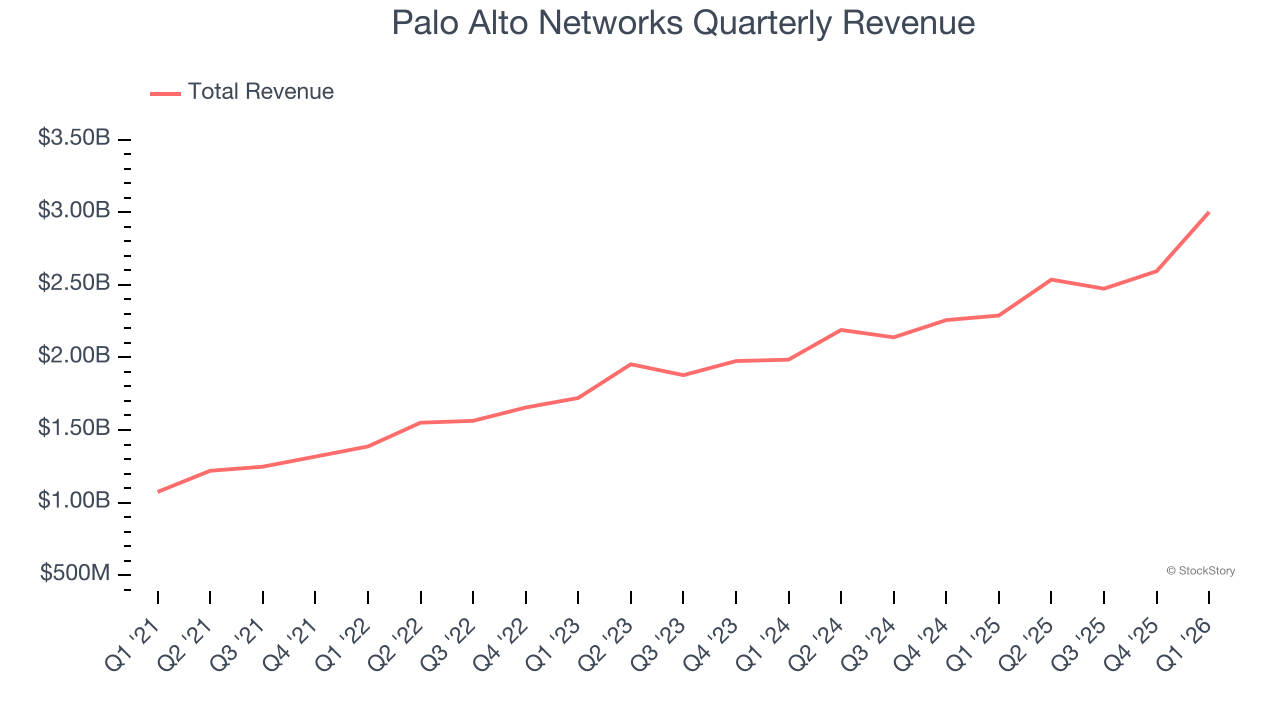

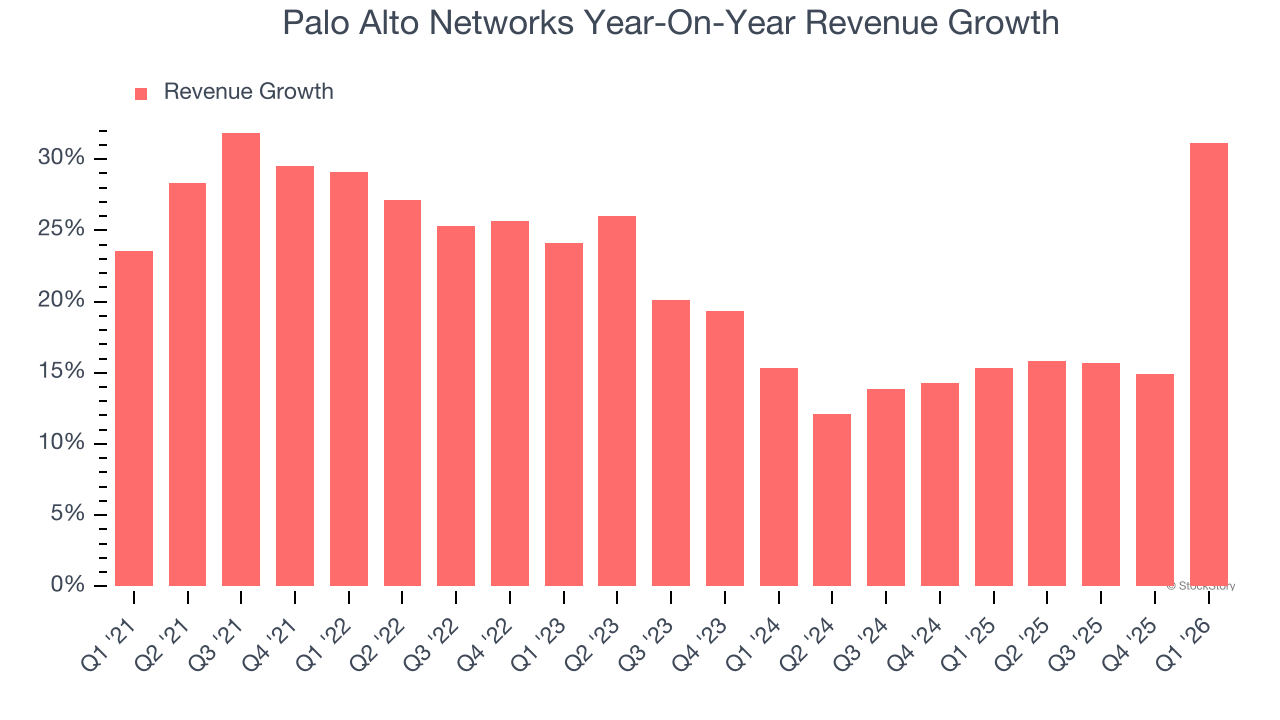

Cybersecurity platform provider Palo Alto Networks (NASDAQ: PANW) announced better-than-expected revenue in Q1 CY2026, with sales up 31.1% year on year to $3.00 billion. Guidance for next quarter’s revenue was optimistic at $3.35 billion at the midpoint, 2.1% above analysts’ estimates. Its non-GAAP profit of $0.85 per share was 6.7% above analysts’ consensus estimates.

Is now the time to buy Palo Alto Networks? Find out by accessing our full research report, it’s free.

Palo Alto Networks (PANW) Q1 CY2026 Highlights:

- Revenue: $3.00 billion vs analyst estimates of $2.94 billion (31.1% year-on-year growth, 2% beat)

- Adjusted EPS: $0.85 vs analyst estimates of $0.80 (6.7% beat)

- Adjusted Operating Income: $814 million vs analyst estimates of $764.7 million (27.1% margin, 6.5% beat)

- Revenue Guidance for Q2 CY2026 is $3.35 billion at the midpoint, above analyst estimates of $3.28 billion

- Management raised its full-year Adjusted EPS guidance to $3.78 at the midpoint, a 2.9% increase

- Operating Margin: -6.1%, down from 9.6% in the same quarter last year

- Free Cash Flow Margin: 31.8%, up from 14.8% in the previous quarter

- Market Capitalization: $243.7 billion

"Q3 was a standout quarter for Palo Alto Networks, with accelerating organic bookings growth as customers turn to us to secure their AI deployments at scale," said Nikesh Arora, chairman and chief executive officer of Palo Alto Networks.

Company Overview

Founded in 2005 by security visionary Nir Zuk who sought to reimagine firewall technology, Palo Alto Networks (NASDAQ: PANW) provides AI-powered cybersecurity platforms that protect organizations' networks, clouds, and endpoints from sophisticated threats.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Palo Alto Networks’s 21.6% annualized revenue growth over the last five years was decent. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Palo Alto Networks’s annualized revenue growth of 16.7% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Palo Alto Networks reported wonderful year-on-year revenue growth of 31.1%, and its $3.00 billion of revenue exceeded Wall Street’s estimates by 2%. Company management is currently guiding for a 32.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping for a company of its scale and indicates its newer products and services will fuel better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Palo Alto Networks’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Palo Alto Networks’s Q1 Results

It was great to see Palo Alto Networks’s full-year EPS guidance top analysts’ expectations. We were also glad its EPS guidance for next quarter exceeded Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 8.4% to $325.46 immediately following the results.

Sure, Palo Alto Networks had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).