Fifth Third Bancorp’s 17.9% return over the past six months has outpaced the S&P 500 by 9.9%, and its stock price has climbed to $57.97 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Fifth Third Bancorp, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Fifth Third Bancorp Not Exciting?

We’re glad investors have benefited from the price increase, but we’re swiping left on Fifth Third Bancorp for now. Here are three reasons you should be careful with FITB, plus one stock we’d rather own.

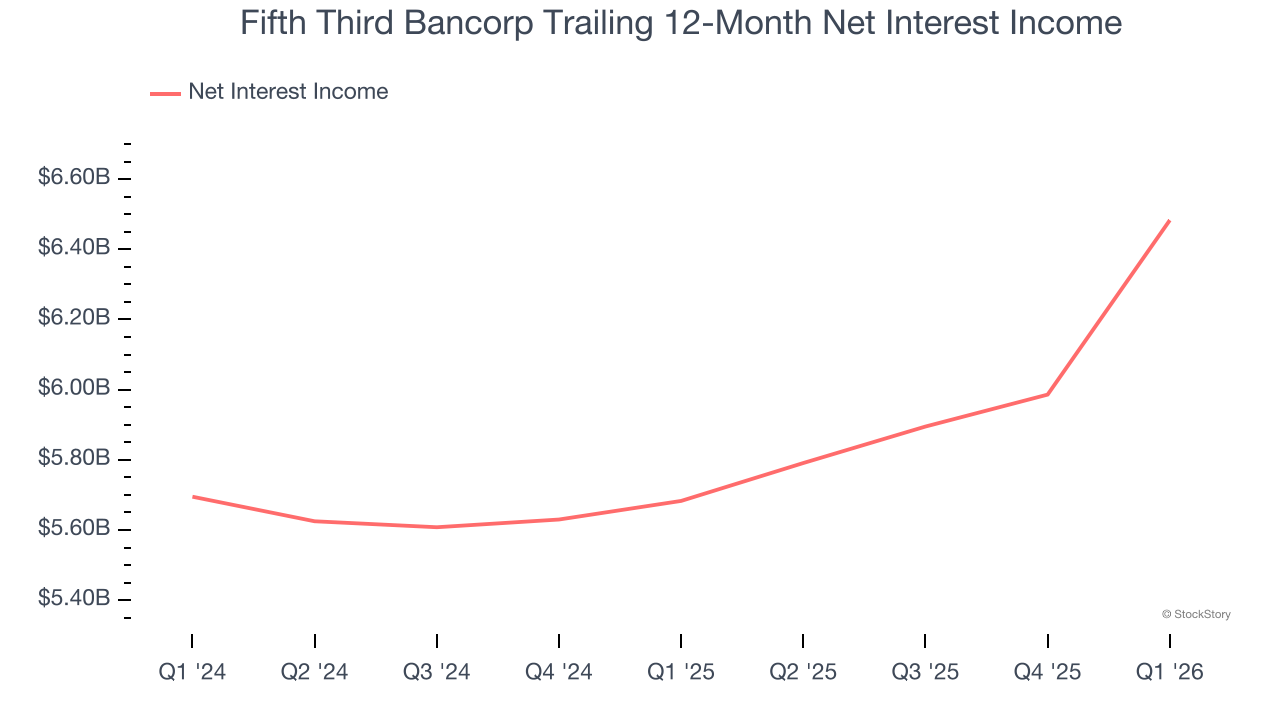

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Fifth Third Bancorp’s net interest income has grown at a 6.5% annualized rate over the last five years, worse than the broader banking industry. Its growth was driven by both an increase in its outstanding loans and net interest margin, which represents how much a bank earns in relation to its outstanding loan book.

