Over the past six months, ServisFirst Bancshares has been a great trade, beating the S&P 500 by 11.1%. Its stock price has climbed to $87.80, representing a healthy 19.1% increase. This performance may have investors wondering how to approach the situation.

Is now still a good time to buy SFBS? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Is SFBS a Good Business?

Founded in 2005 with a focus on serving underserved mid-sized businesses, ServisFirst Bancshares (NYSE: SFBS) is a bank holding company that provides commercial banking services to businesses and professionals through its subsidiary ServisFirst Bank.

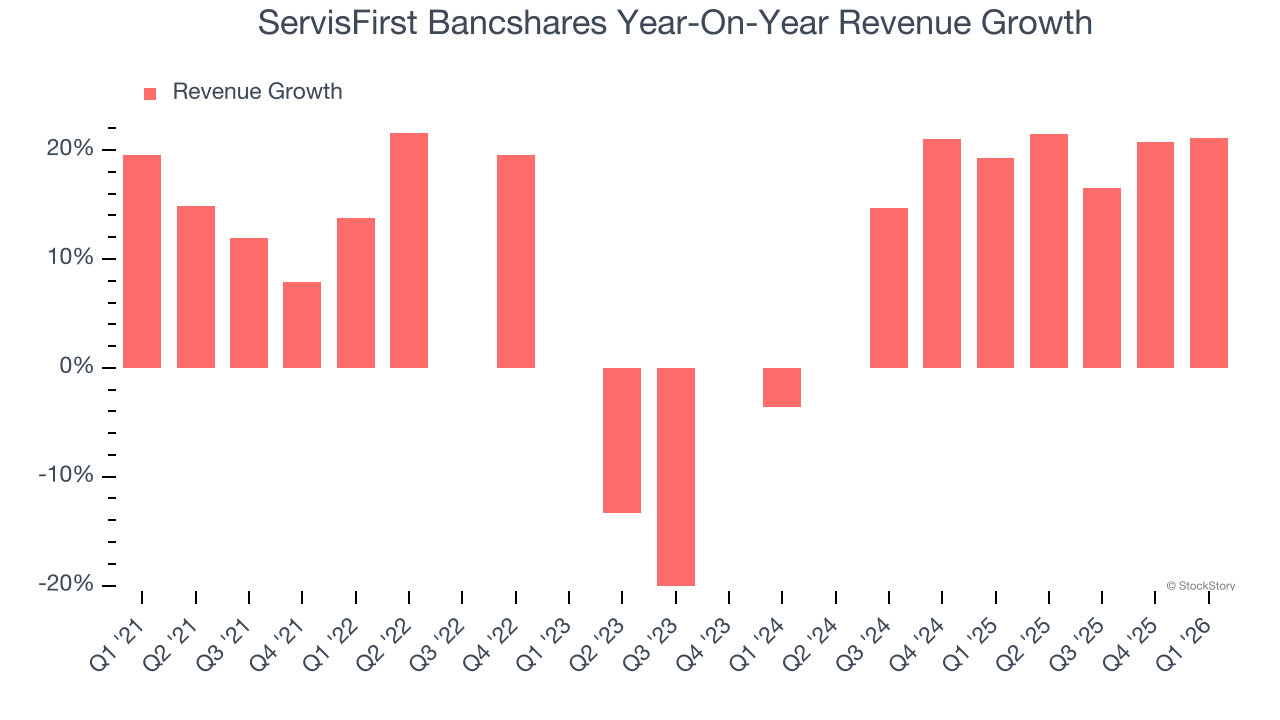

1. Skyrocketing Revenue Shows Strong Momentum

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. ServisFirst Bancshares’s annualized revenue growth of 17.5% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

