Hard-disk drives have stepped out of the shadows and into the spotlight as artificial intelligence (AI) is pushing data demand into overdrive. Prices have firmed, orders keep piling up, and supply now walks a tightrope. Yet Morgan Stanley (MS) analyst Erik Woodring believes the market still underestimates the real muscle behind names like Seagate Technology Holdings plc (STX) and Western Digital Corporation (WDC).

Woodring sees the runway extending further than most expect. He projects steady hard disk drive (HDD) demand with potential shortages lingering through 2028, backed by relentless hyperscale spending and clearer customer visibility. Pricing, too, looks set to hold firm into 2027.

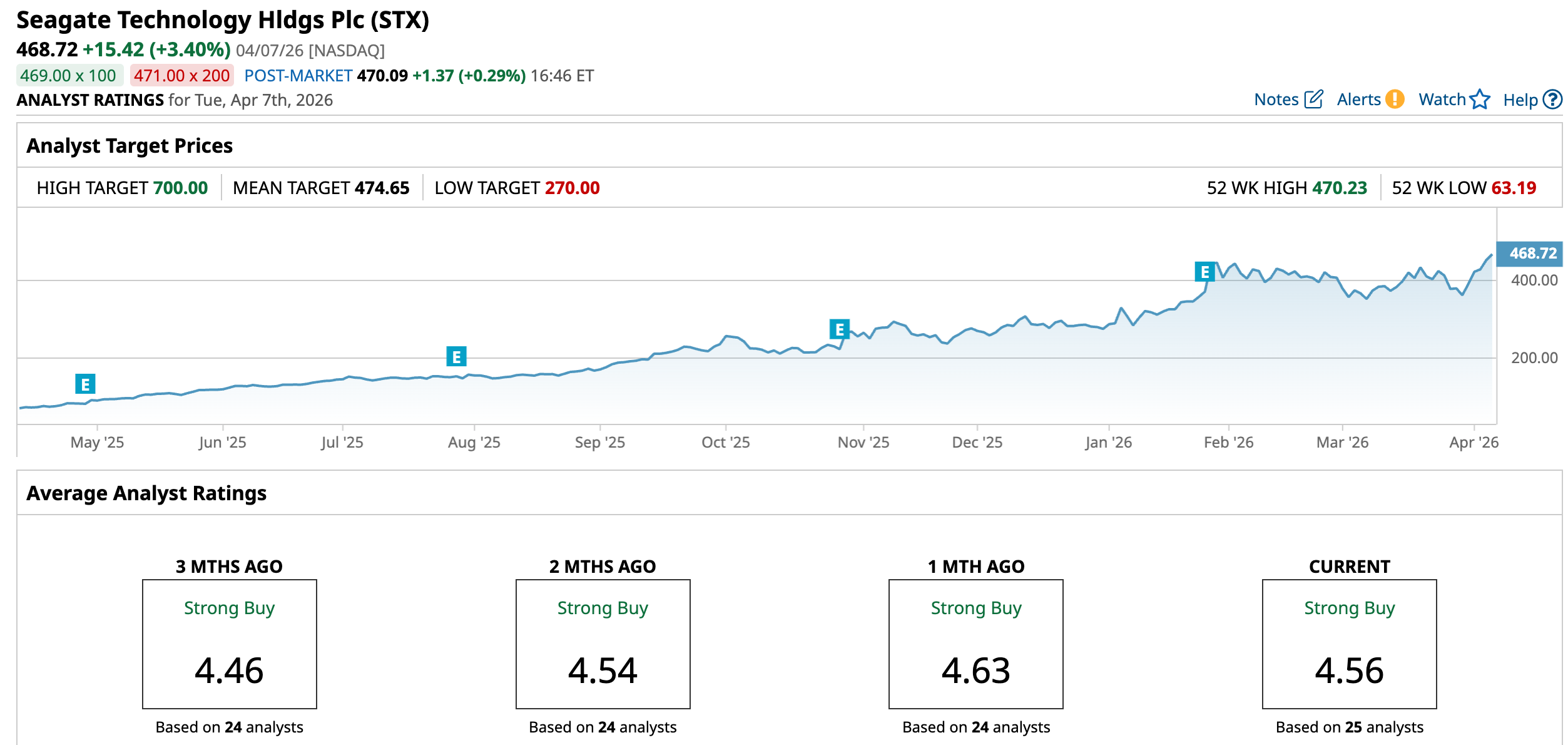

Seagate, the leading innovator of mass-capacity data storage, has begun to pull ahead in this race. Its stock climbed 5.58% on Monday, April 6, to close just above $453, marking a record high after Woodring named it the top pick in Information Technology (IT) hardware.

