Janus’s stock price has taken a beating over the past six months, shedding 22.2% of its value and falling to $5.29 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Janus, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Janus Not Exciting?

Even with the cheaper entry price, we don’t have much confidence in Janus. Here are three reasons why JBI doesn’t excite us, plus one stock we’d rather own.

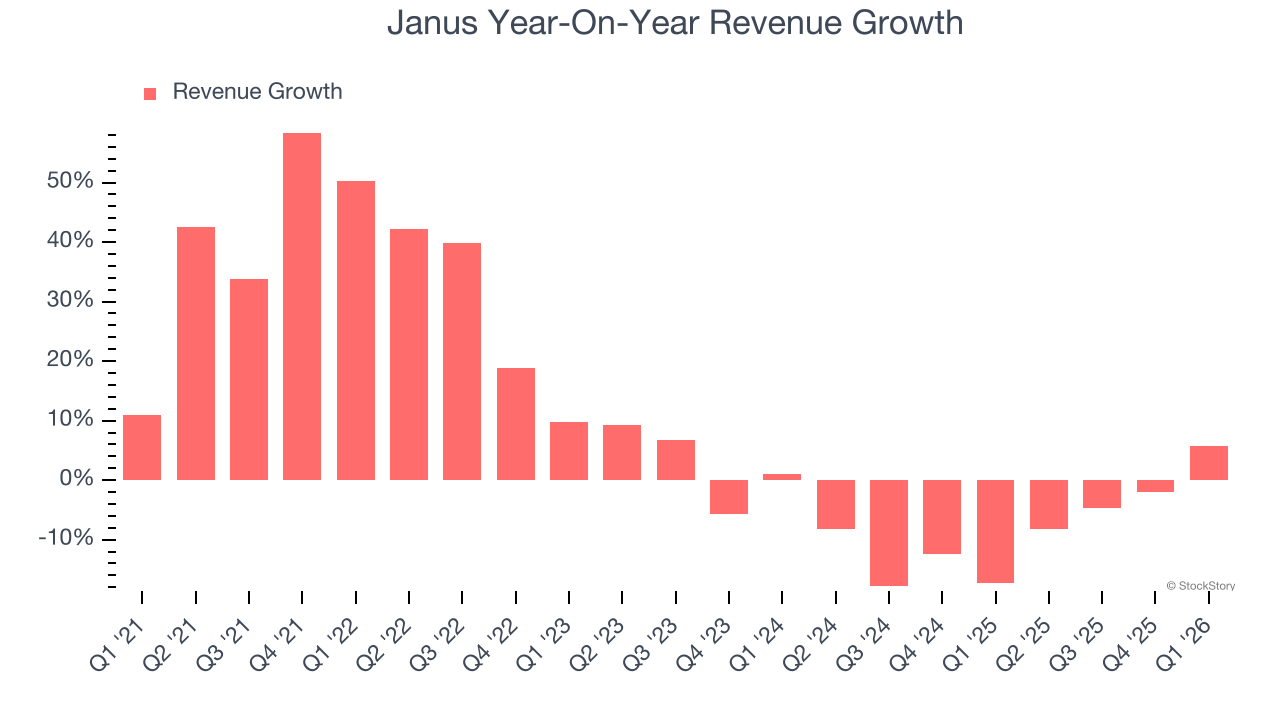

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Janus’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 8.4% over the last two years.

