The U.S.-Iran war has tightened its grip on the aluminum market, and prices have moved decisively higher, rising about 10% even as metals like copper lose ground. Momentum held firm into the week, with prices climbing another 3% on Monday, March 30. The disruption runs through the heart of global supply.

The Middle East accounts for roughly 9% of aluminum production, and the region now faces both logistical and operational setbacks. Iran’s blockade of the Strait of Hormuz has stalled key shipments, while several production facilities have been damaged or forced offline.

The situation escalated further after attacks on Emirates Global Aluminium and Aluminium Bahrain. Australian bank ANZ estimates that four to five million metric tons of exports are now at risk. Even if tensions ease, supply losses could linger, keeping prices supported for longer than the market initially anticipated.

Against this backdrop, Century Aluminum Company (CENX) has stepped into focus. As the largest aluminum smelter in the U.S., the company stands to benefit from tightening global supply and rising realized prices. Its positioning allows margins to expand as industry capacity contracts, creating a favorable setup for the company.

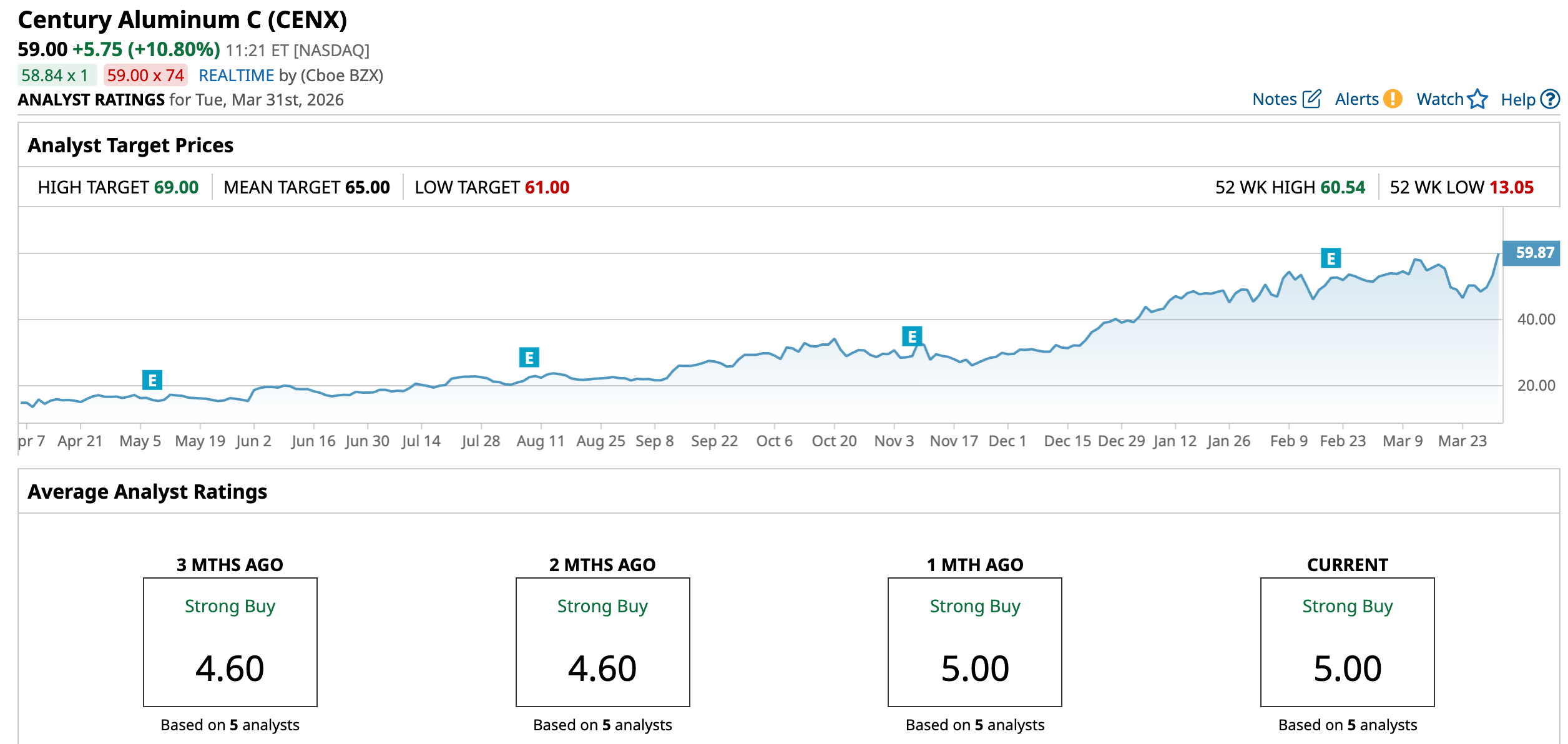

CENX stock has gained 53.14% in 2026, comfortably outpacing Alcoa Corporation (AA), which remains the industry’s most recognized name by market cap. On March 30 alone, Century Aluminum’s shares rose 7.3%, taking its past five trading days' advance to 18.12%.

The rally reflects a shift in market positioning and brings the extent of remaining upside into clearer focus.

About Century Aluminum Stock

Headquartered in Chicago, Illinois, Century Aluminum accounts for nearly 60% of domestic output. With a market cap of $5.27 billion, its footprint stretches across smelting operations in the U.S. and Iceland, alongside bauxite mining and alumina refining in Jamaica. Also, the company runs a carbon anode facility in the Netherlands, supporting a vertically integrated model that strengthens cost control and supply reliability.

Coming to price performance, the stock has rallied 219.75% over the past 52 weeks and 112% in the last six months, reflecting improving fundamentals and a favorable macro backdrop.

