As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the regional banks industry, including Eastern Bank (NASDAQ: EBC) and its peers.

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

The 91 regional banks stocks we track reported a slower Q1. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 7.7% on average since the latest earnings results.

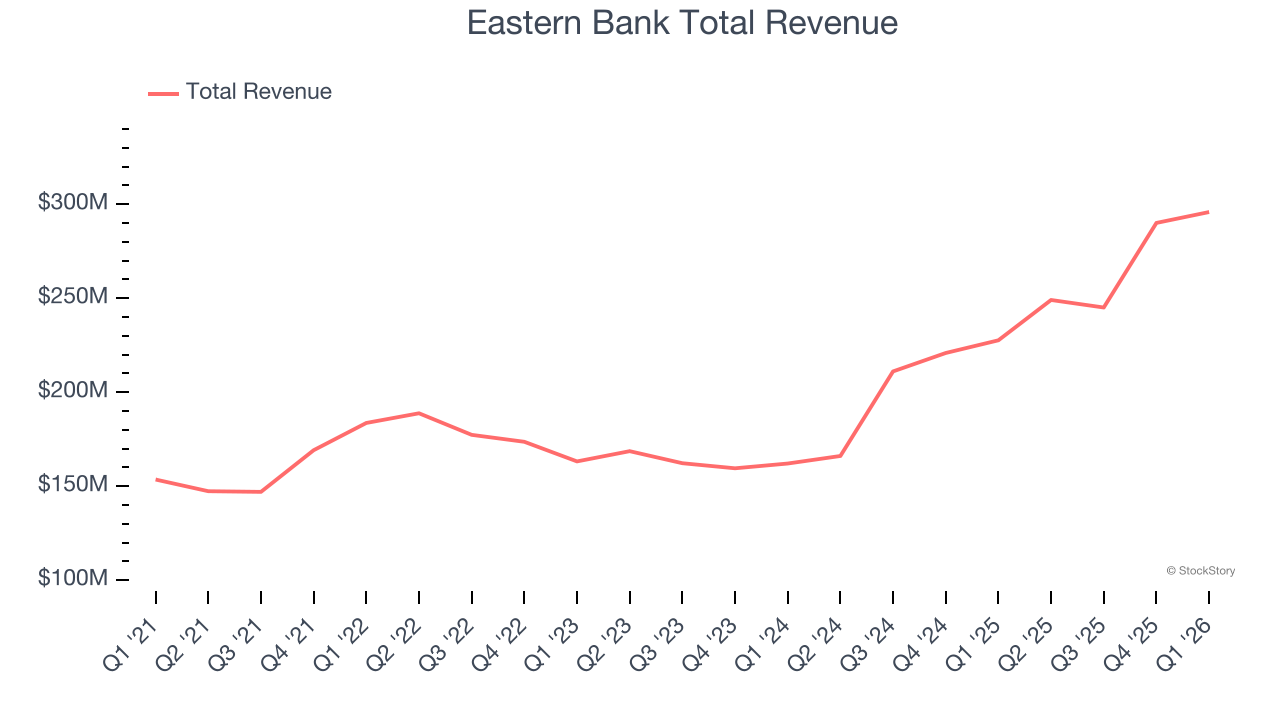

Eastern Bank (NASDAQ: EBC)

Founded in 1818 as one of America's oldest mutual banks before converting to a public company in 2020, Eastern Bankshares (NASDAQ: EBC) operates as a bank holding company providing commercial and retail banking services primarily in Massachusetts, New Hampshire, and Rhode Island.

Eastern Bank reported revenues of $295.9 million, up 30% year on year. This print fell short of analysts’ expectations by 2%. Overall, it was a softer quarter for the company with a significant miss of analysts’ net interest income and EPS estimates.

Interestingly, the stock is up 9.8% since reporting and currently trades at $22.53.

Read our full report on Eastern Bank here, it’s free.

