Over the last six months, IQVIA’s shares have sunk to $177.52, producing a disappointing 19.8% loss - a stark contrast to the S&P 500’s 12.4% gain. This might have investors contemplating their next move.

Is there a buying opportunity in IQVIA, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is IQVIA Not Exciting?

Even though the stock has become cheaper, we’re swiping left on IQVIA for now. Here are three reasons why there are better opportunities than IQV, plus one stock we’d rather own.

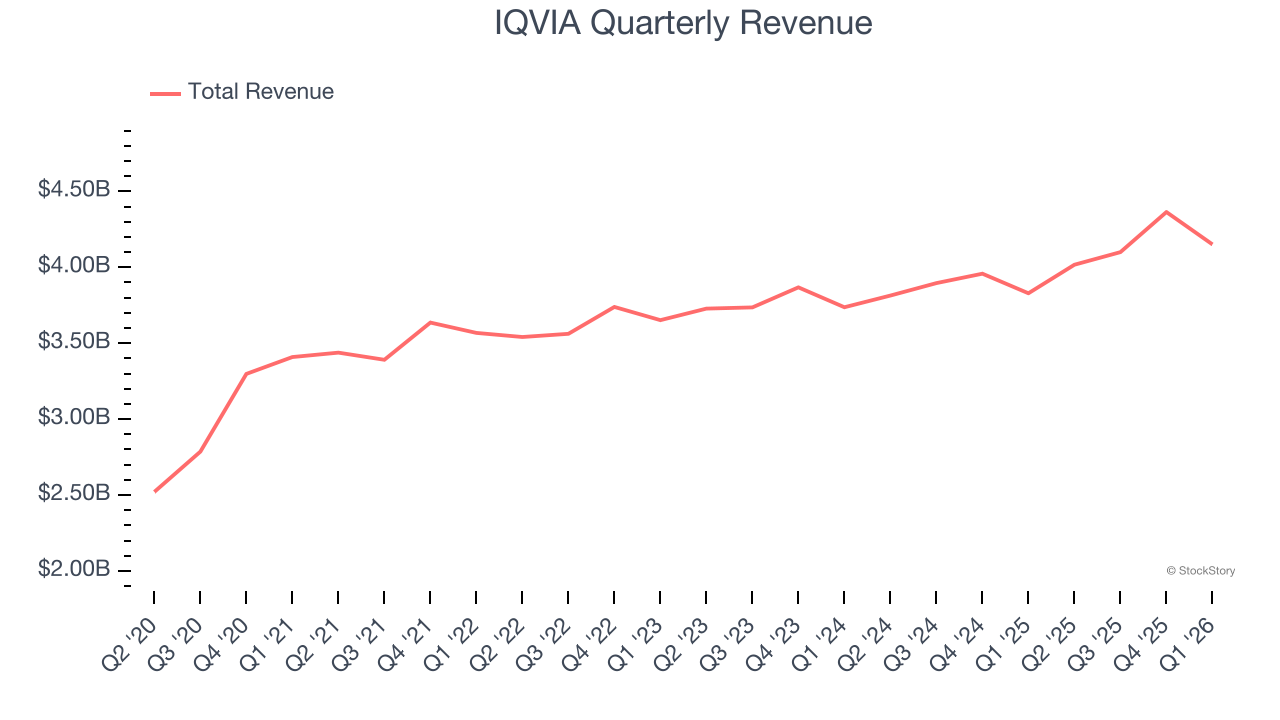

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, IQVIA’s 6.7% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the healthcare sector.