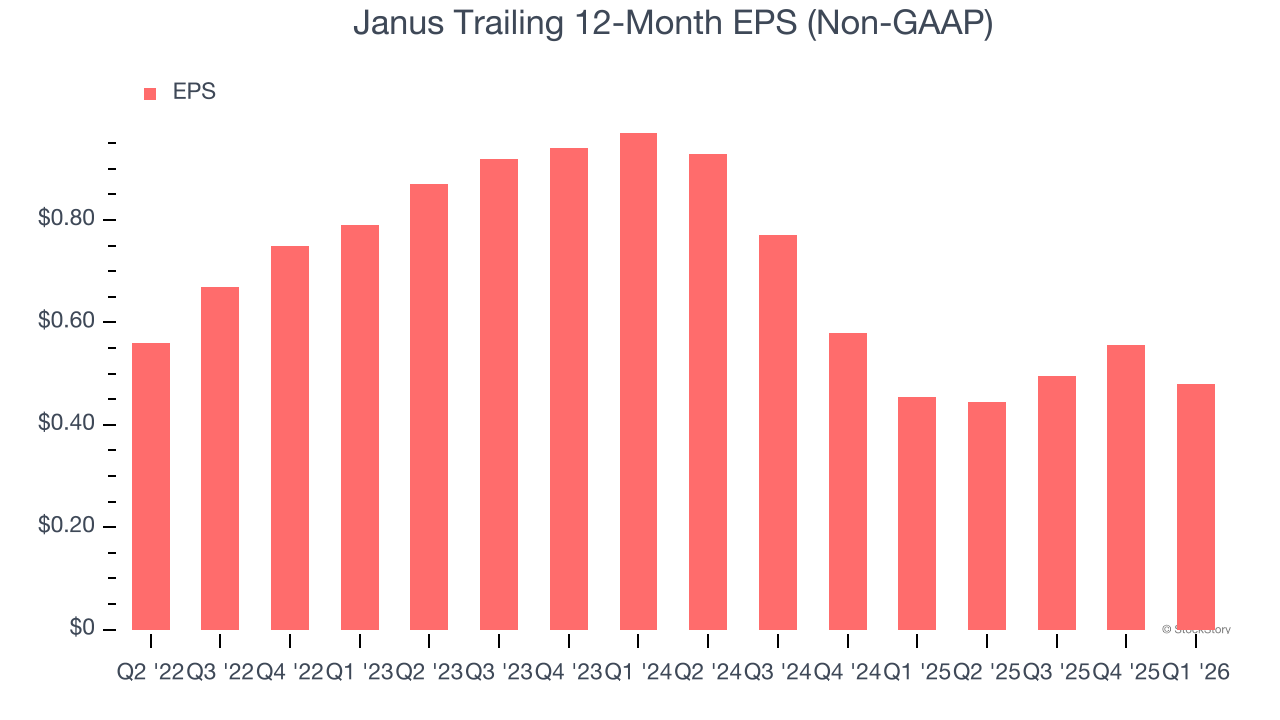

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Janus’s full-year EPS dropped 35.8%, or 8% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Janus’s low margin of safety could leave its stock price susceptible to large downswings.

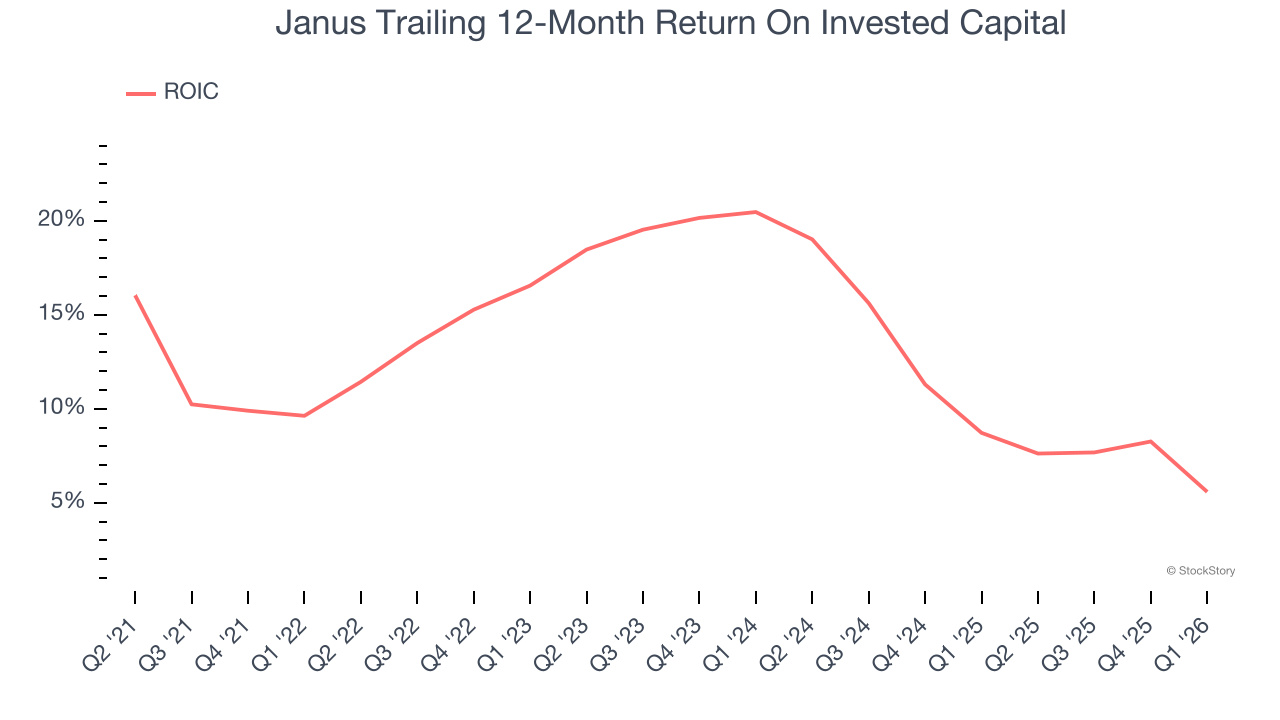

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Unfortunately, Janus’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Janus isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 6.7× forward EV-to-EBITDA (or $5.29 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re fairly confident there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.