Over the past six months, Avery Dennison’s shares (currently trading at $163.83) have posted a disappointing 10.1% loss, well below the S&P 500’s 11.4% gain. This might have investors contemplating their next move.

Is now the time to buy Avery Dennison, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Avery Dennison Not Exciting?

Even though the stock has become cheaper, we’re cautious about Avery Dennison. Here are three reasons why AVY doesn’t excite us, plus one stock we’d rather own.

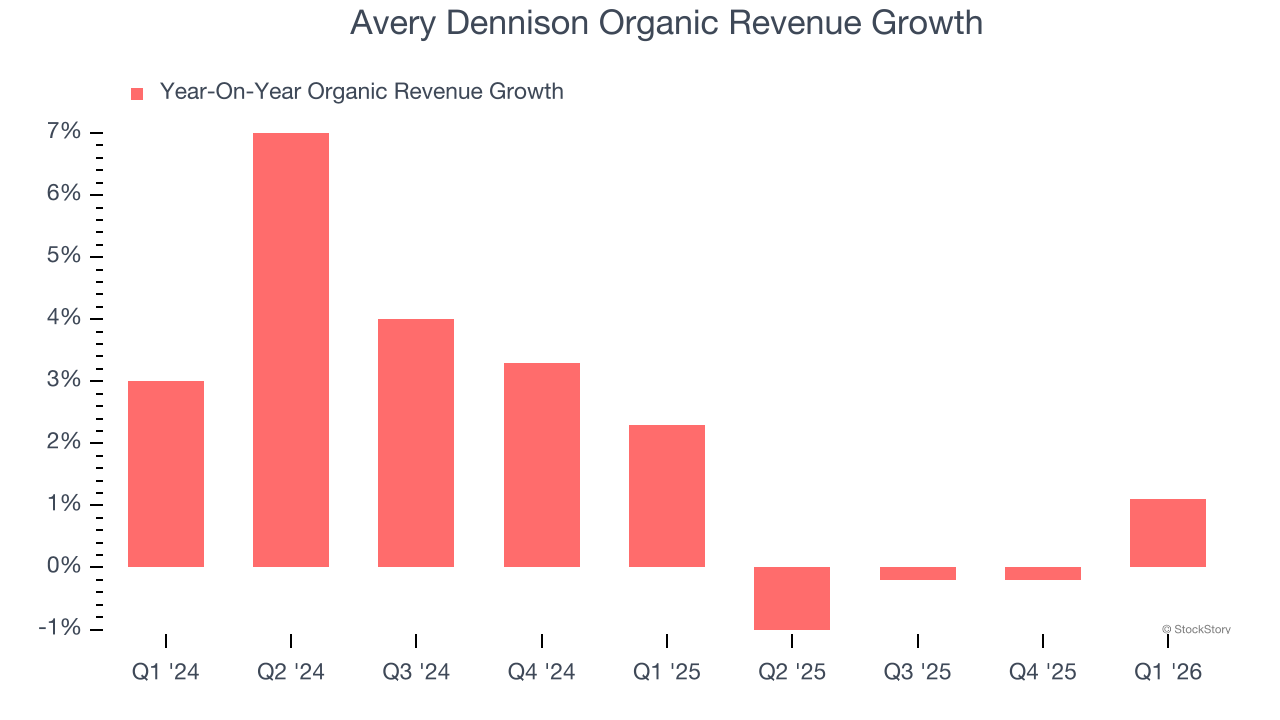

1. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand Industrial Packaging companies by analyzing their organic revenue. This metric gives visibility into Avery Dennison’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Avery Dennison’s organic revenue averaged 2% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Avery Dennison’s revenue to rise by 3.7%, close to its 4.3% annualized growth for the past five years. This projection doesn’t excite us and suggests its newer products and services will not catalyze better top-line performance yet.

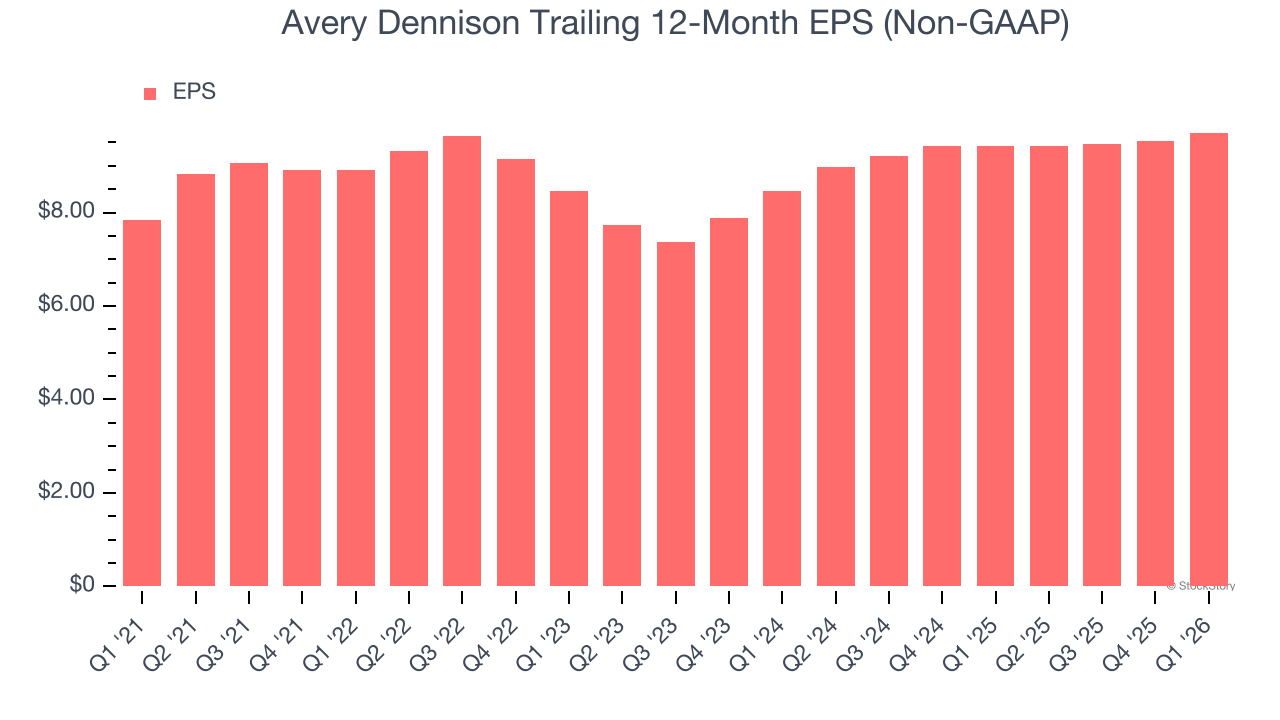

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Avery Dennison’s unimpressive 4.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

Avery Dennison’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 15.3× forward P/E (or $163.83 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,552% between June 2020 and June 2025). Find your next big winner with StockStory today.