As of April 6, 2026, the global gold mining sector is navigating a "Great Decoupling." While gold bullion prices briefly touched historic peaks of $5,600 per ounce in January following geopolitical instability, the industry’s two largest titans—Newmont Corporation (NYSE: NEM) and Barrick Gold (NYSE: GOLD)—are struggling to translate record metal prices into shareholder value. A toxic cocktail of skyrocketing energy costs, production downgrades, and a high-stakes legal civil war has sent both stocks into a technical correction, leaving investors questioning the "bigger is better" mantra that has dominated the sector for the last decade.

The current atmosphere is defined by Newmont’s admission that 2026 will be a "trough year" for the company, as it grapples with a lower production guidance of 5.3 million ounces and a staggering jump in All-In Sustaining Costs (AISC). This operational weakness is occurring just as the "Gilded Peace" between Newmont and Barrick has shattered. A formal Notice of Default regarding their Nevada joint venture has moved into the litigation phase, signaling a period of prolonged uncertainty for the industry's most critical assets.

Operational Turmoil and the 'Trough Year' Pivot

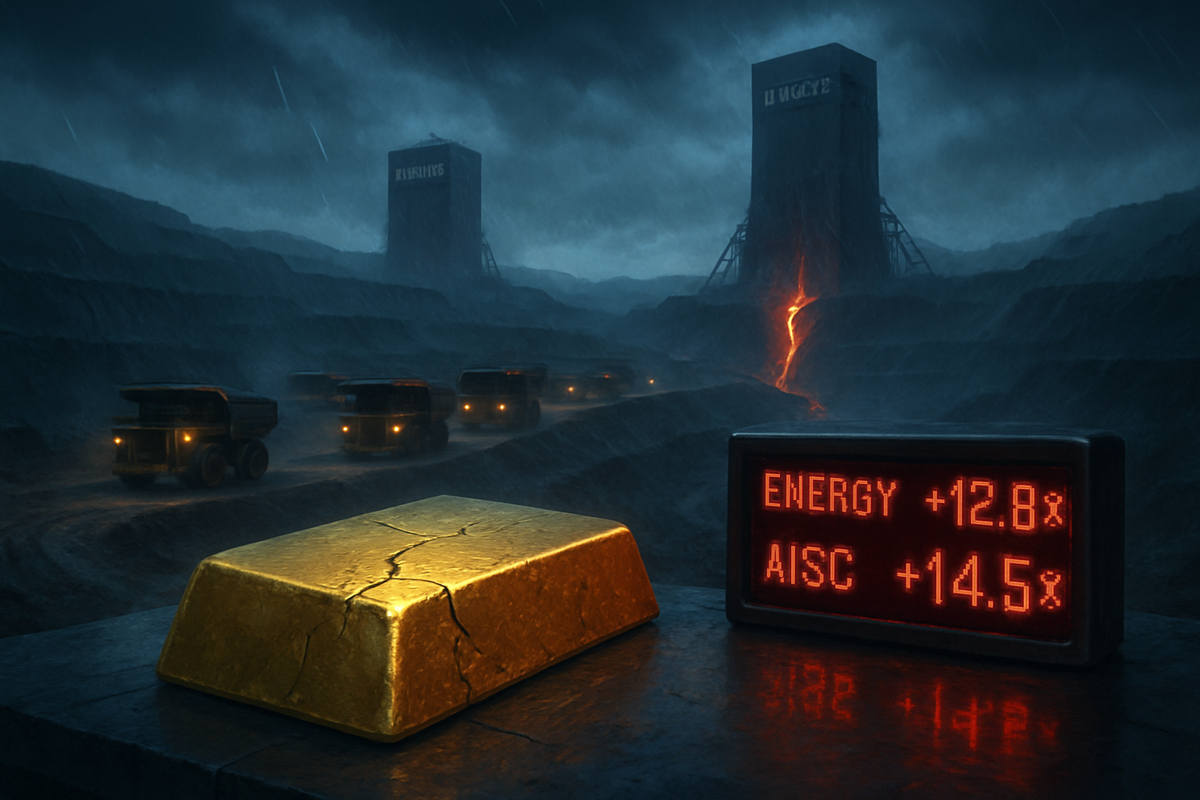

Newmont Corporation (NYSE: NEM) shocked markets earlier this quarter by officially designating 2026 as a "trough year." The company has lowered its gold production guidance to 5.3 million attributable ounces, a sharp 10.2% decline from its 2025 output. This reduction is largely the result of deliberate mine sequencing at Tier 1 assets like Boddington in Australia and Ahafo South in Ghana. While Newmont management argues this "sequencing" is necessary to unlock higher-grade ore in 2027, the market has reacted with skepticism, focusing instead on the immediate margin compression.

