Over the past six months, Piper Sandler’s shares (currently trading at $75.11) have posted a disappointing 18.3% loss, well below the S&P 500’s 9% gain. This may have investors wondering how to approach the situation.

Following the drawdown, is now an opportune time to buy PIPR? Find out in our full research report, it’s free.

Why Do Investors Watch Piper Sandler?

Tracing its roots back to 1895 and rebranded from Piper Jaffray in 2020, Piper Sandler (NYSE: PIPR) is an investment bank that provides advisory services, capital raising, institutional brokerage, and research for corporations, governments, and institutional investors.

Three Things to Like:

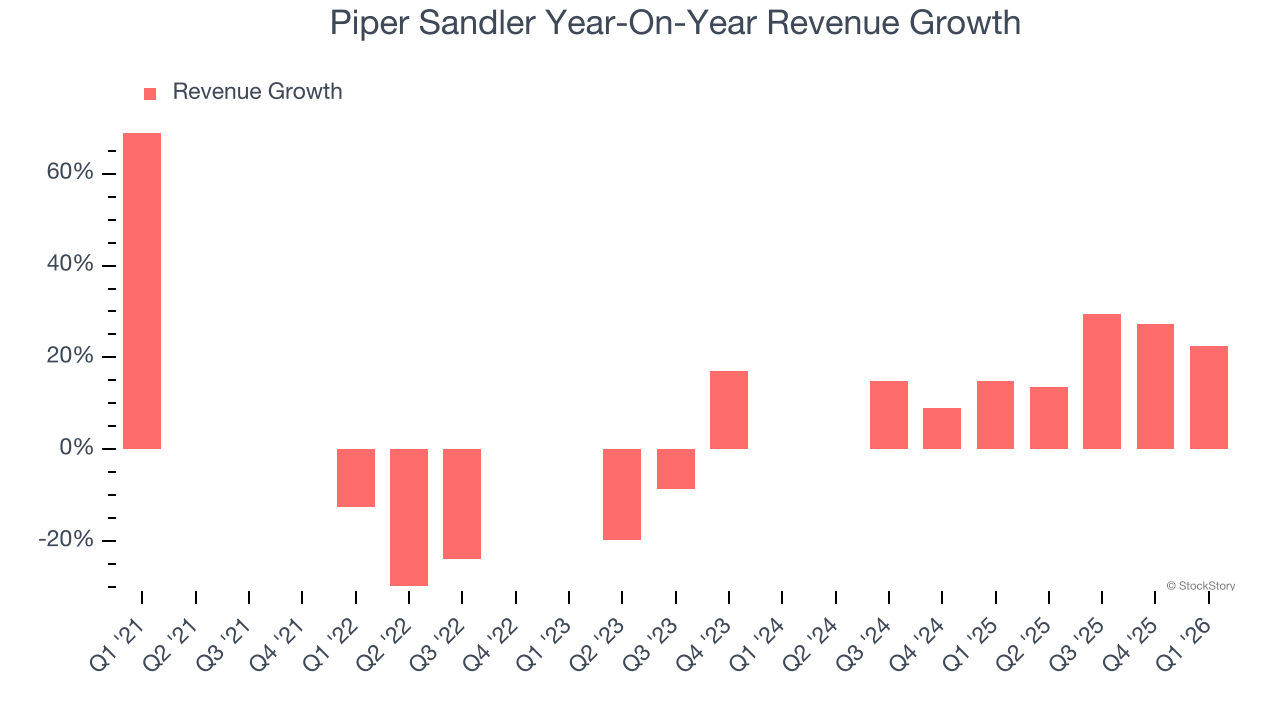

1. Skyrocketing Revenue Shows Strong Momentum

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. Piper Sandler’s annualized revenue growth of 19.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

