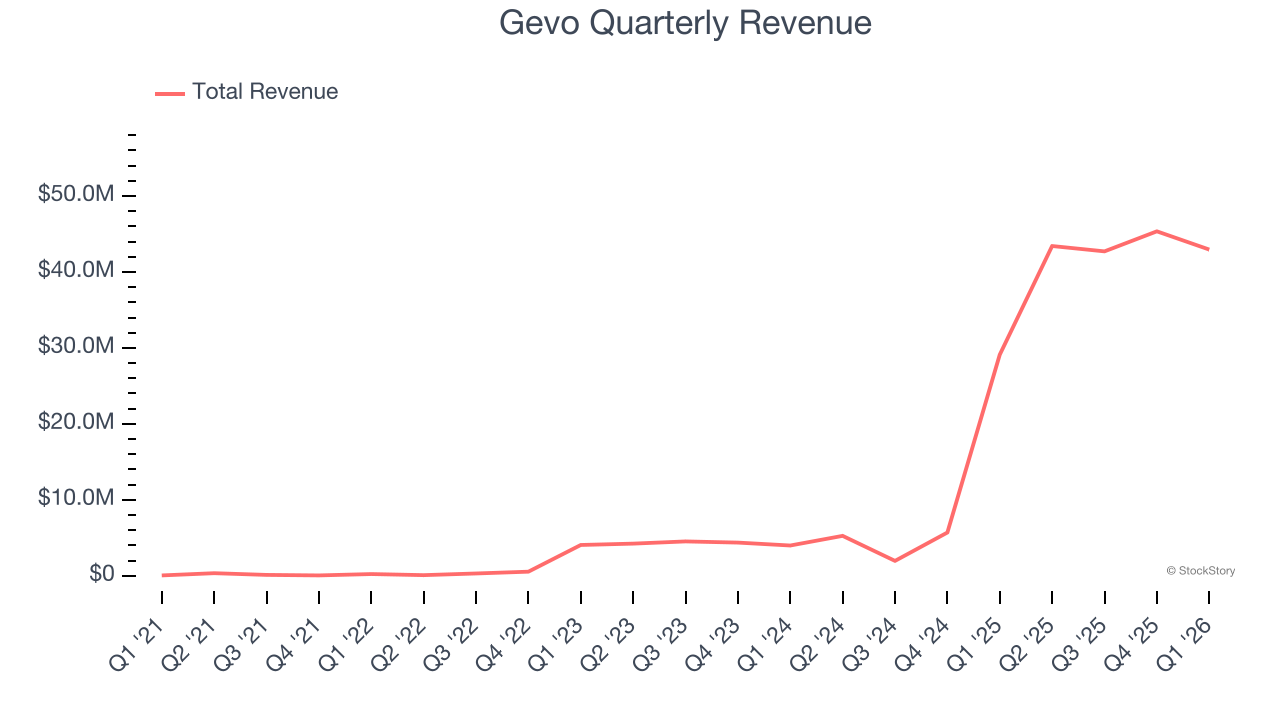

Renewable fuels producer Gevo (NASDAQ: GEVO) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 47.5% year on year to $42.95 million. Its GAAP loss of $0.09 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Gevo? Find out by accessing our full research report, it’s free.

Gevo (GEVO) Q1 CY2026 Highlights:

- Revenue: $42.95 million vs analyst estimates of $45.21 million (47.5% year-on-year growth, 5% miss)

- EPS (GAAP): -$0.09 vs analyst estimates of -$0.02 (significant miss)

- Adjusted EBITDA: $8.53 million vs analyst estimates of $7.89 million (19.9% margin, 8.1% beat)

- Operating Margin: -11.4%, up from -69.2% in the same quarter last year

- Free Cash Flow was -$30.02 million compared to -$29.88 million in the same quarter last year

- Market Capitalization: $485.1 million

“We continue to deliver solid quarterly results while strengthening and expanding our low-carbon ethanol and carbon business to provide a solid foundation for Alcohol-to-Jet (“ATJ”) growth,” said Paul Bloom, chief executive officer of Gevo.

Company Overview

Operating one of the largest dairy-based renewable natural gas facilities in the United States, Gevo (NASDAQ: GEVO) produces sustainable aviation fuel and other renewable hydrocarbon fuels from plant-based feedstocks like corn.

Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Thankfully, Gevo’s 151% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Gevo’s annualized revenue growth of 19% over the last ten years is below its five-year trend, but we still think the results suggest decent demand.

This quarter, Gevo achieved a magnificent 47.5% year-on-year revenue growth rate, but its $42.95 million of revenue fell short of Wall Street’s lofty estimates.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

Although Gevo was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average EBITDA margin of negative 81.2% over the last five years.

On the plus side, Gevo’s EBITDA margin rose over the last year, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q1, Gevo generated an EBITDA margin profit margin of 19.9%, up 72.6 percentage points year on year. This increase was a welcome development and shows it was more efficient. This adjusted EBITDA beat Wall Street’s estimates by 8.1%.

Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Gevo’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 214%, meaning it lit $213.84 of cash on fire for every $100 in revenue.

While the level of free cash flow margins is important, their consistency matters just as much.

Gevo’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 3.3 (lower is better), indicating excellent insulation from commodity swings. This stability supports superior capital access in downturns and positions Gevo to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Gevo? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Gevo burned through $30.02 million of cash in Q1, equivalent to a negative 69.9% margin. The company’s cash burn was in line with the same quarter last year, and it’s unlikely that Gevo will have an attractive free cash flow profile anytime soon.

Key Takeaways from Gevo’s Q1 Results

We enjoyed seeing Gevo beat analysts’ EBITDA expectations this quarter. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4.3% to $1.94 immediately following the results.

The latest quarter from Gevo’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).