The optimism spilled over into peers like Western Digital, Micron Technology (MU), and Sandisk Corporation (SNDK), all of which joined the day’s top gainers in the S&P 500 Index ($SPX).

At first glance, Seagate’s strong run may suggest the easy money has already been made. Woodring sees it differently. The stock has actually lagged Western Digital on a relative basis, leaving room to catch up. More importantly, HDDs sit at the heart of AI infrastructure spending. They act as a bottleneck for cloud providers, and in markets like this, bottlenecks often translate into pricing power and margin expansion.

With several of Western Digital’s catalysts already in the rearview mirror, Seagate now looks better positioned to widen margins over the next 12 months. The cycle is turning, with Seagate set to expand its growth prospects.

About Seagate Stock

Since 1978, Singapore-based Seagate Technology Holdings plc (STX) has done the heavy lifting behind the digital economy, designing storage solutions that keep data flowing where it needs to go. It builds high-capacity hard drives and fast solid-state drives (SSDs) that serve enterprises, gamers, creators, and everyday users who never seem to run out of things to store.

With a market cap of about $98.9 billion, Seagate anchors itself firmly in the data infrastructure chain. Its systems handle vast enterprise workloads, support legacy environments, and power devices from laptops to streaming platforms. Through its Lyve platform, the company moves data seamlessly from edge to cloud, helping businesses stay nimble as volumes scale.

Seagate’s shares have rewarded investors handsomely. The stock surged 582.67% over the past 52 weeks and added 108.31% over the last six months, reflecting a powerful re-rating as storage demand is tightening.

The rally still has fuel in the tank. Shares remain up 70.2% year-to-date (YTD) and have jumped 29.33% in just the past five trading sessions, with fresh analyst optimism adding momentum.

From a valuation standpoint, STX stock is trading at 36.12 times forward adjusted earnings and 8.83 times sales, both comfortably above industry averages. The market has assigned a premium to the stock, pricing in sustained demand tailwinds.

Income adds a steady, if modest, layer to the thesis. The company pays an annual dividend of $2.96 per share, offering a 0.69% yield. It is scheduled to pay its most recent dividend of $0.74 per share on April 8 for shareholders on record as of March 25.

Seagate Surpasses Q2 Earnings

On Jan. 28, Seagate delivered its Q2 fiscal year 2026 financial results, wherein revenue grew 21.5% yea-over-year (YOY) to $2.83 billion, clearing the $2.75 billion analyst estimate. Adjusted EPS came in at $3.11, ahead of the $2.84 Street forecast and up 53.2% YOY.

Non-GAAP income from operations reached $901 million, up 67.5% YOY, while non-GAAP net income rose 62.1% YOY to $702 million. Cash flow adds another feather in its cap. Capital expenditures stood at $116 million, or about 4% of revenue, with full-year fiscal 2026 guidance steady at 4% to 6%.

Free cash flow climbed 304.7% from the previous year’s period, the highest in eight years. Cash reserves crossed $1 billion, backed by total liquidity of $2.3 billion, giving the company room to maneuver without breaking stride.

Operational trends show where the wind blows. Nearline drive capacity rose 22% YOY, approaching 23 terabytes per drive, with cloud customers pushing averages even higher. Looking ahead, Seagate’s management expects Q3 fiscal year 2026 revenue to land at $2.90 billion, give or take $100 million, with non-GAAP diluted EPS of $3.40, plus or minus $0.20.

Analysts, for their part, are reading the same tea leaves. They expect Q3 fiscal 2026 EPS to climb 95.2% YOY to $3.26. For the full fiscal year 2026, the bottom line is projected to grow 63.8% from the prior year to $11.89, followed by another 53.3% jump to $18.23 in fiscal year 2027.

What Do Analysts Expect for Seagate Stock?

Morgan Stanley raised its price target on STX stock to $582 from $468, keeping an “Overweight” rating in place. At the same time, Mark Newman from Bernstein lifted his price target from $500 to $620 and maintained an “Outperform” call.