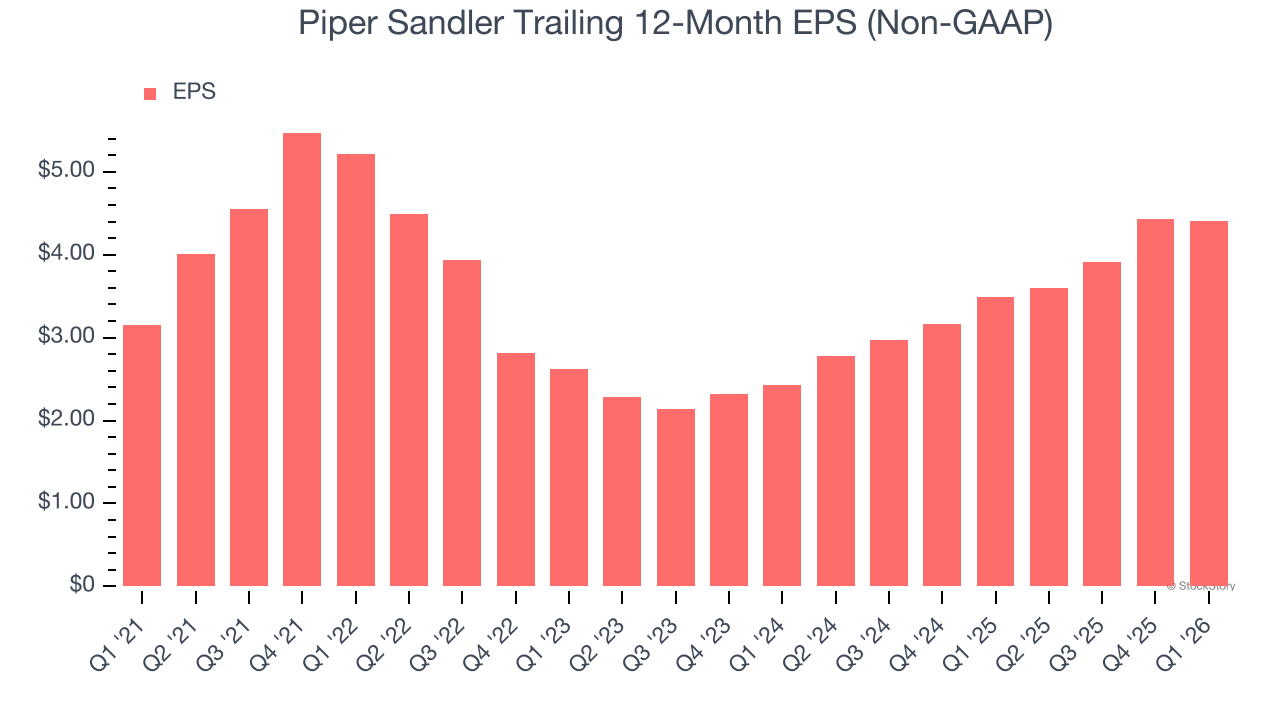

2. EPS Surges Higher Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Piper Sandler’s EPS grew at an astounding 34.8% compounded annual growth rate over the last two years, higher than its 19.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

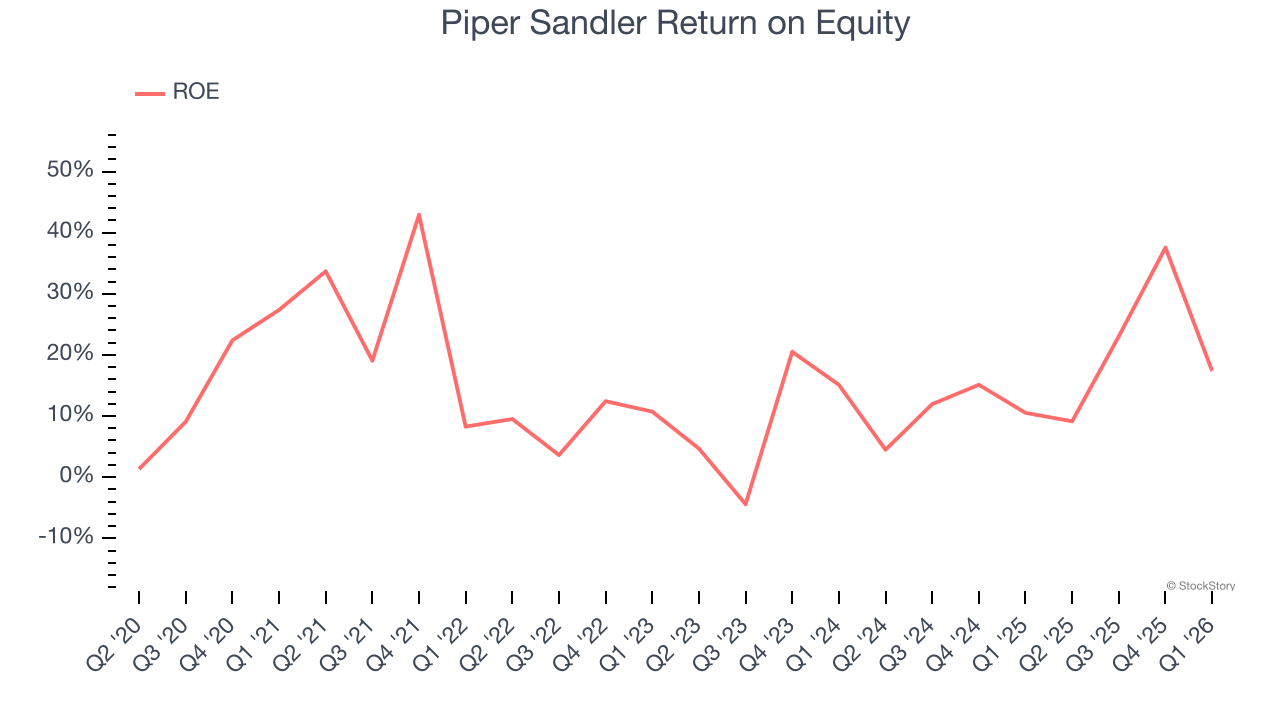

3. Market-Beating ROE Showcases Attractive Growth Opportunities

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for financial firms. Over a long period, financial firms with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, Piper Sandler has averaged an ROE of 15.3%, healthy for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Piper Sandler has a decent competitive moat.

Final Judgment

Piper Sandler is an interesting business with potential. After the recent drawdown, the stock trades at 15× forward P/E (or $75.11 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Piper Sandler

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.