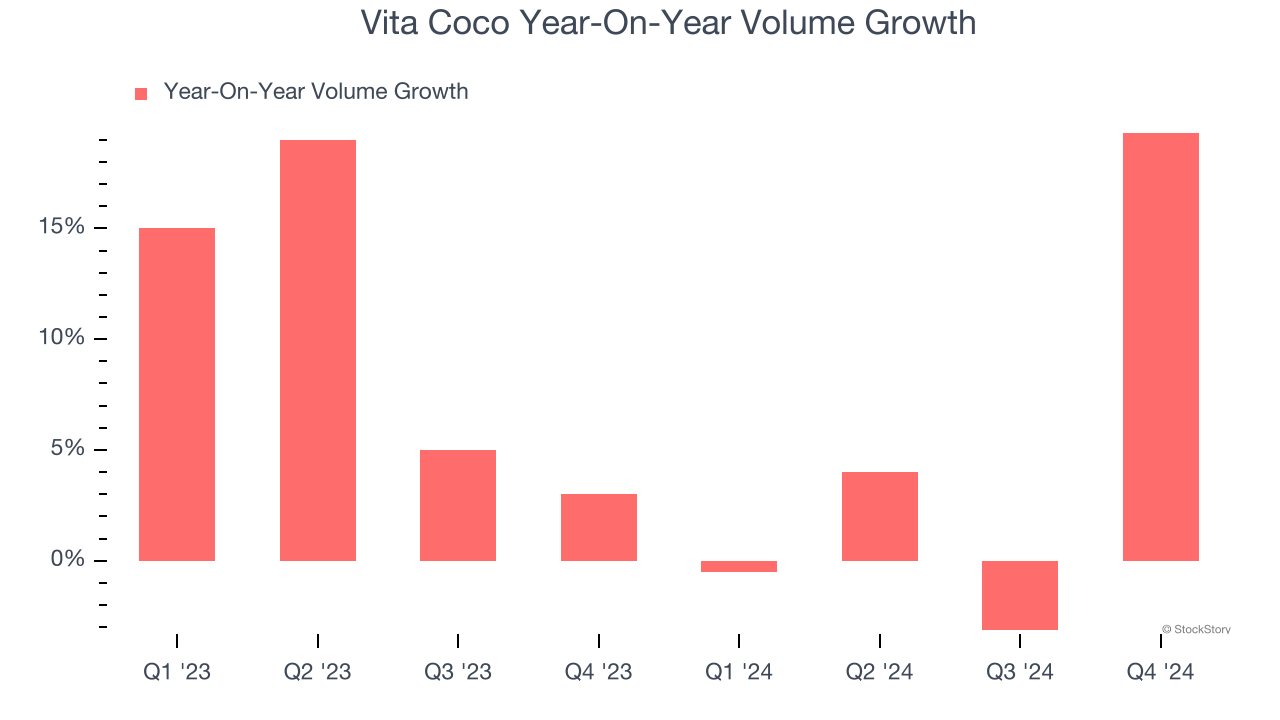

1. Elevated Demand Drives Higher Sales Volumes

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Vita Coco’s average quarterly volume growth was a robust 7.7% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

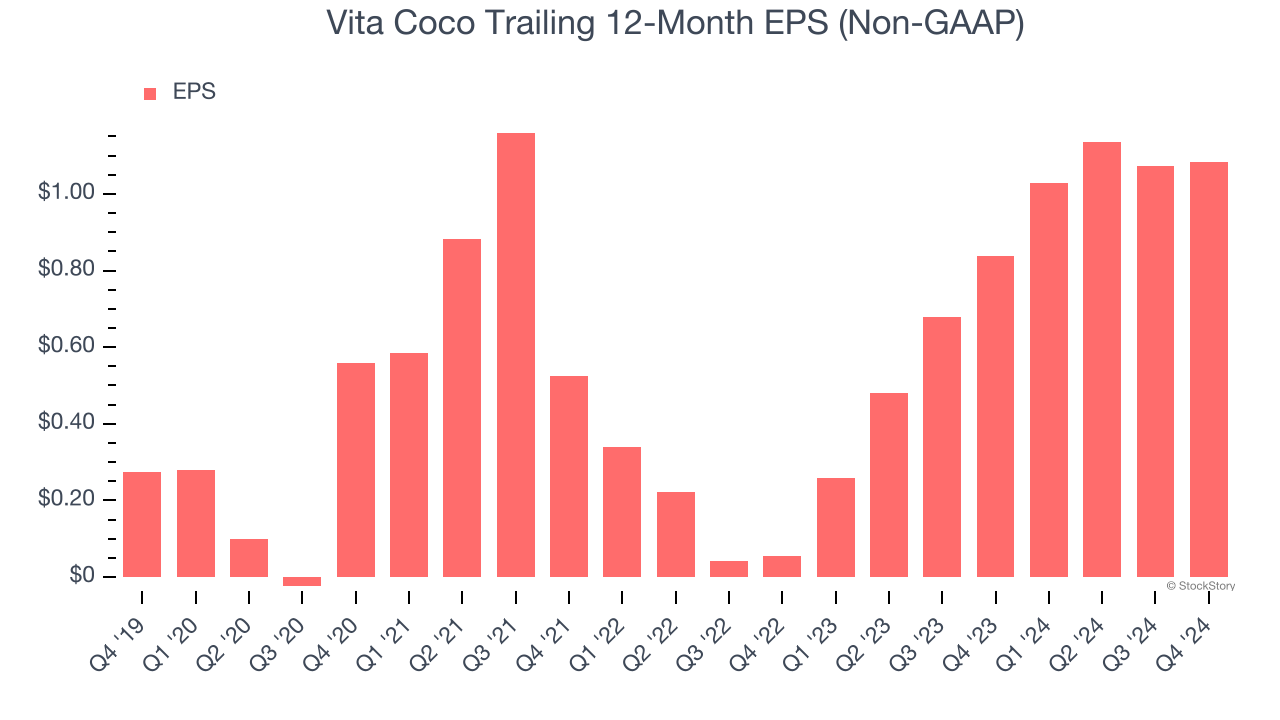

2. Outstanding Long-Term EPS Growth

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Vita Coco’s EPS grew at an astounding 27.3% compounded annual growth rate over the last three years, higher than its 10.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

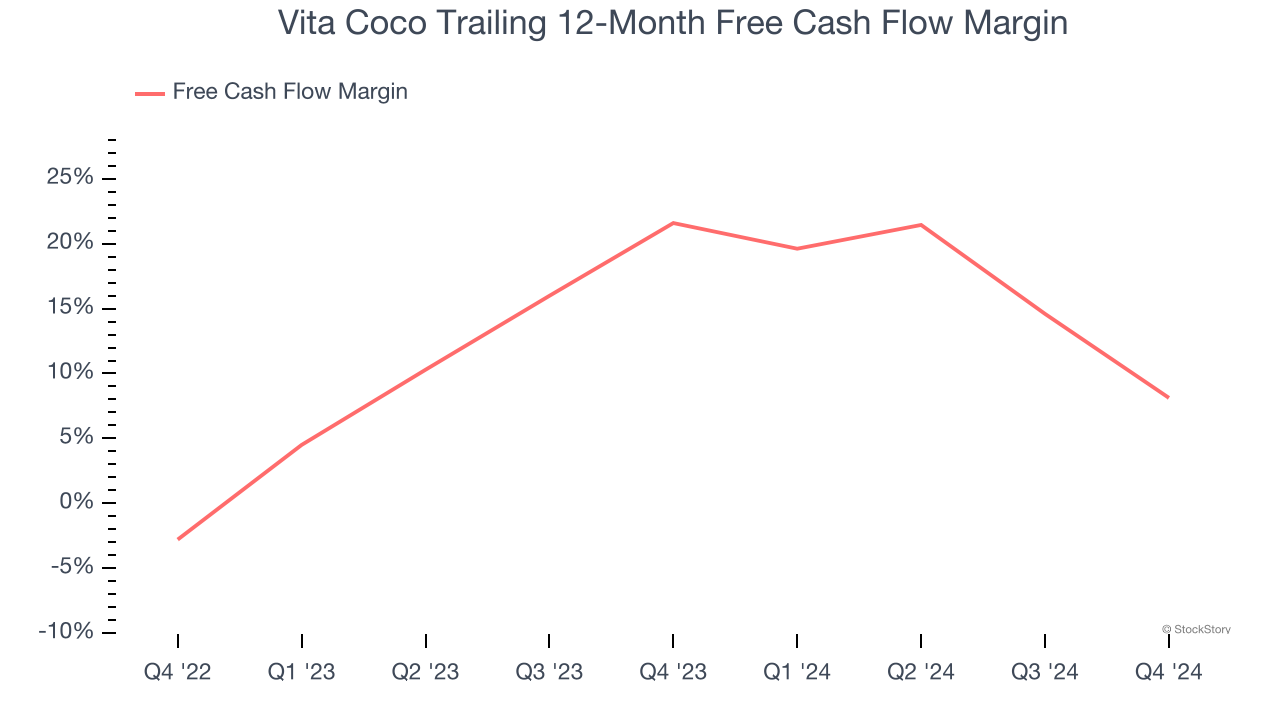

Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Vita Coco’s margin dropped by 13.5 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. Vita Coco’s free cash flow margin for the trailing 12 months was 8.1%.

Final Judgment

Vita Coco’s merits more than compensate for its flaws, and with its shares beating the market recently, the stock trades at 26.4× forward price-to-earnings (or $31.20 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Vita Coco

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.