RPC trades at $5.82 and has moved in lockstep with the market. Its shares have returned 6.3% over the last six months while the S&P 500 has gained 6.1%.

Is there a buying opportunity in RPC, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is RPC Not Exciting?

We’re cautious about RPC. Here are three reasons why RES doesn’t excite us, plus one stock we’d rather own.

1. Fewer Distribution Channels than Larger Competitors

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks.

RPC’s $1.75 billion of revenue in the last year is pretty small for the industry, suggesting the company is a subscale business in an industry where scale matters.

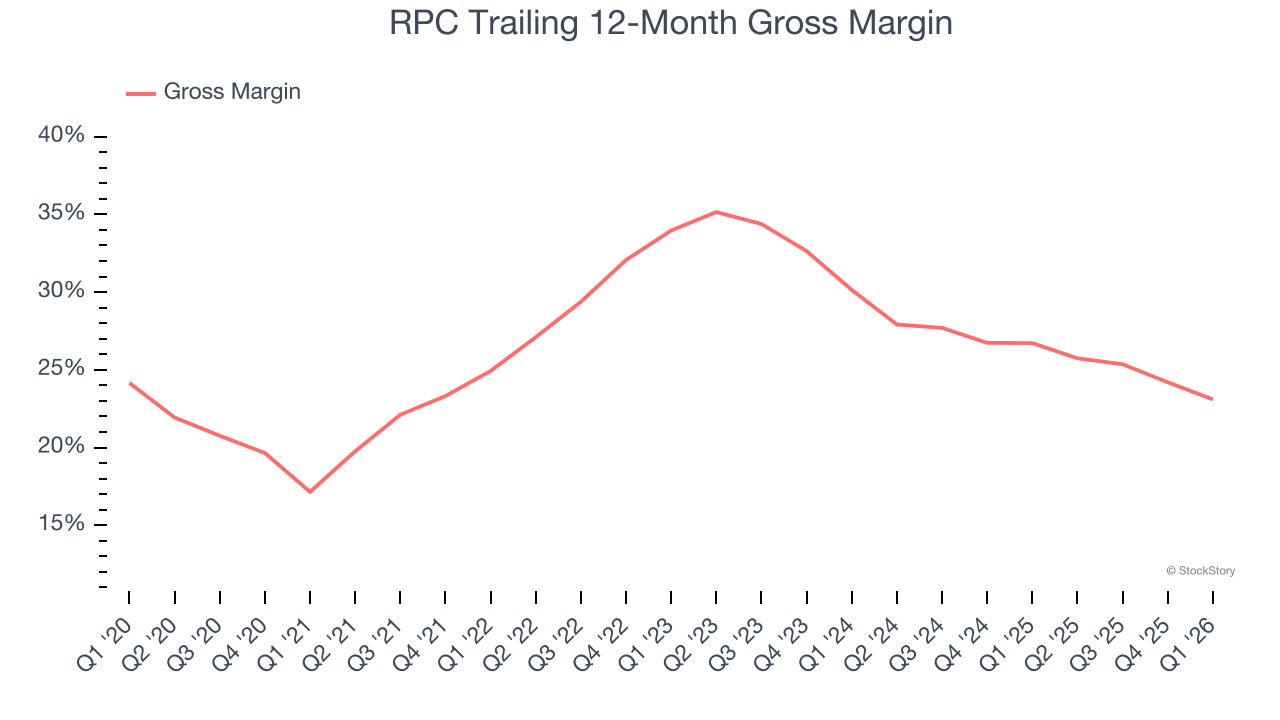

2. Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

RPC, which averaged 28.1% gross margin over the last five years, exhibited bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

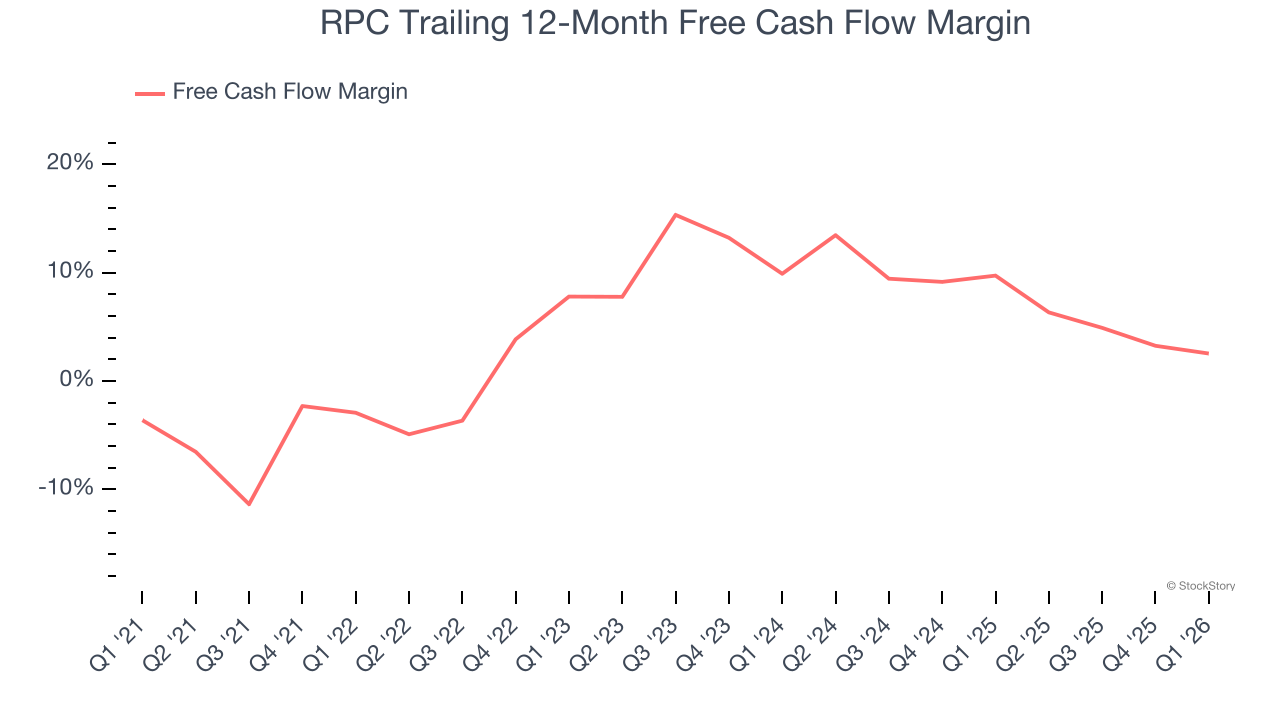

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

RPC has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 5.9%, below what we’d expect for an upstream and integrated energy business.

Final Judgment

RPC isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 27.1× forward P/E (or $5.82 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of RPC

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.