The global economy was already walking a tightrope, balancing tariffs, post-pandemic debt, and stubborn inflation. Then came the shockwave of the Iran war oil shock. Oil prices surged, gas bills climbed, and suddenly, everyday spending felt even heavier. Households began pulling back, prioritizing essentials over wants.

Models from Moody’s Analytics pushed recession odds close to a coin flip, while Oxford Economics warned that prolonged high oil prices could tip growth over the edge. Add layoffs into the mix and a cooling job market for fresh graduates, and the mood shifts fast – cautious, uncertain, value-driven. Consumers are not just spending less, but thinking harder about every dollar.

And that’s where the golden arches quietly step in.

McDonald’s Corporation (MCD) is leaning into this moment, expanding its “McValue” menu with sharper pricing, such as items under $3, bundled meals starting at $4 or $5, and familiar staples repositioned as budget-friendly comfort. It's not just about food, but about meeting consumers exactly where they are – watching wallets and seeking small wins.

For a company that has paid dividends for nearly five decades, the strategy feels familiar. But in a world tilting toward frugality, does this renewed focus on value strengthen McDonald’s ability to weather tougher times, and make MCD a recession-proof pick now?

About McDonald’s Stock

Chicago-based McDonald’s Corporation, founded in 1940, is the world’s go-to fast-food chain. With over 40,000 restaurants across more than 100 countries, it serves everything from its iconic burgers and fries to breakfast favorites and coffee.

Boasting a market capitalization of approximately $220 billion, McDonald’s runs largely on a franchise model, with over 90% of its outlets operated by partners. That keeps the business lean while driving steady cash flow. The company continues to evolve with digital ordering, delivery, and value-focused menus, staying relevant as consumer habits shift. Despite changing tastes and rising costs, McDonald’s remains a global staple – quick, familiar, and consistently in demand.

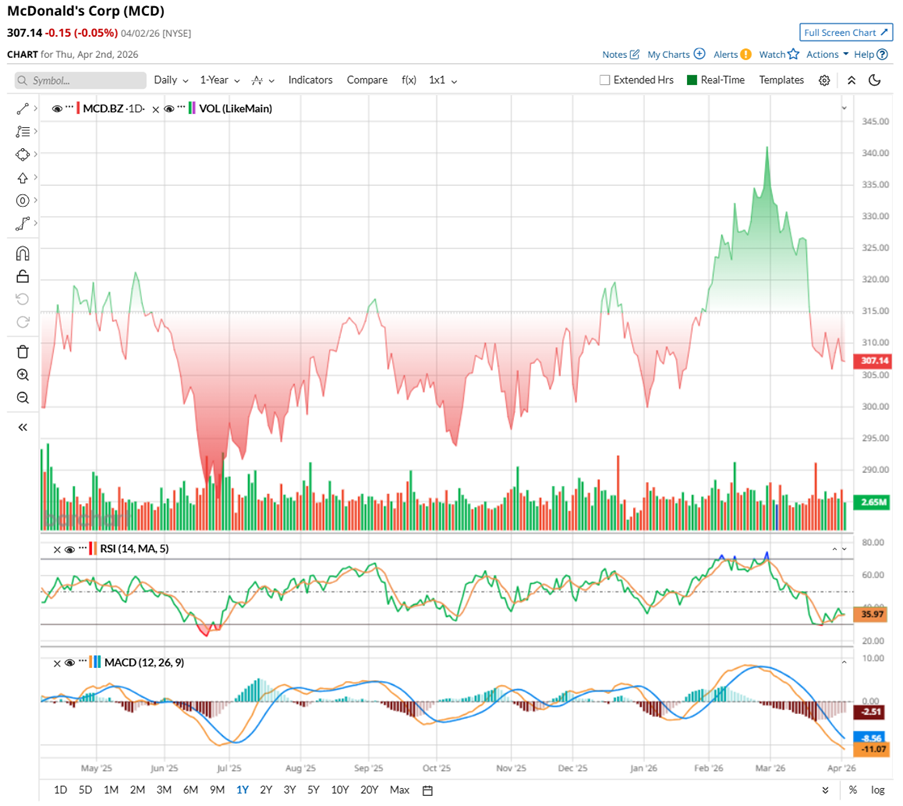

Shares of the fast-food giant have been on a slow simmer in 2026, inching marginally higher before recently losing some heat. After touching a 52-week high of $341.75, the stock has pulled back 9%, with an 5.58% dip over the past month alone.