From a valuation perspective, CENX stock is trading at 5.47 times forward adjusted earnings, placing it at a noticeable discount to the industry average and its own five-year average multiple. This could suggest a wise entry point in the stock for those willing to stay the course.

Century Aluminum Misses Q4 Earnings

On Feb. 19, Century Aluminum reported its Q4 fiscal 2025 results, wherein revenue marginally rose year-over-year (YOY) to $633.7 million but fell short of the $658 million analyst estimate. On a sequential basis, revenue inched up by $2 million, as stronger realized London Metal Exchange prices and Midwest premiums provided support, while softer shipment volumes capped the upside.

Gross profit climbed 35.7% YOY to $90 million, reflecting improving pricing dynamics. However, net income slipped 95.9% to $1.8 million, and EPS plunged 95.5% from the prior year’s quarter to $0.02, missing the Street’s expectation of $1.32.

Liquidity remained a strong pillar. As of Dec. 31, 2025, Century Aluminum held $134.2 million in cash and cash equivalents, alongside $283.8 million in available borrowing capacity, bringing total liquidity to $418.0 million. The company also reduced net debt by $54 million during the quarter.

Looking ahead, management expects Q1 fiscal 2026 adjusted EBITDA in the range of $215 million to $235 million, supported by firmer metal prices and regional premiums. However, higher U.S. energy costs tied to Winter Storm Fern might weigh on near-term margins.

For fiscal 2026, management expects to ship approximately 630,000 tons of primary aluminum, keeping volumes steady as pricing dynamics take center stage. The company plans to allocate between $115 million and $125 million in total CapEx, balancing sustaining needs with targeted investments to support long-term efficiency.

And analysts see a sharp uprise ahead. They expect Q1 fiscal 2026 EPS to rise significantly YOY. The Street projects full-year 2026 bottom line to surge 1,500% from the prior year to $6.72, followed by a further 4.2% increase to $7 in fiscal year 2027.

What Do Analysts Expect for Century Aluminum Stock?

Wall Street has aligned firmly behind Century Aluminum, and the tone has grown more favorable in recent weeks. B. Riley Securities analyst Lucas Pipes reaffirmed a “Buy” rating while lifting the price target from $64 to $68. The revision reflects rising confidence in earnings leverage as aluminum prices strengthen and supply tightens globally.