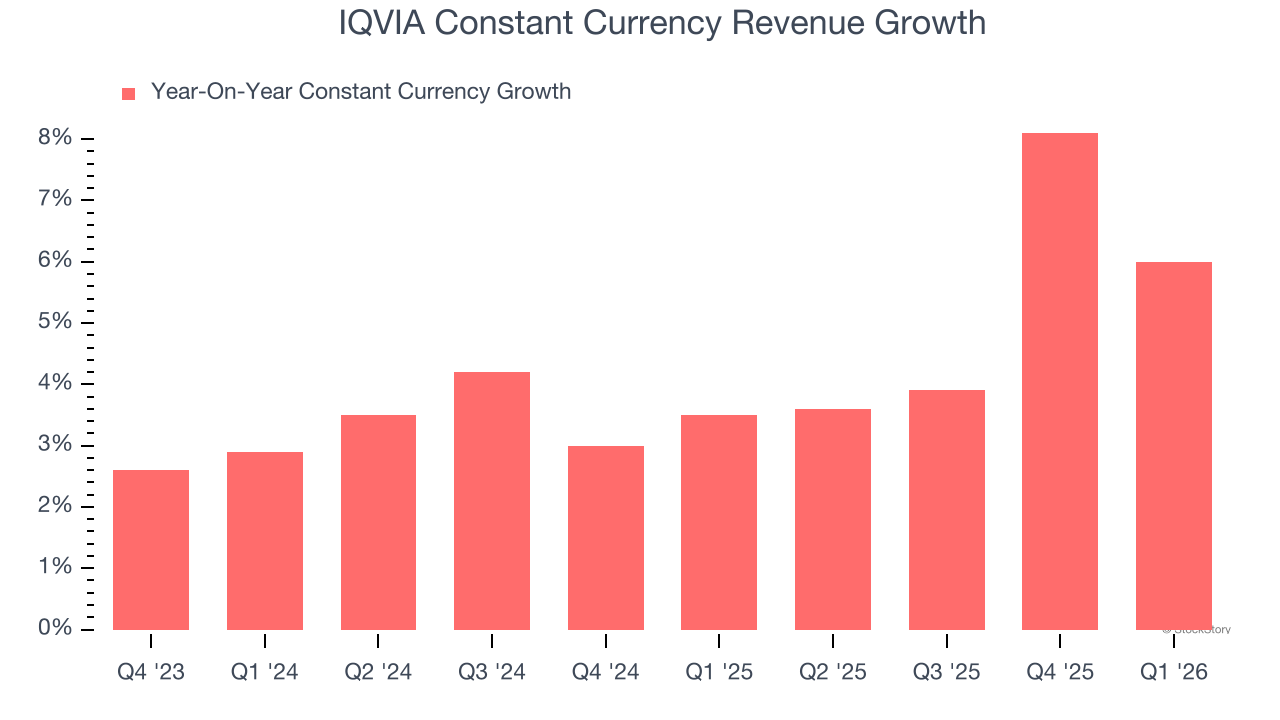

2. Weak Constant Currency Growth Points to Soft Demand

We can better understand Drug Development Inputs & Services companies by analyzing their constant currency revenue. This metric excludes currency movements, which are outside of IQVIA’s control and are not indicative of underlying demand.

Over the last two years, IQVIA’s constant currency revenue averaged 4.5% year-on-year growth. This performance slightly lagged the sector and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

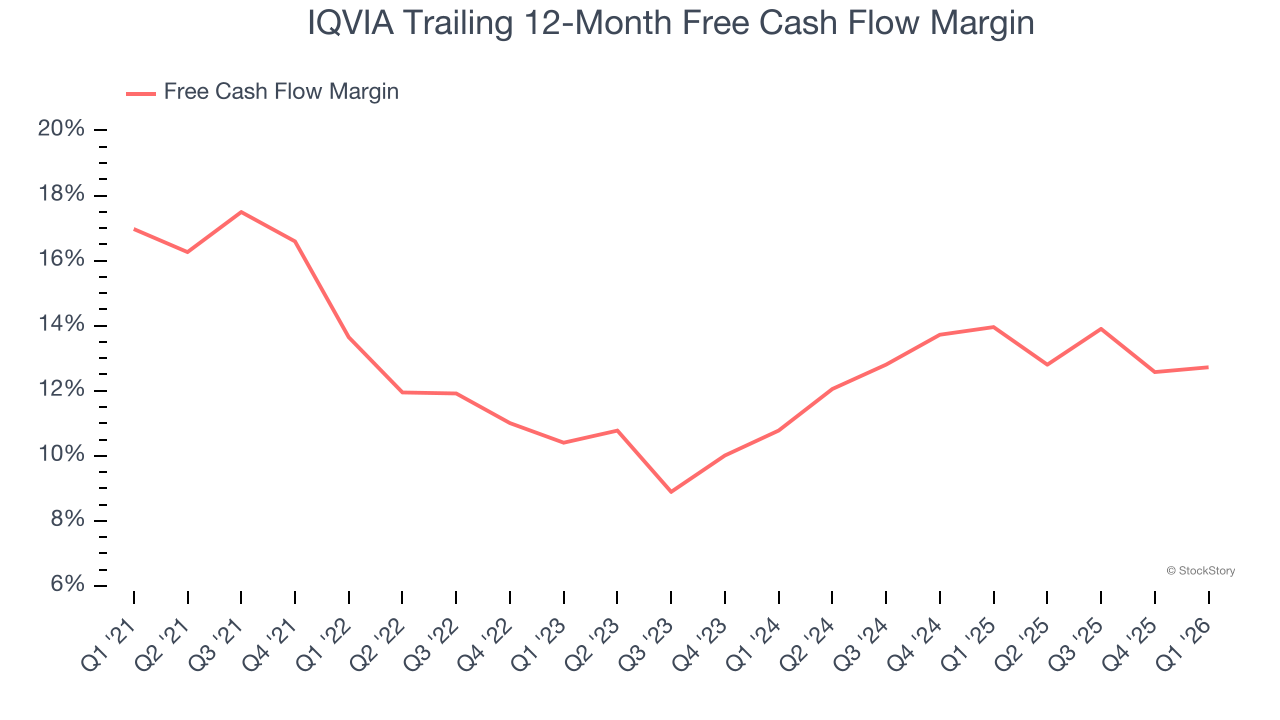

3. Free Cash Flow Margin Stuck in Neutral

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, IQVIA’s margin was unchanged over the last five years, showing it couldn’t improve. Its free cash flow margin for the trailing 12 months was 12.7%.

Final Judgment

IQVIA’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 13.6× forward P/E (or $177.52 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We’re pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Like More Than IQVIA

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.