Investors are piling into momentum trades, such as memory chip stocks like Western Digital Corporation (WDC), on news of the U.S.-Iran ceasefire deal. Memory chips have recently seen a significant increase in demand due to the need for memory and hard drives for artificial intelligence (AI) infrastructure.

Against this backdrop, UBS analysts expect DDR prices to go up 37% in the second quarter and NAND prices to rise 40%. However, peak memory contract pricing may be avoided through long-term agreements.

Should you consider investing in Western Digital’s stock in this situation?

About Western Digital Stock

Western Digital is a global leader in data storage technology, designing, manufacturing, and marketing a broad portfolio of storage devices and solutions that underpin computing across consumers, enterprises, and cloud data centers. The company’s core operations span hard disk drives (HDDs) and flash-based embedded storage, which it supplies to original equipment manufacturers (OEMs), cloud providers, and retail channels.

Western Digital has evolved its operations to become a dedicated storage infrastructure partner for AI-driven workloads, shifting from general-purpose storage to engineered solutions for training, inference, and massive-scale data lakes. Headquartered in San Jose, California, the company has a market capitalization of $114.86 billion.

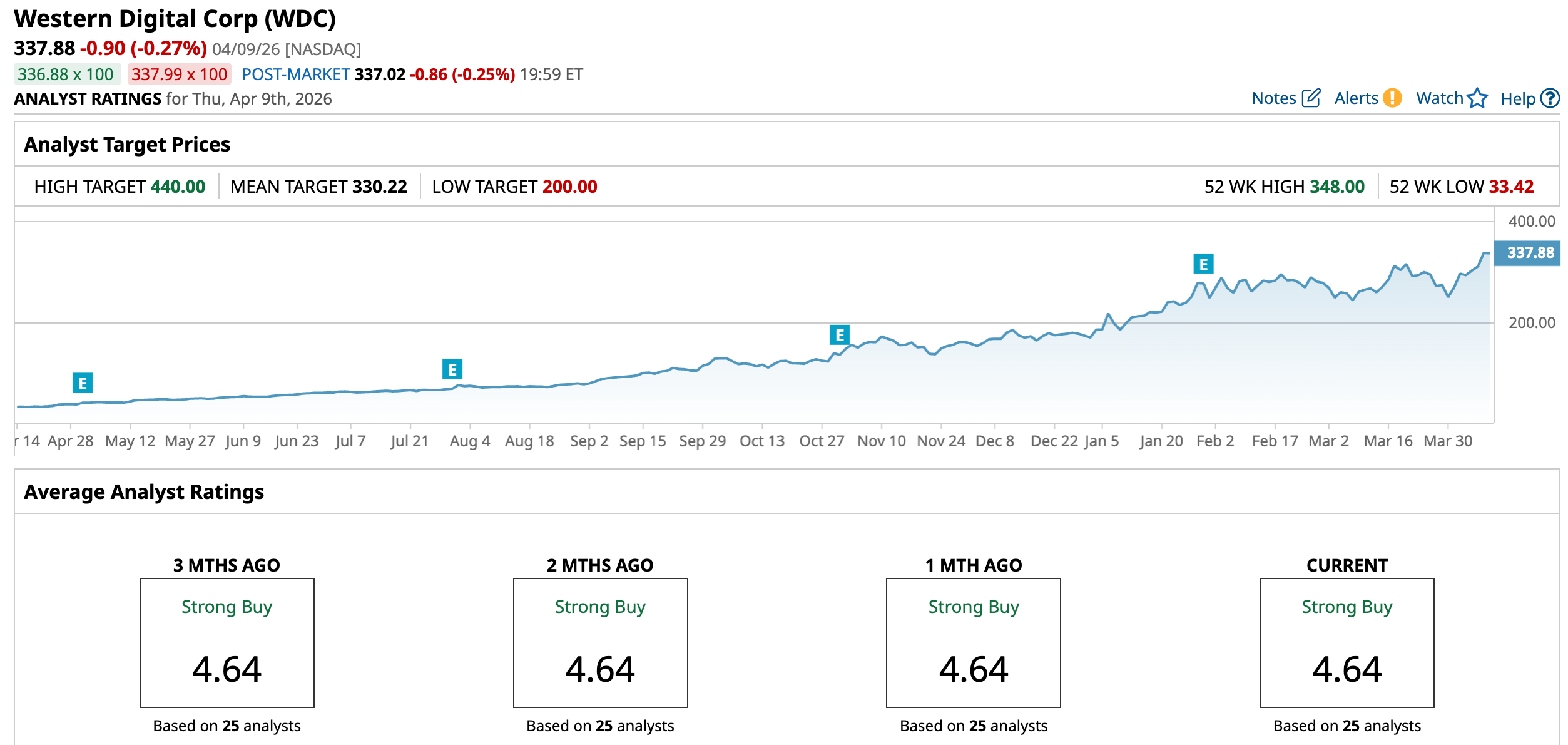

Data centers building AI infrastructure need enormous amounts of storage to train models. This creates a significant tailwind for Western Digital, making the stock look like a pure-play on AI infrastructure. This has also led the company’s share price to skyrocket. Over the past 52 weeks, the stock gained 830.8%, while it is up 96.13% year-to-date (YTD). It reached a 52-week high of $348 on Apr. 8 and is only down modestly from that level.

On a forward-adjusted basis, Western Digital’s price-to-earnings (non-GAAP) ratio of 36.72 times is higher than the industry average of 22.15 times.

