It appears that Dell Technologies (DELL) is once again in the news, but this time it isn't about good news. The company announced in its latest filing for the fiscal year ended Jan. 30, 2026, that headcount shrank by approximately 11,000 jobs to stand at around 97,000, down from 108,000 in fiscal year 2025 and 120,000 in fiscal 2024. Reuters reported that the firm has curbed its hiring efforts in order to save costs and modernize itself amid the changing technological landscape. Now, the logical question for investors would be, is this bad news or simply growing pains for an AI-focused company?

The timing is important. Dell Technologies is making those layoffs when the entire tech sector is doing the exact same thing, not because there is no demand, but because priorities have shifted. Challenger, Gray & Christmas estimated that tech led all other sectors in terms of job cuts made in March and singled out Dell as a major contributor. Meanwhile, the tech sector just experienced its worst quarter since 2022; therefore, investors are rewarding companies that deliver growth despite the challenging conditions. From this perspective, Dell's narrative doesn't look bad at all; instead, it seems like it is reallocating resources in favor of building a solid AI infrastructure.

About Dell Stock

Dell Technologies is a large-cap technology company headquartered in Round Rock, Texas. It operates in various segments, including personal computing products, enterprise infrastructure products, software and services, storage solutions, networking, and AI-optimized servers. As of writing, it has a market capitalization of $112 billion.

The company's stock continues to perform well recently, and for all the right reasons. Shares were trading at $174.37 as of April 6 and were slightly off a 52-week high of $186.39 set earlier on March 26. Overall, within the last 52 weeks, DELL stock has increased by more than 140%, substantially outpacing a generally struggling stock market. This performance highlights why investors should view the stock as a tech winner, one that derives much of its value from being a beneficiary of rapidly expanding AI infrastructure.

Even better, the stock isn't even expensive considering its impressive growth rate. DELL currently trades at 17.9x, 14.3x, and 0.69x trailing P/E, forward P/E, and PEG, respectively, with its stock price-to-sales ratio standing at approximately 1 times. This is quite cheap for a firm projecting growth rates of over 20%, especially for one with the potential to double its AI-optimized servers' revenue in the coming year.

Finally, the stock pays a decent dividend yield, allowing income investors to profit while waiting for further gains. Indeed, in mid-April, Dell increased its quarterly dividend to $0.63 per share, payable on May 1 to those shareholders who own shares as of April 21.

Dell Technologies Earnings Beat and More Focus on AI

Although layoffs have been receiving all the attention, it was the earnings results that really supported the stock's performance. Specifically, for its fiscal year 2026, the firm reported record-breaking total revenue of $113.5 billion, up 19% year-over-year (YoY), while its diluted EPS increased by 36% YoY to stand at $8.68, and non-GAAP EPS rose 27% YoY to $10.30. In Q4 alone, the firm delivered record-breaking revenue of $33.4 billion, up 39% YoY, and non-GAAP EPS of $3.89, an increase of 45% YoY.

As the figures above suggest, the stock has been enjoying strong support from the firm's enterprise and AI-related businesses. Speaking of which, Infrastructure Solutions Group revenue jumped 40% in full year 2026 to $60.8 billion. Fourth-quarter revenue saw even faster expansion, increasing by a staggering 73% YoY to $19.6 billion. Within that segment, AI-optimized server revenue surged 342% YoY in the fourth quarter to $9 billion.

Management added that during fiscal year 2026, Dell Technologies closed AI-optimized server orders worth more than $64 billion, shipped over $25 billion, and booked a record backlog of almost $43 billion worth of AI-related products. In other words, although the current quarter saw some impressive results, it wasn't a one-off event for the firm.

Regarding expectations, management projects a significant rise in revenues over the next twelve months, estimating 23% YoY growth to $140 billion, or a midpoint between $138 billion and $142 billion as guidance for fiscal year 2027. Further, AI-optimized servers' revenues are expected to be around $50 billion, up by 103% YoY, while non-GAAP EPS is projected to hit a mark of $12.90. In other words, yes, layoffs are a thing and terrible for those affected. However, they are done in order to trim costs and focus more on growing businesses, so this strategy makes perfect sense.