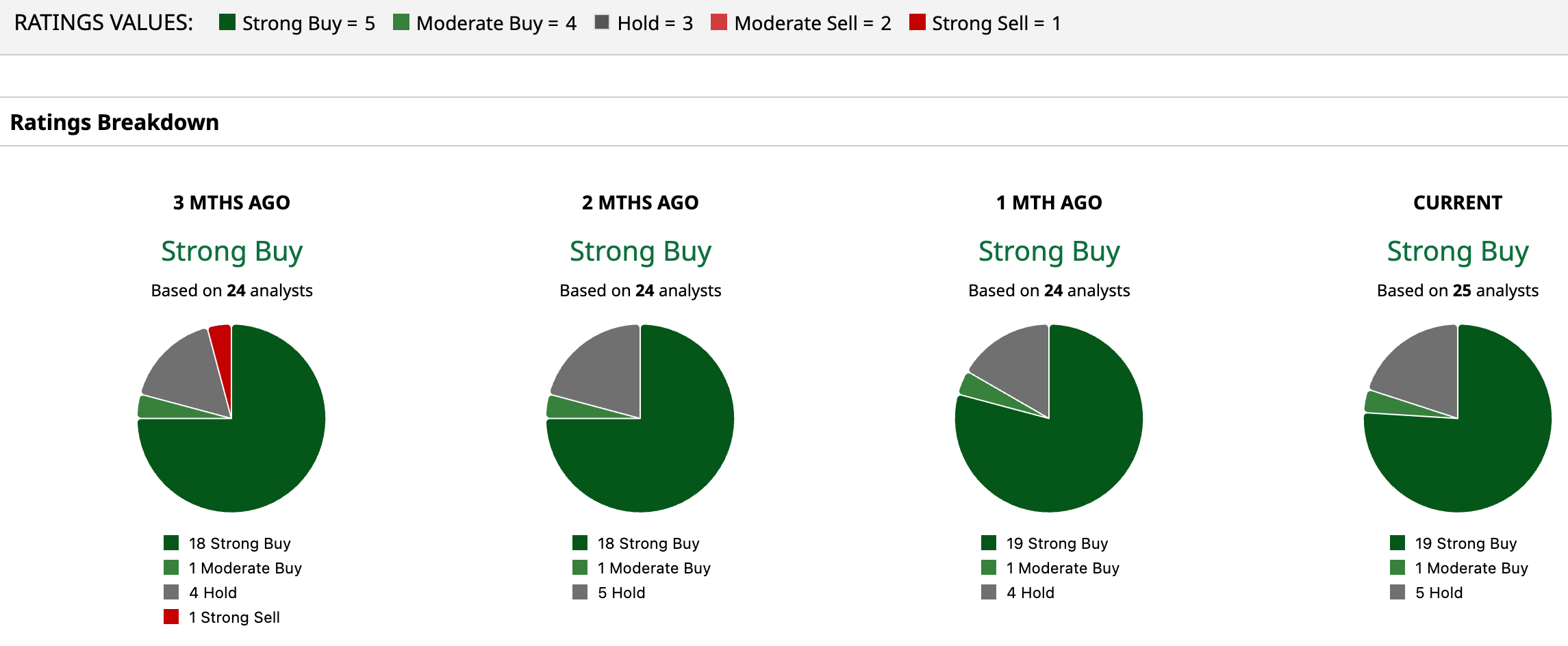

The broader analyst community leans in the same direction. Of the 25 analysts covering the stock, 19 rate it a “Strong Buy,” one calls it a “Moderate Buy,” and five sit on “Hold.”

The mean price target of $474.65 sits almost neck and neck with current levels, implying a modest upside of 1.27%. Yet the Street-high target of $700 opens the door to a potential gain of roughly 49.3% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear United Airlines Stock Fans, Mark Your Calendars for April 21

- From $575 Million IPO to Penny Stock in Less Than a Decade: Is There Any Hope Left for This Stock at 52-Week Lows?

- Want to Ride the Rally? Here’s the Ultimate ‘Go Big or Go Home’ Strategy for Your Stock Portfolio.

- AI Stocks Are Splitting. Here’s 1 Winner and 1 Comeback Play