Western Digital’s Q2 Earnings Reflect Strong Demand and Improved Margins

For the second quarter of fiscal 2026 (quarter ended Jan. 2), Western Digital’s revenue increased 25% year-over-year (YOY) to $3.02 billion, which was higher than the $2.95 billion that Wall Street analysts had expected. The company highlighted that its results were driven by cloud demand.

Western Digital’s non-GAAP gross margin inflated by 770 basis points YOY to 46.1%, while non-GAAP operating margin increased 930 basis points to 33.8%. Its non-GAAP EPS for the quarter was $2.13, up 78% YOY and surpassing the $1.95 that Street analysts had expected.

For the third quarter, Western Digital expects revenue of $3.20 billion, plus or minus $100 million, while non-GAAP EPS is projected to be $2.30, plus or minus $0.15. For the current fiscal year, Wall Street analysts expect the company’s EPS to be $8.50, indicating an 87.6% YOY increase, followed by a 66.8% growth to $14.18 in the following fiscal year.

What Do Analysts Think About Western Digital’s Stock?

Wall Street analysts have an overwhelmingly positive view of Western Digital’s prospects. This month, analysts at Morgan Stanley raised the stock’s price target from $368 to $380, while maintaining an “Overweight” rating. Analyst Erik Woodring believes that HDD demand continues to strengthen. Moreover, Morgan Stanley’s supply-and-demand tracker now implies shortages through 2028.

In February, Western Digital’s stock was reaffirmed with an “Outperform” rating and a $325 price target by Wedbush analyst Matt Bryson. The reaffirmation suggests steady potential for the stock. Mizuho analyst Vijay Rakesh also maintained an “Outperform” rating and raised the price target to $340 from $325.

Cantor Fitzgerald analysts also maintained an “Overweight” rating on Western Digital and raised the price target to $420 from $325. Analysts at the firm highlighted that WDC’s expected growth and profitability are “significantly better” than previously expected. They also see EPS for CY2028 ranging from $19 to $32.

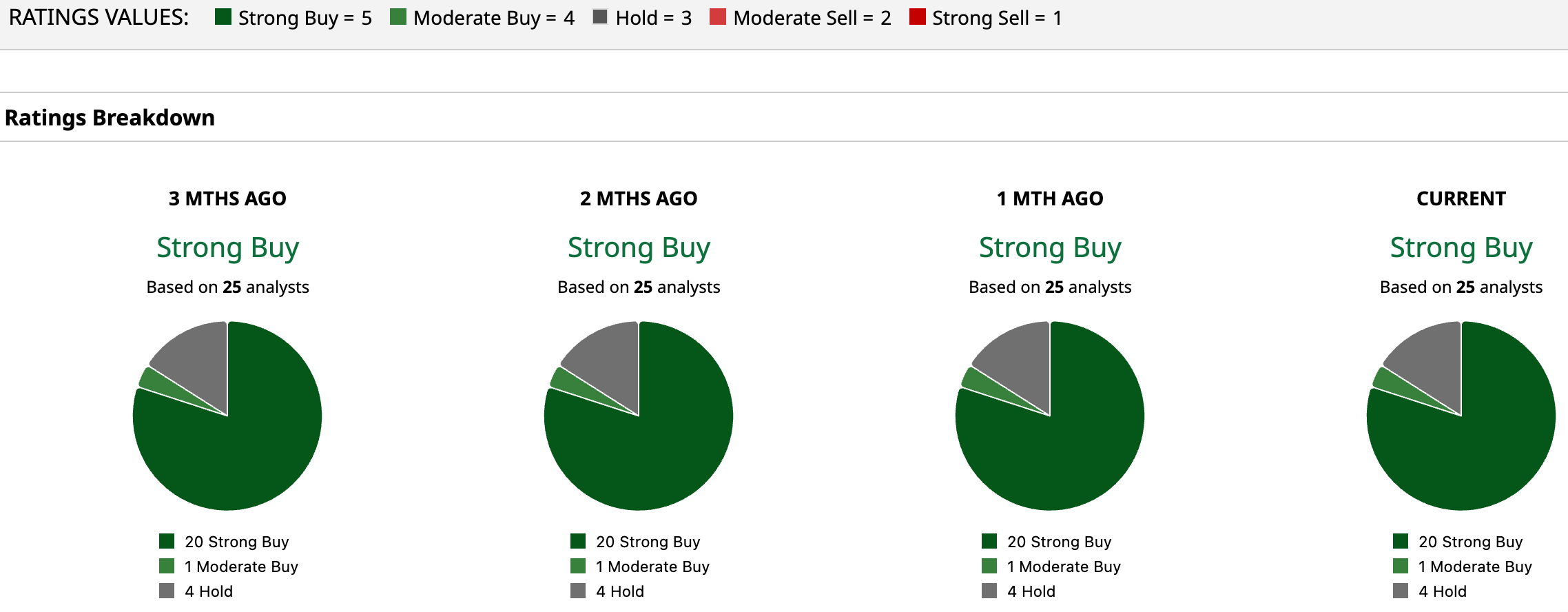

Western Digital has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 25 analysts rating the stock, a majority of 20 analysts have given it a “Strong Buy” rating, one analyst rated it “Moderate Buy,” while four analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $330.22 represents a 2.27% downside from current levels. However, the Street-high price target of $440 indicates a 30.2% upside.

Bottom Line

Western Digital spun off the NAND flash memory business last year to focus on HDDs. Therefore, when DDR and NAND prices spike, hyperscalers might seek cheaper storage alternatives and push more data onto HDDs for AI data lakes, which could be a tailwind for WDC. Therefore, with memory demand rising, the stock might be a buy now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart