The U.S.-Iran war, which started on Feb. 28, hit airline stocks hard. Jet fuel costs surged 81% from the start of the conflict and were up 124% for the year by mid-March, putting real pressure on airlines to raise fares, change routes, and prepare for weaker demand.

The U.S. Global Jets ETF (JETS), which tracks the sector, fell from about $31.33 to a low of $23.81 during that stretch. With oil climbing toward $100 a barrel, investors pulled back fast, and Deutsche Bank warned that without quick relief, airlines around the world might have to ground thousands of planes.

That changed on Apr. 8. President Trump announced a two-week ceasefire with Iran, tied to the reopening of the Strait of Hormuz, a key route for global oil supply. WTI crude oil fell more than 17% on the news, and airline stocks bounced hard. Airline shares were among the biggest winners: Alaska Air Group (ALK) jumped more than 16%, United Airlines (UAL) and Southwest (LUV) both rose more than 13%, and Delta Air Lines (DAL) gained more than 11%.

Delta came into that rally with one advantage many rivals do not have. Its Trainer Refinery, a 185,000-barrel-per-day plant in Pennsylvania, covers about 75% of its fuel needs, which gives it more protection than most major U.S. airlines when oil prices spike.

Even so, the stock is still well below its 52-week high, and an 11% jump on a ceasefire that only lasts two weeks raises a fair question: is this the start of a real recovery, or just a short-term bounce?

Delta’s Financial Strength

Delta is more than just a passenger airline. It also makes money from cargo and maintenance, which gives the business a bit more support when the travel market gets rough.

The stock has had a strong run, rising nearly 53.2% over the past 52 weeks, but it is still down 2.26% so far this year.

On valuation, Delta looks fairly cheap, trading at a forward P/E of 10.75 times versus 19.90 times for the sector. However, that also shows the market is still being careful about its near-term profit outlook.

Delta is paying shareholders, but not stretching to do it. The stock currently offers a dividend yield of about 0.71%, with a forward payout ratio of 11.59% and two straight years of dividend increases, so management has room to keep rewarding investors if earnings grow.

In the March 2026 quarter, Delta posted GAAP revenue of $15.9 billion, operating income of $501 million, and a pre-tax loss of $214 million, with an operating margin of 3.2%. Adjusted results looked better, with $14.2 billion in revenue, $652 million in operating income, and earnings per share of $0.64. The company also brought in $2.4 billion in operating cash flow, which is important because costs are still moving higher. Non-fuel CASM rose 6%, while fuel expense increased 8%. Even with that pressure, Delta still generated $63.4 billion in annual sales and $5 billion in net income, while paying a dividend yield of 0.71%.

What Still Works in Delta’s Favor

Delta recently chose GE Aerospace’s GEnx engines for 30 new Boeing 787-10s, with options for 30 more. And, the deal includes spare engines and long-term service support. That matters because these engines already have more than 70 million flight hours since 2011, so Delta is betting on equipment that is already widely used and trusted. It also gives the airline a better shot at keeping future long-haul flying efficient and reliable.

Further, Delta is trying to improve the cargo side of the business. Its partnership with Trackonomy is meant to help manage cargo and equipment better across global operations. Trackonomy says its system is on track to cover about 12% of all air containers and pallets worldwide and is already helping handle around 15 million shipments a day. For Delta, that means access to a system that is already working at scale.

The same push is showing up in Pulse, the platform Delta Cargo launched with Trackonomy. It gives customers real-time shipment tracking from airport to airport and helps Delta spot problems before they slow things down. By pulling in Cargo IQ data, live flight information, FlightAware inputs, and sensor data from airport equipment, the system is built to make cargo operations more visible, more reliable, and easier to manage.

Wall Street’s View

Wall Street is expecting a softer near-term earnings picture from Delta. For the current quarter, analysts are looking for earnings of $1.34 per share, down from $2.10 a year ago. The estimate for the Sept. quarter is $1.42, also below last year’s $1.71. For full-year 2026, the average estimate is $5.34, which is 8.25% lower than 2025’s $5.82.

That helps explain why Citigroup lowered its Delta price target from $87 to $77 in late March, but kept a “Buy” rating, saying the cut was mainly tied to higher fuel costs, not a broken long-term story. UBS analyst Thomas Wadewitz also kept a "Buy" rating and set a $75 target when the stock closed at $59.57, showing a similar view that short-term pressure does not change the bigger picture.

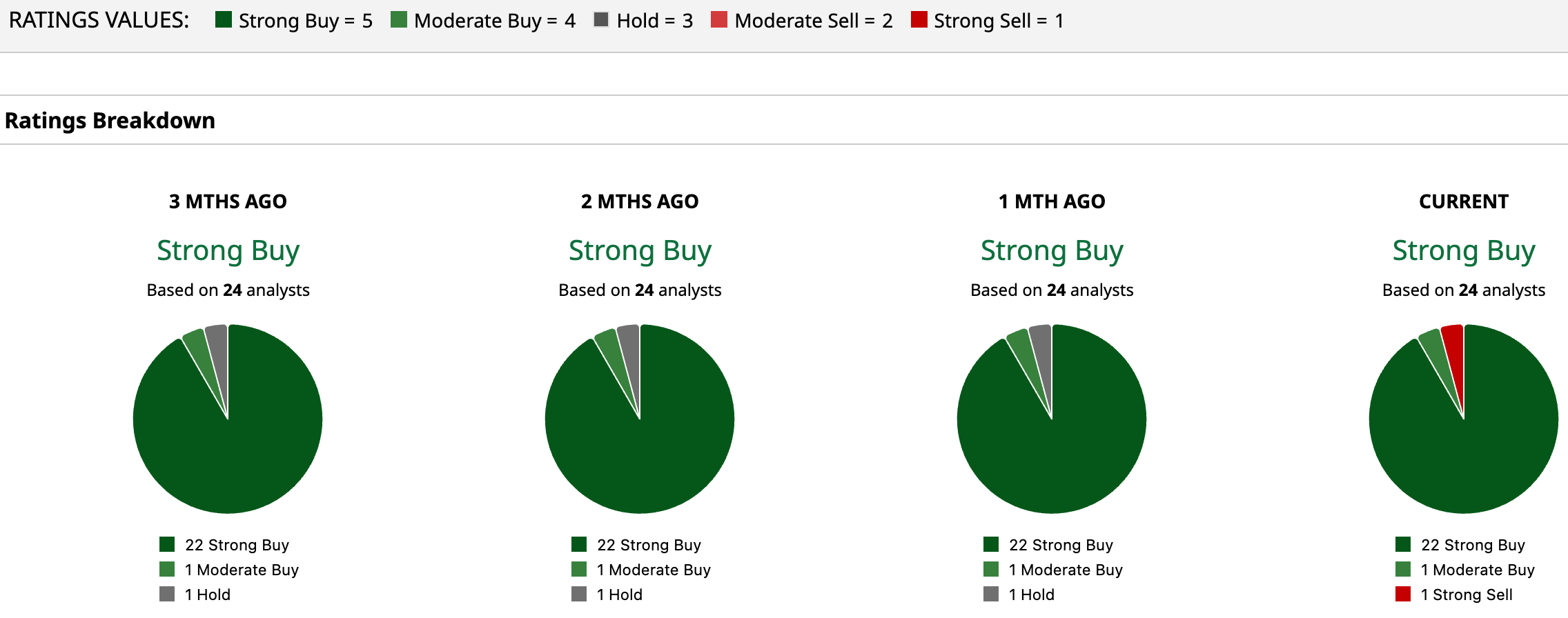

More broadly, 22 of the 24 analysts surveyed rate the stock a “Strong Buy,” and the average price target of $80.44 suggests about 18.6% upside from current levels.

Conclusion

At this point, Delta’s rally looks less like a random pop and more like investors re-pricing its earning power, even if it’s built on a fragile ceasefire. With a solid balance sheet, the Trainer refinery helping on fuel, ongoing fleet upgrades, and a full slate of “Strong Buy” ratings, any pullbacks from here look more like chances to add than signs the story is broken. If the truce holds and oil doesn’t spike again, Delta’s stock is more likely to work its way up toward the $80 area over the next year or so than give back the whole move, but it probably won’t be a smooth ride.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart