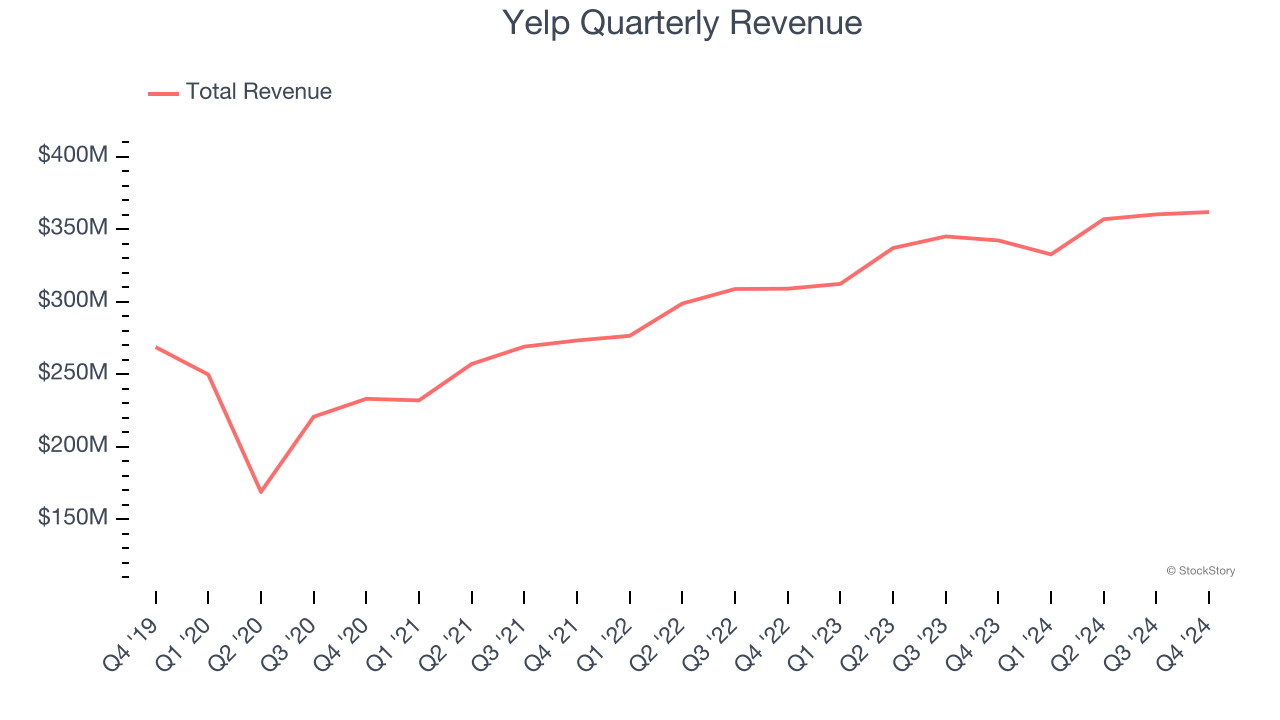

Local business platform Yelp (NYSE: YELP) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 5.7% year on year to $362 million. The company expects the full year’s revenue to be around $1.48 billion, close to analysts’ estimates. Its GAAP profit of $0.62 per share was 17.9% above analysts’ consensus estimates.

Is now the time to buy Yelp? Find out by accessing our full research report, it’s free.

Yelp (YELP) Q4 CY2024 Highlights:

- Revenue: $362 million vs analyst estimates of $350.5 million (5.7% year-on-year growth, 3.3% beat)

- EPS (GAAP): $0.62 vs analyst estimates of $0.53 (17.9% beat)

- Adjusted EBITDA: $101.1 million vs analyst estimates of $87.56 million (27.9% margin, 15.4% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.48 billion at the midpoint, in line with analyst expectations and implying 4.6% growth (vs 5.6% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $352.5 million at the midpoint, below analyst estimates of $362.9 million

