Target Hospitality’s stock price has taken a beating over the past six months, shedding 26.8% of its value and falling to $8.26 per share. This may have investors wondering how to approach the situation.

Given the weaker price action, is now a good time to buy TH? Find out in our full research report, it’s free.

Why Does TH Stock Spark Debate?

Essentially a builder of mini communities, Target Hospitality (NASDAQ: TH) is a provider of specialty workforce lodging accommodations and services.

Two Things to Like:

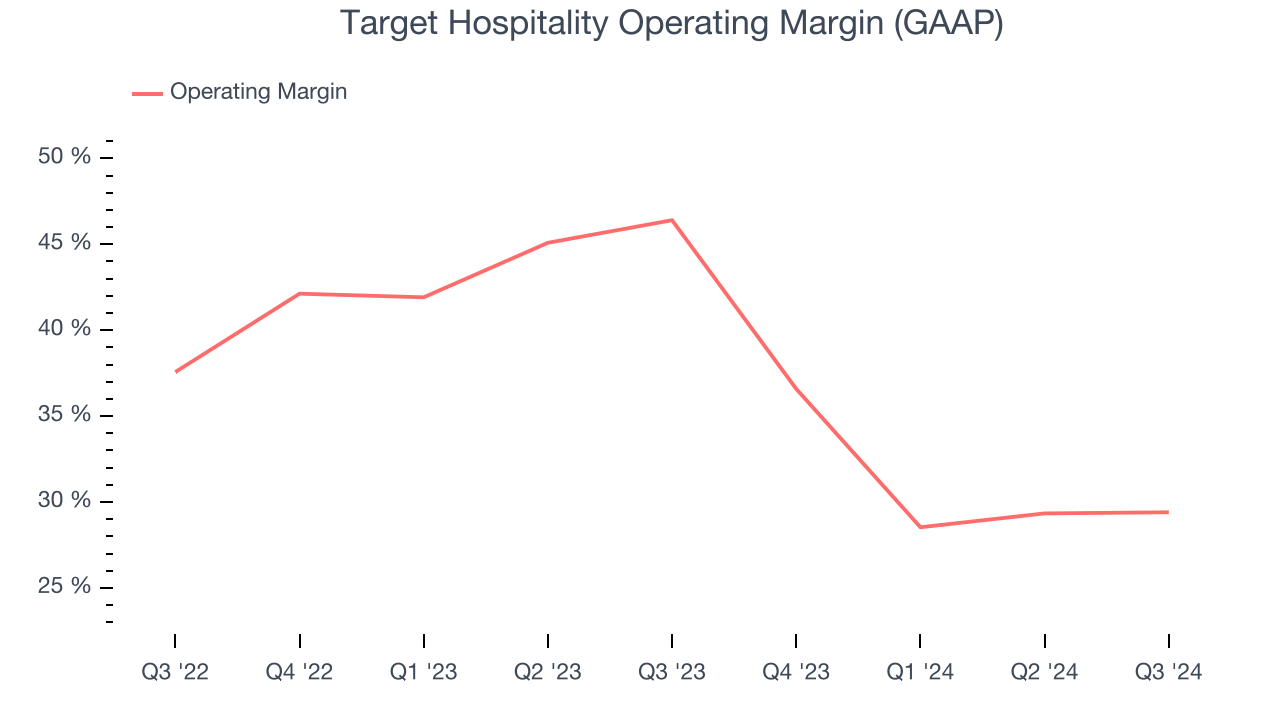

1. Operating Margin Reveals a Well-Run Organization

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Target Hospitality’s operating margin has shrunk over the last 12 months, but it still averaged 38.6% over the last two years, elite for a consumer discretionary business. This shows it’s an optimally-run company with an efficient cost structure, and we wouldn’t weigh the short-term trend too heavily.

2. New Investments Bear Fruit as ROIC Jumps

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Fortunately, Target Hospitality’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

One Reason to be Careful:

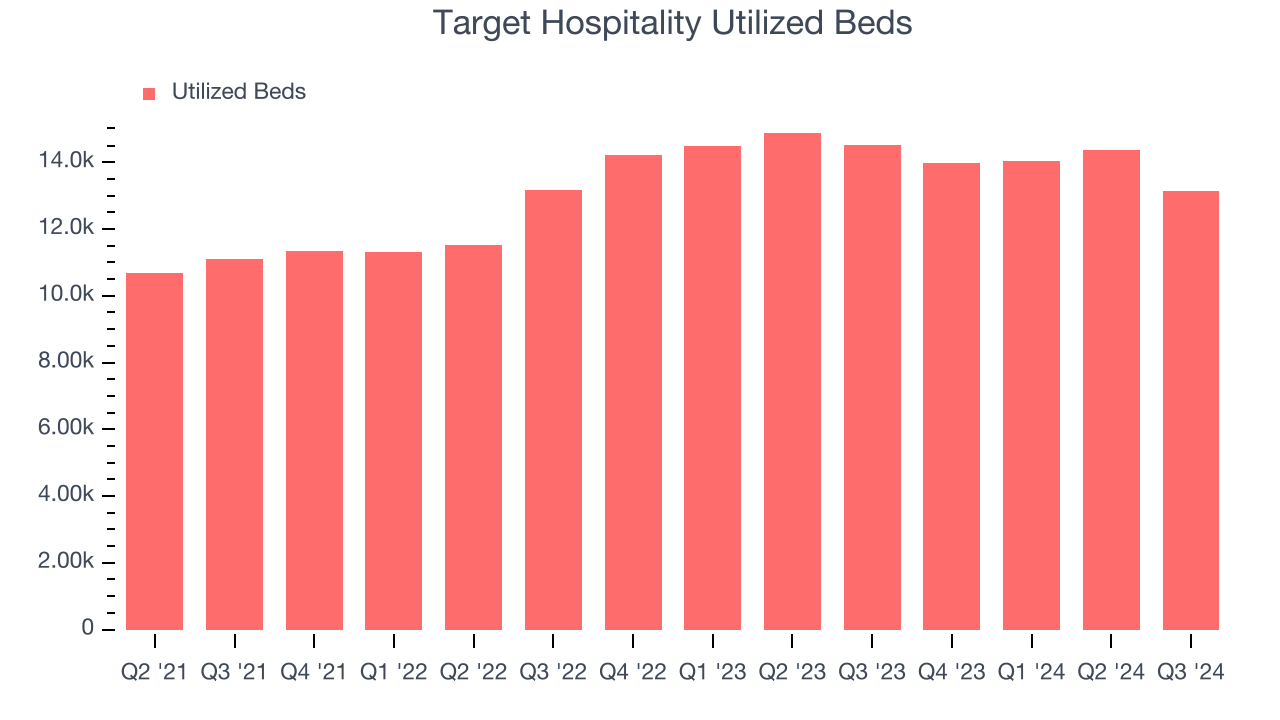

Weak Growth in Utilized Beds Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Target Hospitality, our preferred volume metric is utilized beds). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Target Hospitality’s utilized beds came in at 13,138 in the latest quarter, and over the last two years, averaged 9.4% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

Final Judgment

Target Hospitality has huge potential even though it has some open questions. With the recent decline, the stock trades at 5.2x forward EV-to-EBITDA (or $8.26 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Target Hospitality

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.