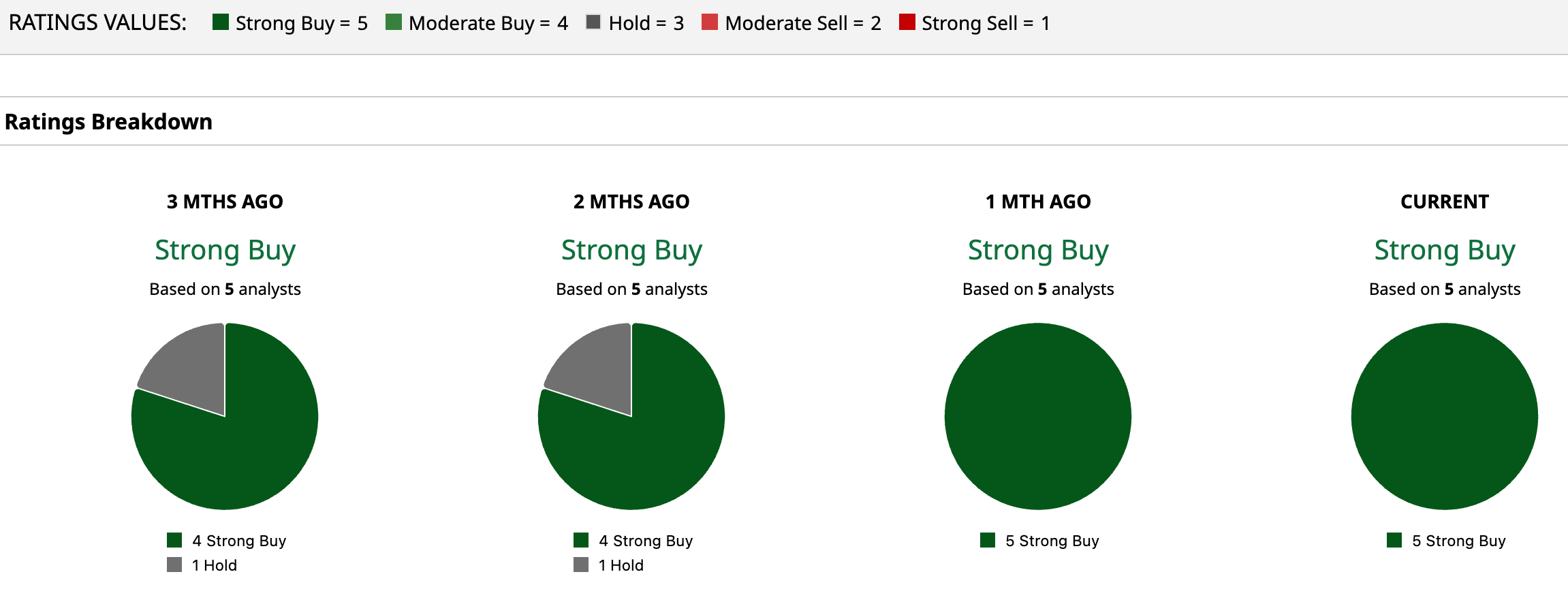

The broader analyst community reinforces the optimism. The stock holds a “Strong Buy” overall rating, with all five analysts firmly backing it with the same top-tier recommendation.

The numbers reinforce the view with an average price target of $65, implying potential upside of 10.2%. Meanwhile, the Street-high target of $69 by Timna Tanners of Wells Fargo points to a possible gain of 17% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Ignore the Panic and Buy the Dip in Micron Stock, Says Bank of America

- Ignore the TurboQuant Panic and Keep Buying Seagate Technology Stock, Says JPMorgan

- Constellation Energy Just Broke Below Its 50-Day Moving Average. Should You Buy the CEG Stock Dip as Company Misses Guidance?

- Energy Prices Could Soon ‘Skyrocket.’ Why Cheniere Is One of the Top-Rated Stocks to Buy Now.