Over the past six months, Atmus Filtration Technologies’s stock price fell to $50.83. Shareholders have lost 6.3% of their capital, which is disappointing considering the S&P 500 has climbed by 9%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Atmus Filtration Technologies, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Atmus Filtration Technologies Not Exciting?

Even though the stock has become cheaper, we’re swiping left on Atmus Filtration Technologies for now. Here are three reasons why there are better opportunities than ATMU, plus one stock we’d rather own.

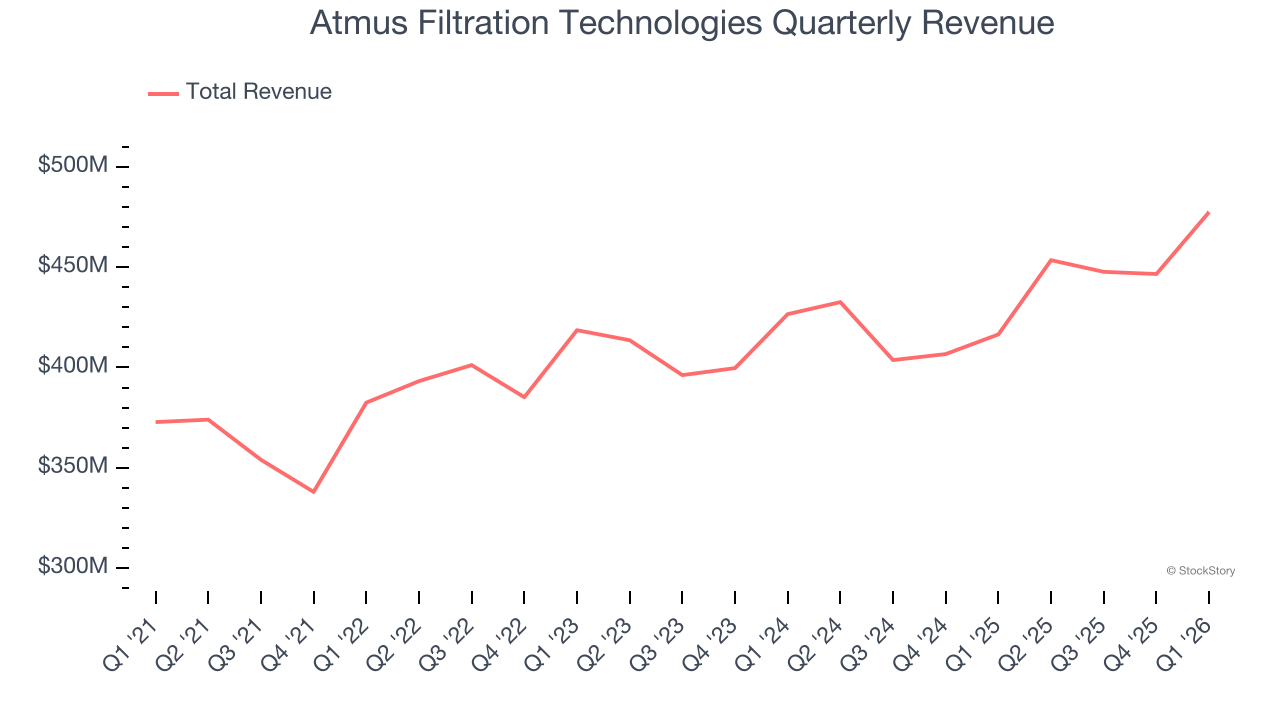

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last four years, Atmus Filtration Technologies grew its sales at a tepid 6% compounded annual growth rate. This was below our standard for the industrials sector.