The most alarming metric for analysts is the spike in Newmont’s AISC to $1,680 per ounce. This represents a massive increase from the $1,358 average seen in 2025. The primary culprit is a global energy crisis triggered by "Operation Epic Fury" in late February—a series of Middle Eastern military strikes that led to the blockade of the Strait of Hormuz. For massive open-pit miners, the resulting 70% jump in the price of "red diesel" has been catastrophic. Every $10 increase in the price of oil currently adds roughly $15 to the AISC of major miners, effectively neutralizing the gains from higher gold prices.

A House Divided: The Nevada Gold Mines Legal War

Adding to the operational headwinds is a total breakdown in the relationship between Newmont and Barrick Gold (NYSE: GOLD). On February 3, 2026, Newmont issued a formal Notice of Default to Barrick regarding their Nevada Gold Mines (NGM) joint venture—the world’s largest gold-producing complex. Newmont, which holds a 38.5% stake, has accused Barrick, the 61.5% owner and operator, of "resource piracy."

The allegation centers on the Fourmile project, a high-grade deposit owned 100% by Barrick that sits adjacent to the JV’s Cortez operations. Newmont alleges that Barrick has been surreptitiously diverting shared NGM heavy equipment, technical staff, and administrative expertise to accelerate Fourmile’s development at the expense of joint venture production. The 30-day remedy period expired in March with no settlement, and the dispute has now entered a formal litigation phase in Nevada courts. This conflict has already derailed Barrick's planned North American asset spin-off, leaving the company's strategic roadmap in a state of paralysis as of April 2026.

Winners and Losers in the High-Cost Era

In this high-cost environment, the market is aggressively rotating capital toward more agile and cost-efficient "senior" miners. Agnico Eagle Mines (NYSE: AEM) has emerged as the clear winner of early 2026. With an AISC guidance of just $1,475 per ounce and a focus on low-risk jurisdictions like Canada and Finland, Agnico Eagle has managed to preserve its margins. Its sophisticated diesel hedging program has shielded it from the worst of the energy-driven inflation that has hamstrung Newmont and Barrick.

Conversely, the "Big Two" are the primary losers in the eyes of momentum investors. Since their January 2026 peaks, Newmont and Barrick shares have fallen by 15.4% and 24.5%, respectively. While they remain slightly above their 2025 lows, they are severely underperforming the 52-week highs set just four months ago. Other beneficiaries include mid-tier players like Orla Mining (NYSE: ORLA) and Greatland Gold, which have been picking up "non-core" assets at bargain prices as Newmont attempts to divest $4.5 billion in property to shore up its balance sheet during this transition year.

Broader Industry Trends and the Energy Trap

The challenges facing the gold majors highlight a broader industry shift: the era of "production at any cost" is over. The "Golden Squeeze" of 2026 has exposed the vulnerability of the world’s largest mines to global energy supply chains. For years, miners focused on consolidation to gain scale, but the current crisis suggests that extreme scale may be a liability when energy prices decouple from metal prices.

This situation echoes the 2012-2013 mining bust, where high costs eventually led to massive write-downs across the sector. However, the 2026 scenario is unique because gold prices remain near all-time highs; the crisis is purely operational and geopolitical. Regulatory scrutiny is also increasing, as the Nevada litigation has prompted calls for greater transparency in how joint ventures manage shared resources and "fenced-off" assets like Fourmile.

Looking Ahead: A 2027 Rebound or Continued Friction?

The short-term outlook for Newmont and Barrick remains clouded by the pending court dates in Nevada, with preliminary hearings for the NGM dispute scheduled for May 2026. If the court finds in favor of Newmont, it could force a massive restructuring of how the Nevada assets are managed, potentially leading to a forced sale or a change in operatorship. Long-term, Newmont’s "trough year" strategy assumes a significant production rebound and a return to lower costs in 2027, but this pivot relies entirely on energy prices stabilizing.

Market participants should prepare for continued volatility. Until the energy-driven AISC spike is contained or the Nevada dispute is settled, the "Big Two" are likely to remain laggards. Investors will be watching for any signs of a settlement in the NGM case, as well as the progress of Newmont’s divestiture program. A successful sale of remaining non-core assets could provide the cash cushion needed to weather the high-cost storm and prepare for the promised 2027 recovery.

Summary of the 2026 Gold Market Outlook

The first quarter of 2026 has been a humbling period for the world’s gold giants. Newmont's pivot to a "trough year" and the subsequent spike in AISC to $1,680 have signaled that even with gold at historic highs, profitability is not guaranteed. The legal battle over Nevada Gold Mines further complicates the narrative, suggesting that internal friction may be just as damaging as external inflation.

Moving forward, the market is likely to reward "operational excellence" and geographic focus over sheer size. While Newmont and Barrick remain massive cash-flow engines, their ability to navigate this period of margin compression and legal warfare will determine if they can regain their 2025-era momentum. For now, the "Golden Squeeze" continues to dominate the headlines, and investors should remain cautious as the industry's leaders fight a war on two fronts: one against rising costs and one against each other.

This content is intended for informational purposes only and is not financial advice.