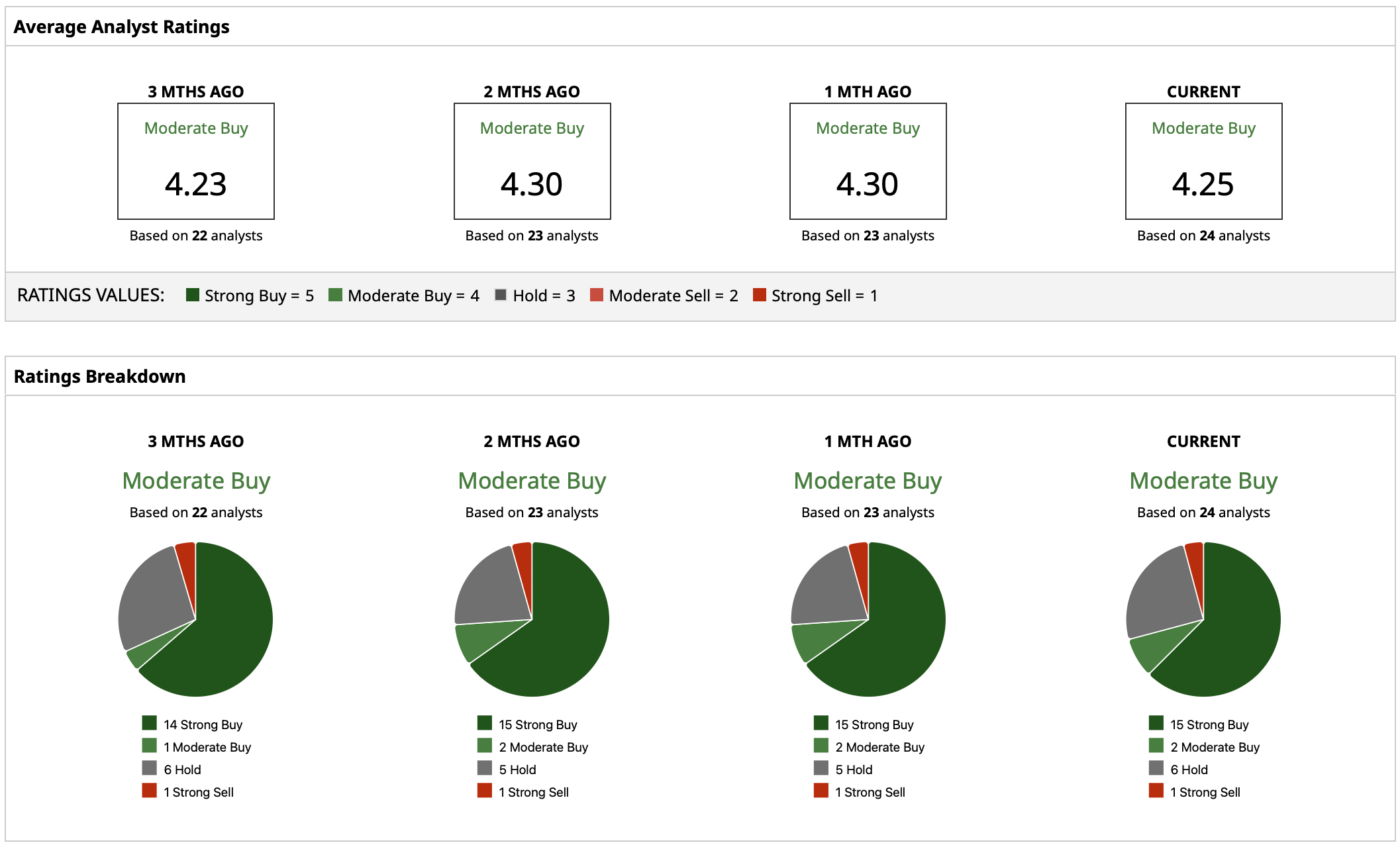

What Do Analysts Expect for DELL Stock?

DELL stock carries a "Moderate Buy" rating consensus with an average price target of $172.18, which implies a potential downside of 1.3% from the recent $174.37 close. Its low target price of $110 suggests a potential downside of 36.9%, whereas its high target price of $220 represents an upside potential of 26.2%.

On the date of publication, Yiannis Zourmpanos had a position in: DELL . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dell Announced Major AI-Driven Layoffs in March 2026. What Comes Next for Dividend-Paying DELL Stock?

- Dear Costco Stock Fans, Mark Your Calendars for May 1

- Comparing 2 Healthcare Giants: Which Dividend Aristocrat Will Keep Paying Out for Generations to Come?

- Sysco Just Announced a $29.1 Billion Acquisition and Wall Street Is Nervous. Can a 3% Dividend Sweeten the Deal?