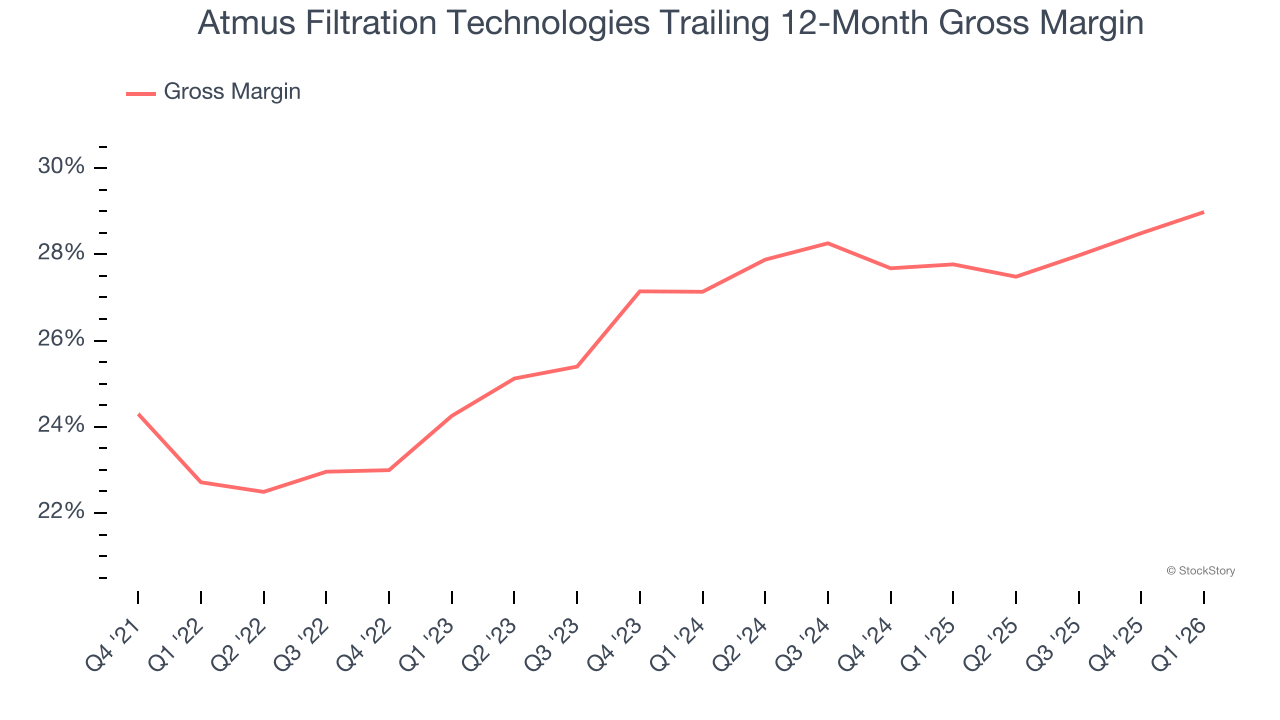

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Atmus Filtration Technologies has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 26.3% gross margin over the last five years. That means Atmus Filtration Technologies paid its suppliers a lot of money ($73.67 for every $100 in revenue) to run its business.

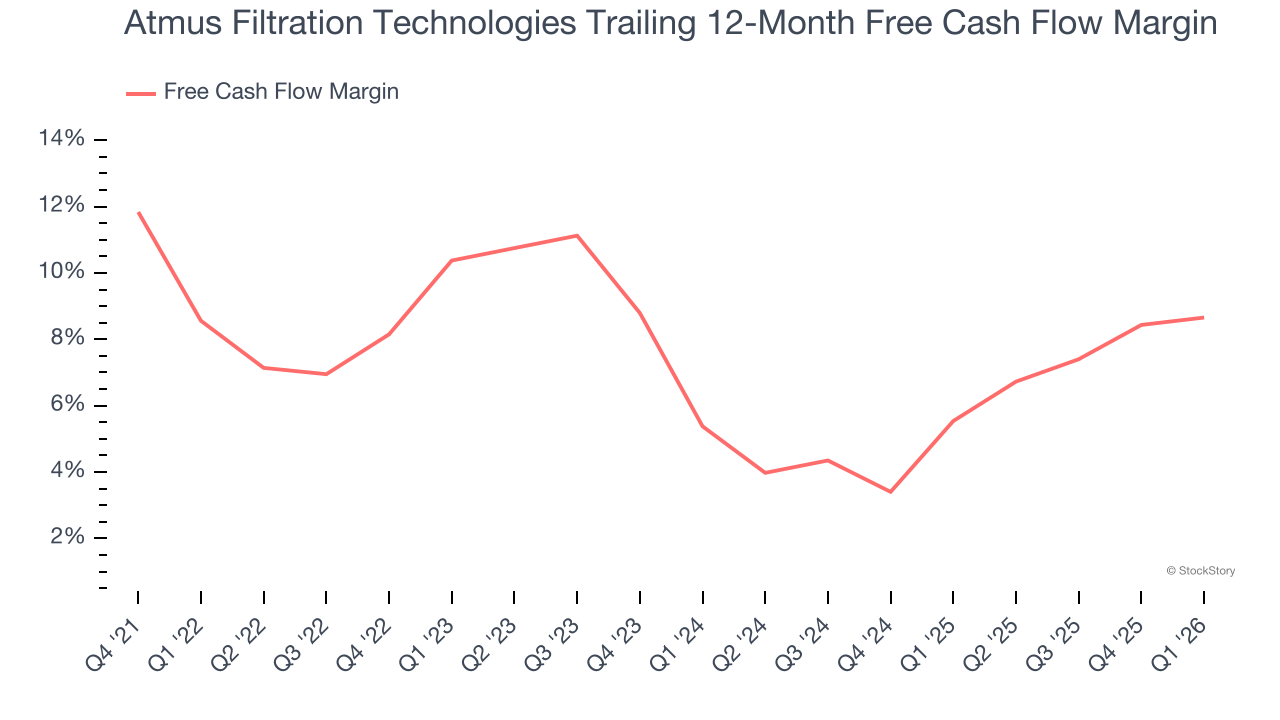

3. Free Cash Flow Margin Stuck in Neutral

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Atmus Filtration Technologies’s margin was unchanged over the last five years, showing it couldn’t improve. Its free cash flow margin for the trailing 12 months was 8.7%.

Final Judgment

Atmus Filtration Technologies’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 17.3× forward P/E (or $50.83 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at the most dominant software business in the world.

Stocks We Like More Than Atmus Filtration Technologies

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.