The pressure is not coming from one place. Investors are weighing softer consumer spending and concerns around menu pricing limits. Even the longer-term impact of GLP-1 weight-loss drugs are potentially changing eating habits.

Still, the story is not entirely cold. Trading volumes have picked up, hinting at renewed investor interest, while the 14-day RSI has rebounded to around 40.87 from oversold levels, suggesting selling pressure may be easing.

But caution lingers beneath the surface. The MACD line has crossed below the signal line, typically a bearish sign, and the negative histogram bars point to weakening momentum. For now, MCD stock feels like it’s in a pause – cooling off, but not entirely out of flavor.

From a valuation lens, MCD is not exactly sitting on the value menu, but it's not overpriced either. The stock is currently priced at 23.23 times forward adjusted earnings and 7.66 times sales, slightly below its own five-year averages, suggesting the pricing has cooled a bit.

That said, compared to the sector peers, it still carries a premium price tag. Investors are essentially paying extra for consistency, scale, and a brand that rarely goes out of taste. It may not be a deep discount pick, but for many, it is like a reliable signature meal, priced a bit higher, yet trusted to deliver through changing market appetites.

Extending that steady valuation story, McDonald’s brings reliable income for investors. The company has raised its dividend for 49 consecutive years, reflecting remarkable consistency across economic cycles and securing its status among the elite “Dividend Aristocrats.”

On March 17, the company paid a quarterly dividend of $1.86 per share, or $7.44 annually, translating to a yield of about 2.42%, well above the broader State Street SPDR S&P 500 ETF Trust’s (SPY) 1.13% yield. Importantly, the payout ratio sits at 58.8%, leaving enough room to sustain and potentially grow distributions ahead.

For investors, it is not just about returns today, but a steady stream that keeps coming, even when the broader market appetite turns uncertain.

A Snapshot of McDonald’s Better-Than-Expected Q4 Numbers

On Feb. 11, McDonald’s reported stellar Q4 earnings results, generating $7 billion in revenue, which represents a growth of 9.7% year-over-year (YOY). The top line beat Wall Street’s projections. Growth was not coming from just one corner of the business – it was broad-based. Company-operated restaurants’ sales came in at $2.54 billion, up 10% annually, while franchise-operated locations brought in $4.3 billion in sales, rising 9% YOY. Even the smaller “other revenues” line jumped 35% to $162 million.

Across the globe, the demand picture looked healthy. Global comparable sales rose 5.7% YOY, supported by more customers walking through the doors and spending a bit more. In the U.S., sales climbed 6.8%, helped by effective promotions and value-focused offerings. The International Operated Market (IOM) segment followed suit, with strong performances led by the U.K., Germany, and Australia.

Non-GAAP EPS in Q4 grew 10.2% YOY to $3.12, slightly ahead of forecasts, while operating income rose 10% to $3.15 billion. The company generated solid cash and equivalents of $774 million as of Dec. 31, 2025, with free cash flow reaching $7.2 billion for 2025, giving it room to invest and reward shareholders, even as long-term debt stood at $40 billion.

What stands out, though, is how McDonald’s is adapting to a more cautious consumer. From discounted combo meals to the McValue menu and the return of Snack Wraps, the company has leaned into affordability. These moves are already helping it win back lower-income customers, reinforcing its reputation as a go-to for value.

Looking ahead, McDonald’s is projecting steady growth with a few helpful tailwinds. Management expects currency movements to give a slight lift to 2026 EPS. It’s not a guaranteed boost, though, as exchange rates can shift throughout the year. So, the company is treating this as a moving piece rather than a fixed advantage.

Where the strategy feels more concrete is expansion. After beating its restaurant opening targets in 2025, with gross openings of about 2,275 restaurants and net openings of 1,880, McDonald’s is stepping on the gas.

The plan for 2026 includes around 2,600 new restaurants globally, with a balanced mix, about 750 in the U.S. and IOM segments, and a much larger push across high-growth regions. In fact, over 1,800 openings are expected in international development markets, including a significant buildout in China.

All of this keeps the company on track toward its long-term goal of 50,000 locations by 2027. Net additions of anticipated 2,100 restaurants in 2026 should translate into about 4.5% unit growth. To support this expansion, McDonald’s is planning CapEx between $3.7 billion and $3.9 billion, with most of it going into new stores and strengthening its core markets.

Analysts tracking the company expect its EPS to be $13.23, up 8.44% YOY for fiscal 2026, and then surge by another 9.1% annually to $14.43 in fiscal 2027.

What Do Analysts Expect for MCD Stock?

