What a time it’s been for Smith & Wesson. In the past six months alone, the company’s stock price has increased by a massive 49.2%, reaching $15.36 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Smith & Wesson, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Smith & Wesson Will Underperform?

We’re glad investors have benefited from the price increase, but we’re swiping left on Smith & Wesson for now. Here are three reasons why there are better opportunities than SWBI, plus one stock we’d rather own.

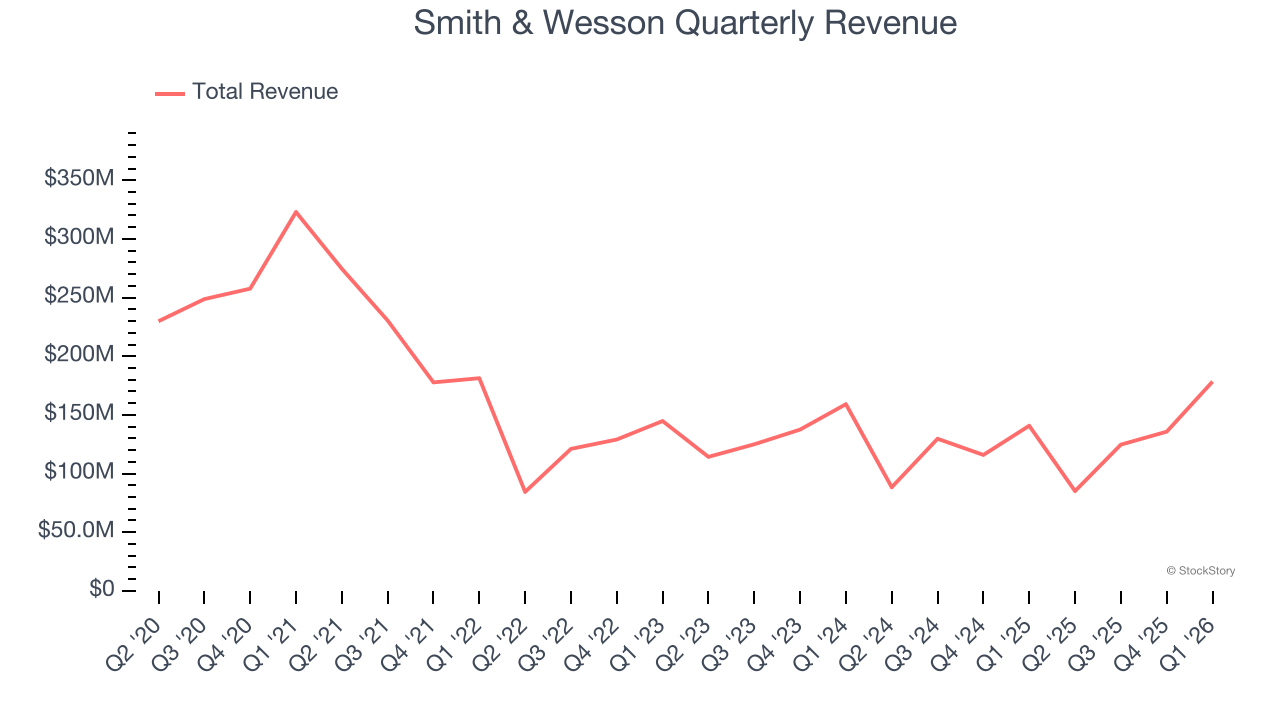

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Smith & Wesson’s demand was weak over the last five years as its sales fell at a 13.1% annual rate. This wasn’t a great result and is a sign of poor business quality.

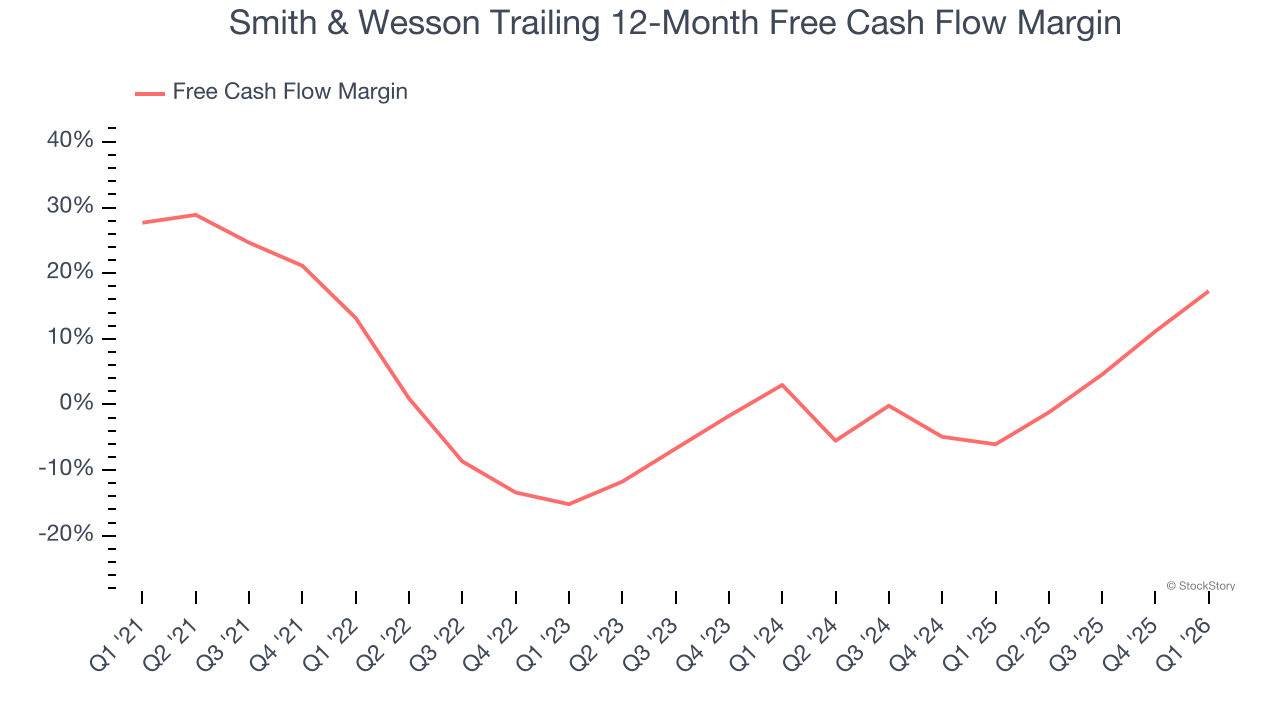

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Smith & Wesson has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.2%, below what we’d expect for a consumer discretionary business.

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Unfortunately, Smith & Wesson’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Smith & Wesson falls short of our quality standards. After the recent rally, the stock trades at 45.3× forward P/E (or $15.36 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. Let us point you toward a dominant aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Smith & Wesson

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.