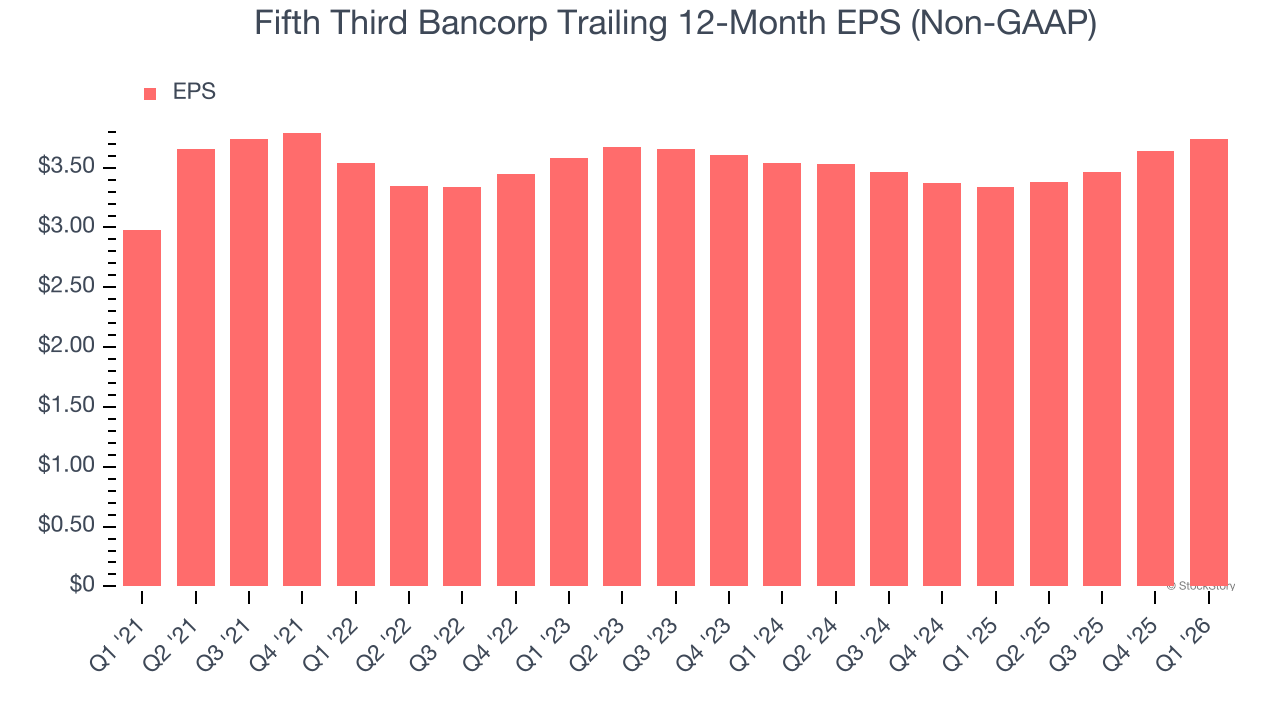

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Fifth Third Bancorp’s weak 4.7% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

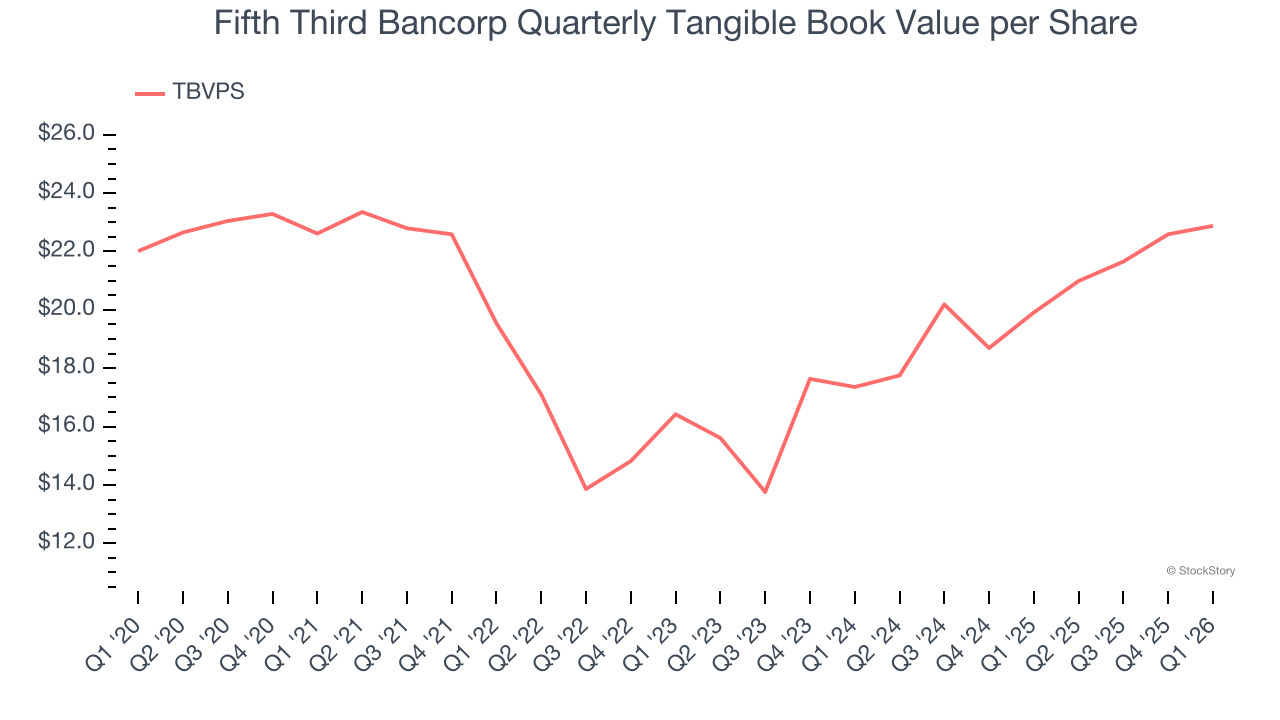

3. Growing TBVPS Reflects Strong Asset Base

We consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation.

Although Fifth Third Bancorp’s TBVPS was flat over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at an impressive 14.8% annual clip over the past two years (from $17.36 to $22.88 per share).

Final Judgment

Fifth Third Bancorp isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 1.5× forward P/B (or $57.97 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We’re pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Fifth Third Bancorp

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.