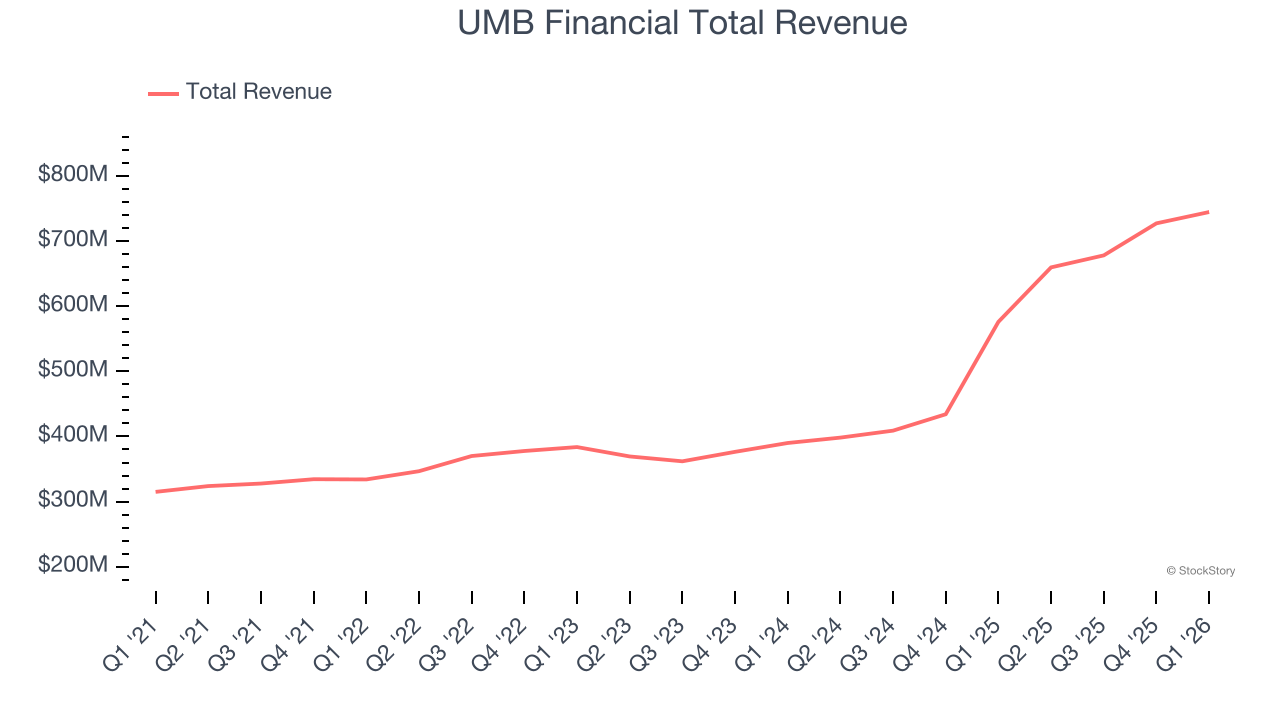

Best Q1: UMB Financial (NASDAQ: UMBF)

With roots dating back to 1913 and a name derived from "United Missouri Bank," UMB Financial (NASDAQ: UMBF) is a financial holding company that provides banking, asset management, and fund services to commercial, institutional, and individual customers.

UMB Financial reported revenues of $744.8 million, up 29.3% year on year, outperforming analysts’ expectations by 5.4%. The business had an exceptional quarter with a beat of analysts’ EPS and net interest income estimates.

UMB Financial scored the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 16.5% since reporting. It currently trades at $146.03.

Is now the time to buy UMB Financial? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: BankUnited (NYSE: BKU)

Born from the ashes of a failed Florida thrift during the 2009 financial crisis, BankUnited (NYSE: BKU) is a regional bank that provides commercial lending, deposit services, and treasury solutions to businesses and consumers primarily in Florida and the New York metropolitan area.

BankUnited reported revenues of $273.8 million, up 6.1% year on year, falling short of analysts’ expectations by 5.1%. It was a disappointing quarter as it posted a significant miss of analysts’ net interest income and EPS estimates.

Interestingly, the stock is up 4.4% since the results and currently trades at $48.81.

Read our full analysis of BankUnited’s results here.

City Holding (NASDAQ: CHCO)

With roots dating back to 1957 and a strategic presence along the I-64 and I-81 corridors, City Holding (NASDAQGS:CHCO) operates as a financial holding company providing banking, trust, and investment services through its subsidiary City National Bank across West Virginia, Kentucky, Virginia, and Ohio.

City Holding reported revenues of $79.49 million, up 6.4% year on year. This number met analysts’ expectations. However, it was a slower quarter as it recorded a slight miss of analysts’ net interest income estimates and a slight miss of analysts’ tangible book value per share estimates.

The stock is up 6.8% since reporting and currently trades at $132.78.

Read our full, actionable report on City Holding here, it’s free.

First Busey (NASDAQ: BUSE)

Tracing its roots back to 1868 during America's post-Civil War reconstruction era, First Busey (NASDAQ: BUSE) is a bank holding company that provides commercial and retail banking, wealth management, and payment technology solutions across Illinois, Missouri, Florida, and Indiana.

First Busey reported revenues of $197.2 million, up 40.1% year on year. This print was in line with analysts’ expectations. Overall, it was a strong quarter as it also produced an impressive beat of analysts’ tangible book value per share and EPS estimates.

The stock is up 10.1% since reporting and currently trades at $29.22.

Read our full, actionable report on First Busey here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.