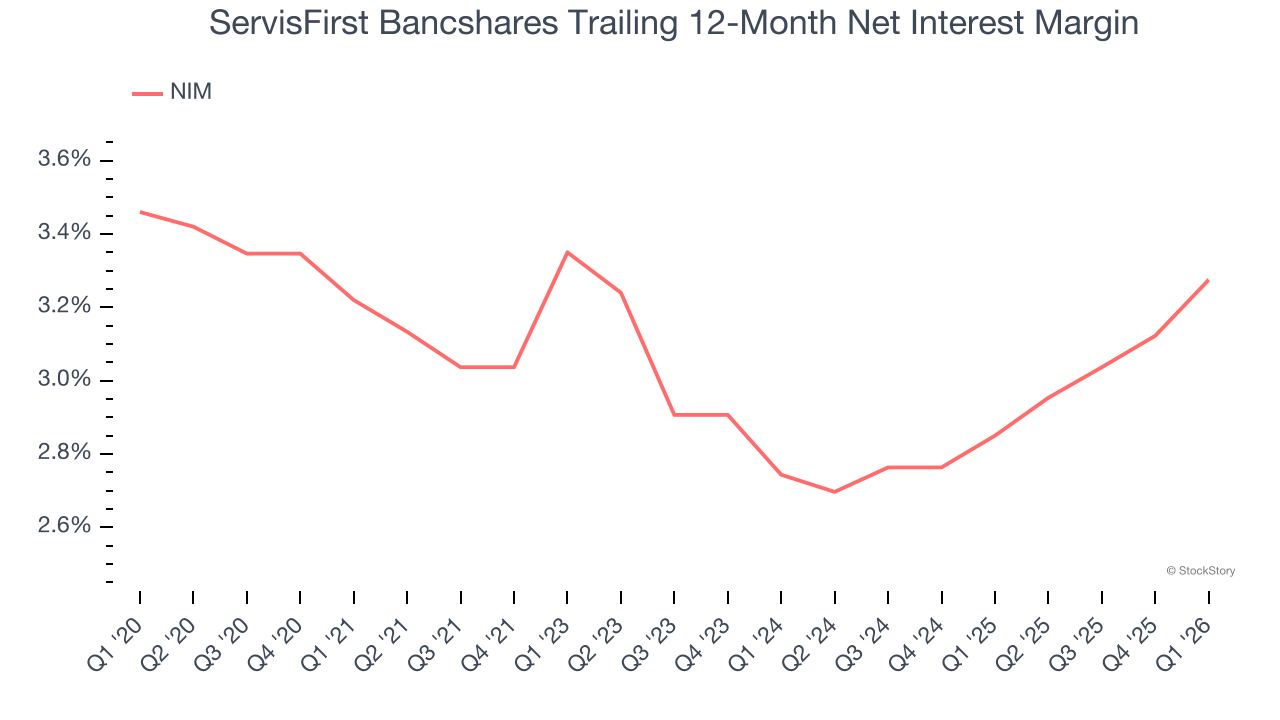

2. Increasing Net Interest Margin Juices Financials

Net interest margin (NIM) serves as a critical gauge of a bank’s fundamental profitability by showing the spread between interest income and interest expenses. It’s essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, ServisFirst Bancshares’s net interest margin averaged 3.1%. On the bright side, it climbed by 53.2 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

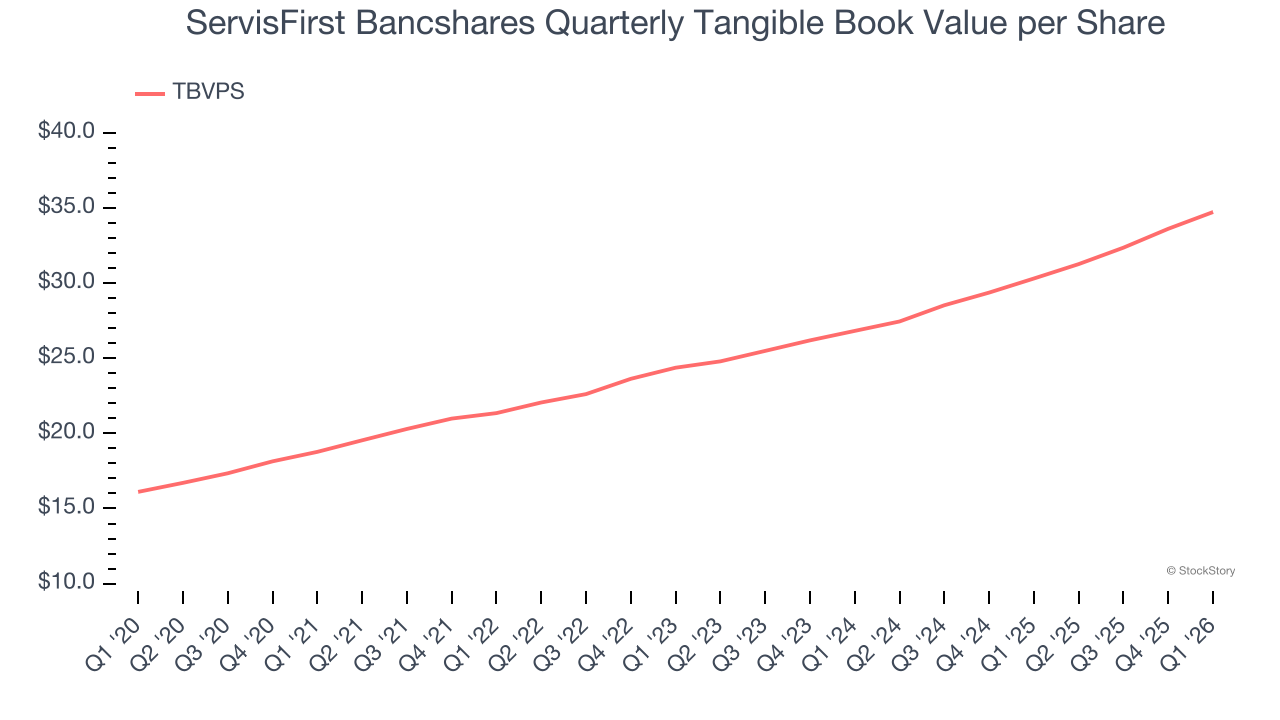

3. Steady Increase in TBVPS Highlights Solid Asset Growth

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

ServisFirst Bancshares’s TBVPS increased by 13.1% annually over the last five years, and the past two years show a similar trajectory as TBVPS grew at a solid 13.8% annual clip (from $26.82 to $34.73 per share).

Final Judgment

These are just a few reasons why we think ServisFirst Bancshares is a high-quality business, and with its shares topping the market in recent months, the stock trades at 2.2× forward P/B (or $87.80 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than ServisFirst Bancshares

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.