Survey of 1,500 early-stage companies shows AI adopters are hiring more, more confident, and more likely to be actively scaling in 2025

Mercury, the fintech more than 200K ambitious companies and entrepreneurs trust with their finances, today released The New Economics of Starting Up. The data report, based on a survey of 1,500 early-stage founders and executives across the U.S., offers a detailed look at how early-stage companies – from professional services to financial services, manufacturing, ecommerce, tech, and more – are raising, spending, and hiring in 2025.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20250819036939/en/

Mercury data shows AI is driving hiring, not replacing it

As economic conditions shift and AI reshapes how businesses operate, early-stage founders are adapting. Top findings from the report reveal:

- Despite 89% of respondents citing general economic uncertainty as a top concern, 87% said their confidence in their company’s financial prospects has improved since 2024.

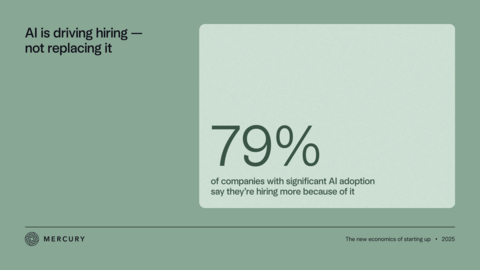

- And among startups with significant AI adoption, 79% say they’re hiring more because of AI.

A closer look at the data reveal key themes including:

AI-forward companies are leading the charge.

Founders who’ve embraced AI aren’t just feeling better — they’re behaving differently. Among companies with significant AI adoption, 60% said their confidence in financial prospects had “significantly improved” compared to 2024, versus just 28% of non-AI adopters.

AI-forward companies were also:

- 3x more likely to be actively scaling their teams

- 2x more likely to be seeking larger funding rounds

Far from replacing jobs, AI seems to be helping founders grow their teams:

- 68% of companies using AI are actively scaling team size

- 79% of significant AI adopters are hiring more because of AI

- AI-adopting companies report increased hiring across growth-oriented roles — including business development (44%), sales (43%), marketing (42%), customer service (42%)

The default route in funding is not necessarily VC money – even in tech.

Startups are stacking capital sources and embracing funding flexibility. While self-funding or “bootstrapping” remains the most common capital source (61%), founders are increasingly combining funding types. Across industries, companies reported drawing on business loans (47%), revenue-based financing (41%), and angel investments (22%) — with venture capital showing up, but not dominating, at 25%.

Tech companies were far more likely to have raised larger rounds, with 10% raising over $20M in their last round, compared to just 3-4% raising that amount across other industries. Yet overall, round sizes for these early-stage companies generally skewed small. Companies using four or more funding sources and raising VC were 40% more likely to report a last round over $5M, compared to just 15% of companies with just one source of funding.

Two-thirds of respondents said they’ve changed their capitalization strategy in the past year — with younger companies more likely to seek larger rounds to fuel growth, and more established companies emphasizing extending runway between rounds and exploring alternative financing.

Early-stage companies are building lean paths to growth.

Among companies bringing in $10M+ in annual revenue, half had raised $5-20M rounds — but just 9% had raised over $20M. On the other end of the spectrum, nearly half (49%) of companies with less than $1M in revenue raised under $1M. This suggests these founders may be finding alternative paths to profitability — or simply operating leaner.

There were a few sharp patterns across industries when it came to growth:

- Retail seems to follow a “scale fast or fail fast” trajectory. Among companies generating over $1M in annual revenue, 35% were at least five years old — compared to just 8% of their sub-$1M peers.

- Professional services showed something similar, with 32% of $1M+ companies clocking in at 5+ years old, versus just 16% of sub-$1M firms. That tracks with the slower, relationship-driven growth curve of many agency or consultancy models.

- Ecommerce, however, told a different story. Among those hitting $1M+ in annual revenue, 55% were just 2–5 years old — but only 16% had made it past year five. That could signal rapid scaling success — but could also suggest some companies burn out before reaching long-term maturity.

- Financial services stood out for steady scaling: 56% of $1M+ companies in this group were 2–5 years old. That might suggest a more predictable revenue trajectory once product-market fit clicks.

Entrepreneurs say costs were up – and many expect to spend more in the year ahead.

A majority of respondents reported that in the last 12 months, costs were up across all areas we asked them about:

- 71% customer acquisition

- 69% tech infrastructure

- 65% talent and acquisition retention

- 63% access to capital

- 59% regulatory and compliance

- 57% office / physical space

A full 79% of respondents expect to spend more in the year ahead, with growth opportunity as the number one reason cited. Respondents were most likely (73%) to be somewhat or significantly increasing spend on AI tools and technology.

Contractors are key to scaling.

Freelancers and consultants are a strategic lever: 61% of early-stage companies surveyed said their company is very reliant or reliant on contract talent. That number climbs among companies that have adopted AI.

- AI adopters are 4x more likely to be very reliant on contractors vs. non-AI adopters

- Entrepreneurs who said their company’s AI adoption was significant are 2x as likely to use contractors to access global talent than non-AI adopters

Despite headwinds, optimism endures.

In a volatile economic climate, early-stage companies are adapting. The entrepreneurs leading them are deploying flexible funding strategies, embracing AI to unlock new efficiencies, and investing in people and technology that can help them grow.

Their confidence is high, their tools are evolving, and their playbooks are changing.

You can read the full report on the Mercury blog.

Methodology: Data is based on a Mercury-commissioned survey of 1,500 U.S.-based early-stage company founders and executives in May 2025 to understand how economic conditions, tech adoption, and other factors are reshaping startup finances and strategies. Data points are rounded up or down to the nearest single digit, which means some things won’t add up to 100%.

ABOUT MERCURY

Mercury is the fintech that brings all the ways people and businesses use money into a single product that feels extraordinary to use. Mercury gives more than 200K ambitious companies, from small businesses to growth stage enterprises, the banking*, credit cards*, and software they need to power all their financial workflows. To learn more, visit Mercury.com.

*Mercury is a financial technology company, not a bank. Banking services provided through Choice Financial Group, Column N.A., and Evolve Bank & Trust; Members FDIC. The IO Card is issued by Patriot Bank, Member FDIC, pursuant to a license from Mastercard®.

View source version on businesswire.com: https://www.businesswire.com/news/home/20250819036939/en/

The New Economics of Starting Up report, based on a survey of 1,500 early-stage founders and executives across the U.S., offers a detailed look at how early-stage companies are raising, spending, and hiring in 2025.

Contacts

Nic Corpora

press@mercury.com