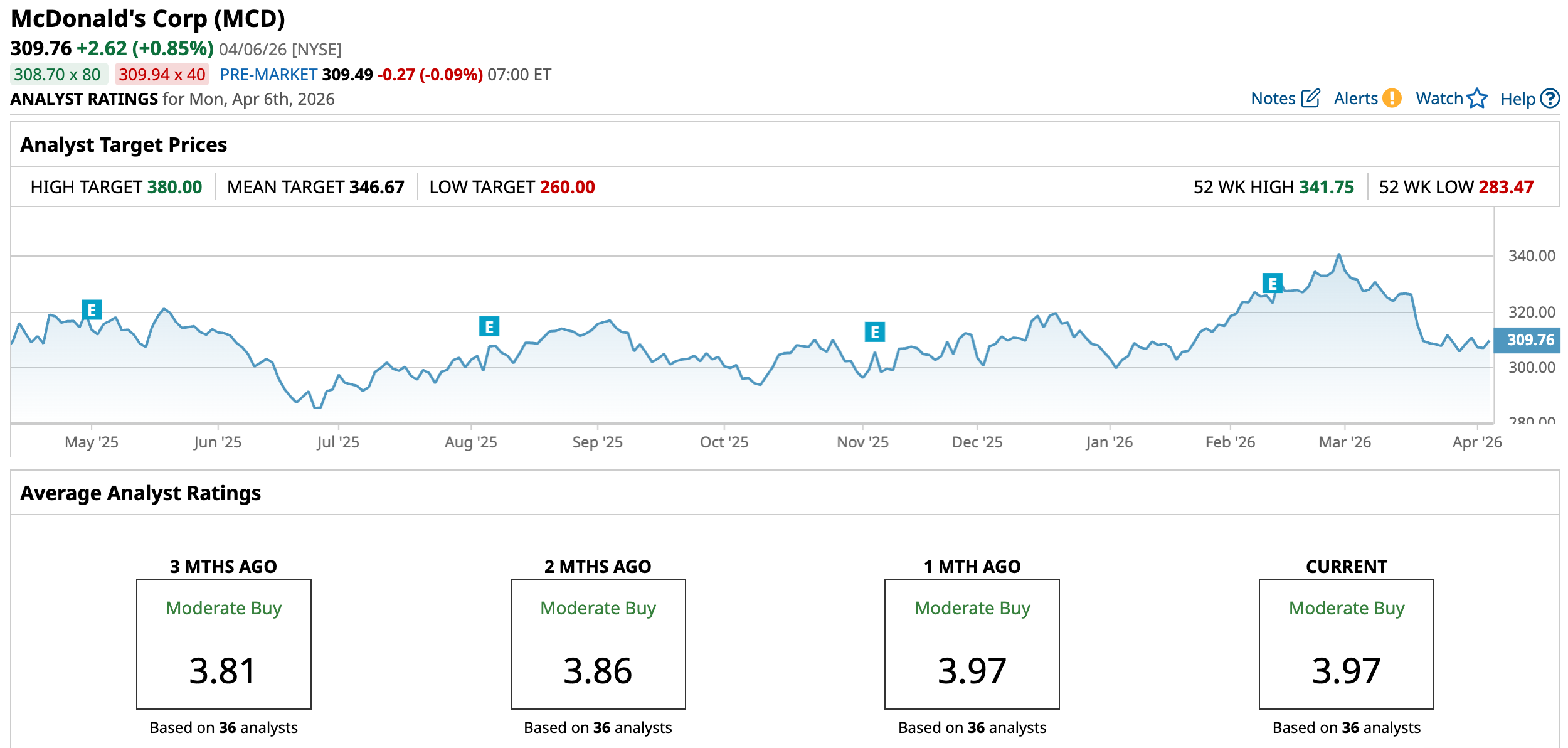

Bullish sentiment is still cooking on MCD, even though the stock has cooled off over the past year. For instance, Tigress Financial lifted the price target last month to the Street’s highest of $385, implying about 25.4% upside potential, while keeping a “Buy” rating.

The brokerage firm anticipates growth coming from a mix of global expansion, digital and loyalty strength, AI-led efficiency gains, and its franchise-heavy model, all working together to drive steady revenue and cash flow in the years ahead.