- Operating Margin: 14.8%, up from 7.3% in the same quarter last year

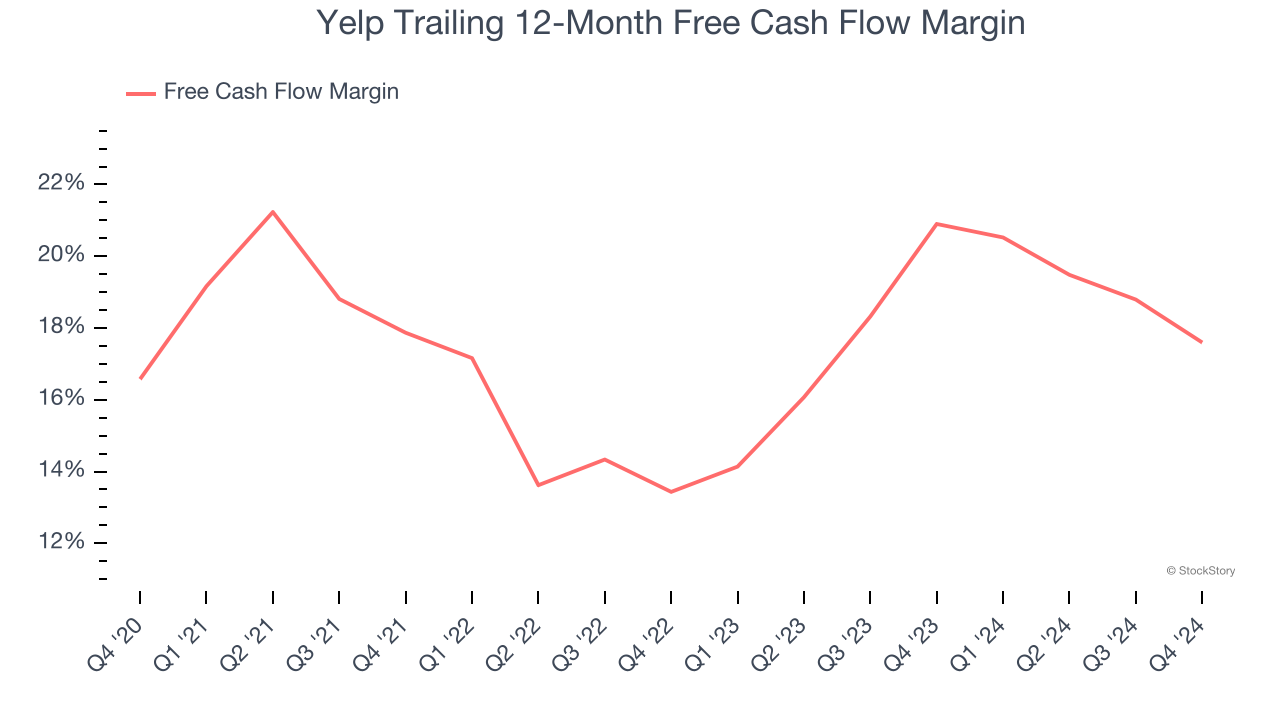

- Free Cash Flow Margin: 16.6%, down from 25.7% in the previous quarter

- Market Capitalization: $2.61 billion

“Yelp's 2024 results reflect the strong execution on our services roadmap,” said Jeremy Stoppelman, Yelp’s Co-Founder and Chief Executive Officer.

Company Overview

Founded by PayPal alumni Jeremy Stoppelman and Russel Simmons, Yelp (NYSE: YELP) is an online platform that helps people discover local businesses through crowd-sourced reviews.

Social Networking

Businesses must meet their customers where they are, which over the past decade has come to mean on social networks. In 2020, users spent over 2.5 hours a day on social networks, a figure that has increased every year since measurement began. As a result, businesses continue to shift their advertising and marketing dollars online.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, Yelp grew its sales at a decent 11% compounded annual growth rate. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Yelp reported year-on-year revenue growth of 5.7%, and its $362 million of revenue exceeded Wall Street’s estimates by 3.3%.

Looking ahead, sell-side analysts expect revenue to grow 4.4% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Yelp has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors while maintaining a cash cushion. The company’s free cash flow margin averaged 19.2% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Yelp’s margin was unchanged over the last few years, showing its long-term free cash flow profile is stable.

Yelp’s free cash flow clocked in at $59.96 million in Q4, equivalent to a 16.6% margin. The company’s cash profitability regressed as it was 4.8 percentage points lower than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Key Takeaways from Yelp’s Q4 Results

We were impressed by how significantly Yelp blew past analysts’ revenue, EPS, and EBITDA expectations this quarter. On the other hand, its full-year EBITDA guidance missed. Zooming out, we think this was a decent quarter featuring some areas of strength but also some blemishes. The stock traded up 3.8% to $42.08 immediately after reporting.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.