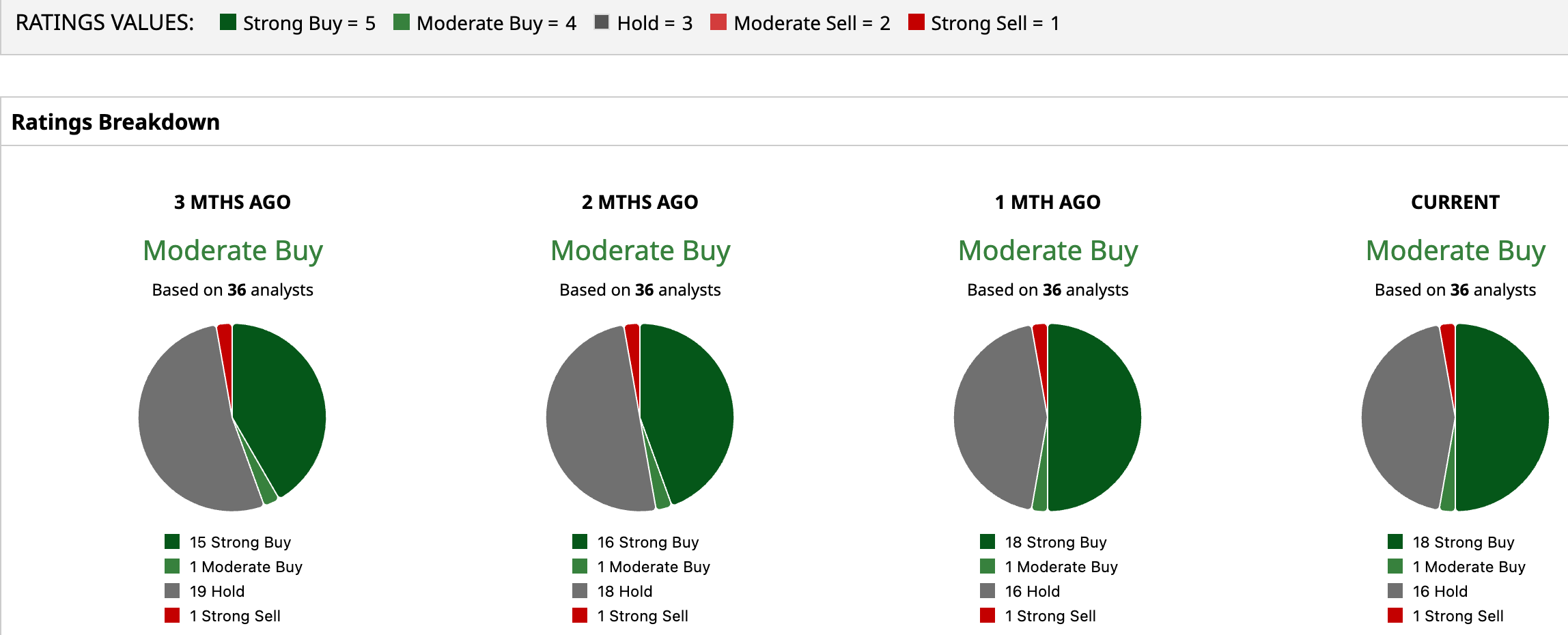

Overall, sentiment on MCD remains optimistic, but with a dash of caution. The stock has a consensus rating of “Moderate Buy.” Out of 36 analysts, 18 recommend a “Strong Buy,” one advises a “Moderate Buy,” 16 are playing it safe with a “Hold” rating, and the remaining one has a “Strong Sell” rating. Its average price target of $346.67 implies upside potential of 11.9%.

Final Thoughts on MCD

At a time when every dollar counts, McDonald’s is offering simple, affordable meals that keep customers coming back. That focus on value feels especially relevant now, as consumers grow more cautious with spending.

MCD has not been immune to pressure, and concerns around demand and shifting habits still linger. But the foundation remains steady. Strong cash flows, a dependable dividend, and unmatched global scale continue to anchor the story.

With value front and center, along with steady expansion and digital growth, McDonald’s looks less like a risky bet and more like a reliable name. It may not be fully recession-proof, but it is built to hold up when conditions get tough.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Raytheon Is a Top Defense Stock to Buy Amid the Iran War, But It Will Also Benefit From a Ceasefire. Here’s How.

- 3 Dividend Kings With 50+ Years of Raises Are Trading at a Huge Discount. Analysts Say Buy Before They Rebound

- The ‘McValue’ Menu Is Getting Bigger. Does That Make McDonald’s a Top Recession-Proof Stock to Buy Now?

- Dell Announced Major AI-Driven Layoffs in March 2026. What Comes Next for Dividend-Paying DELL Stock?