As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the healthcare technology for providers industry, including Omnicell (NASDAQ: OMCL) and its peers.

The healthcare technology sector provides software and data analytics to help hospitals and clinics streamline operations and improve patient outcomes, often through value-based care models. Future growth is expected as providers prioritize digital transformation to manage rising costs and patient demands. Tailwinds include the adoption of AI-driven tools and government incentives for digitization. There are challenges as well, including long sales cycles and slow adoption by providers, who may be resistance to change. Tightening hospital budgets and cybersecurity threats are additional risks that could slow adoption.

The 4 healthcare technology for providers stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 3.6% on average since the latest earnings results.

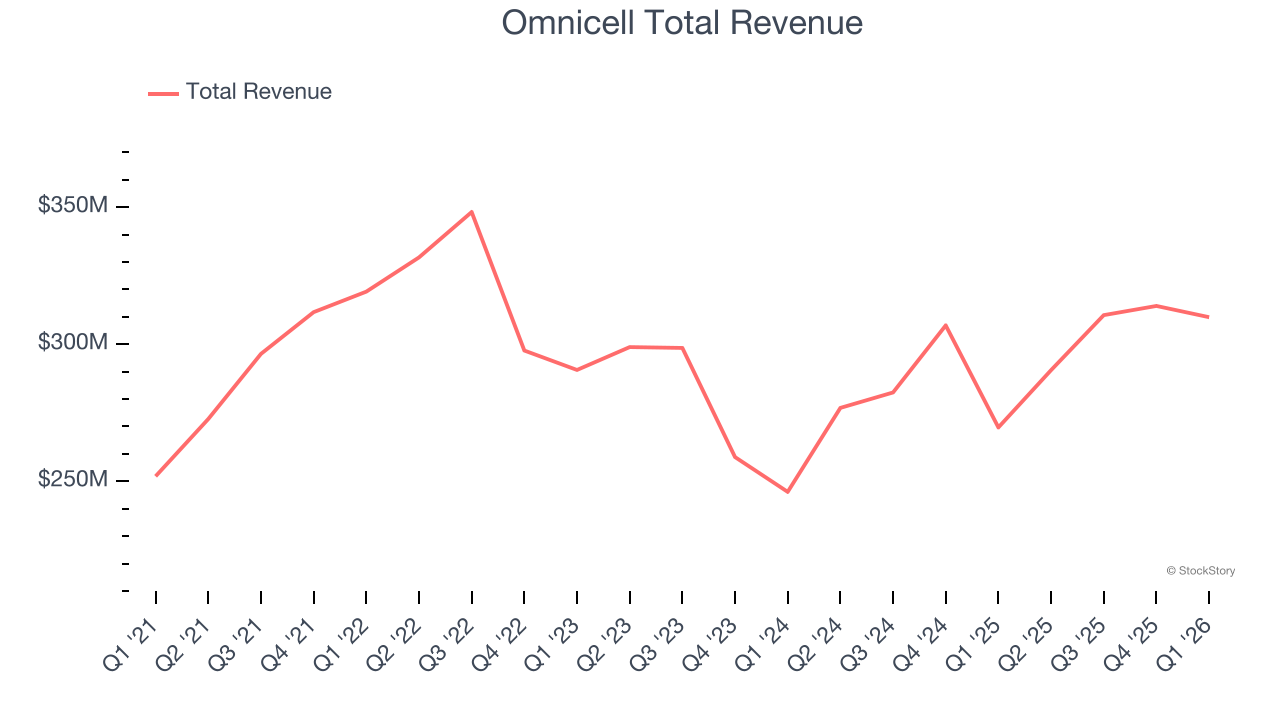

Best Q1: Omnicell (NASDAQ: OMCL)

Driven by the vision of an "Autonomous Pharmacy" with zero medication errors, Omnicell (NASDAQ: OMCL) provides medication management automation and adherence tools that help healthcare systems and pharmacies reduce errors and improve efficiency.

Omnicell reported revenues of $309.9 million, up 14.9% year on year. This print exceeded analysts’ expectations by 1.8%. Overall, it was an exceptional quarter for the company with EBITDA guidance for next quarter exceeding analysts’ expectations and a beat of analysts’ EPS estimates.

“We delivered a strong start to 2026, driven by solid execution and sustained demand for our points of care solutions,” said Randall Lipps, chairman, president, chief executive officer, and founder of Omnicell.

Interestingly, the stock is up 16.5% since reporting and currently trades at $43.85.

Is now the time to buy Omnicell? Access our full analysis of the earnings results here, it’s free.

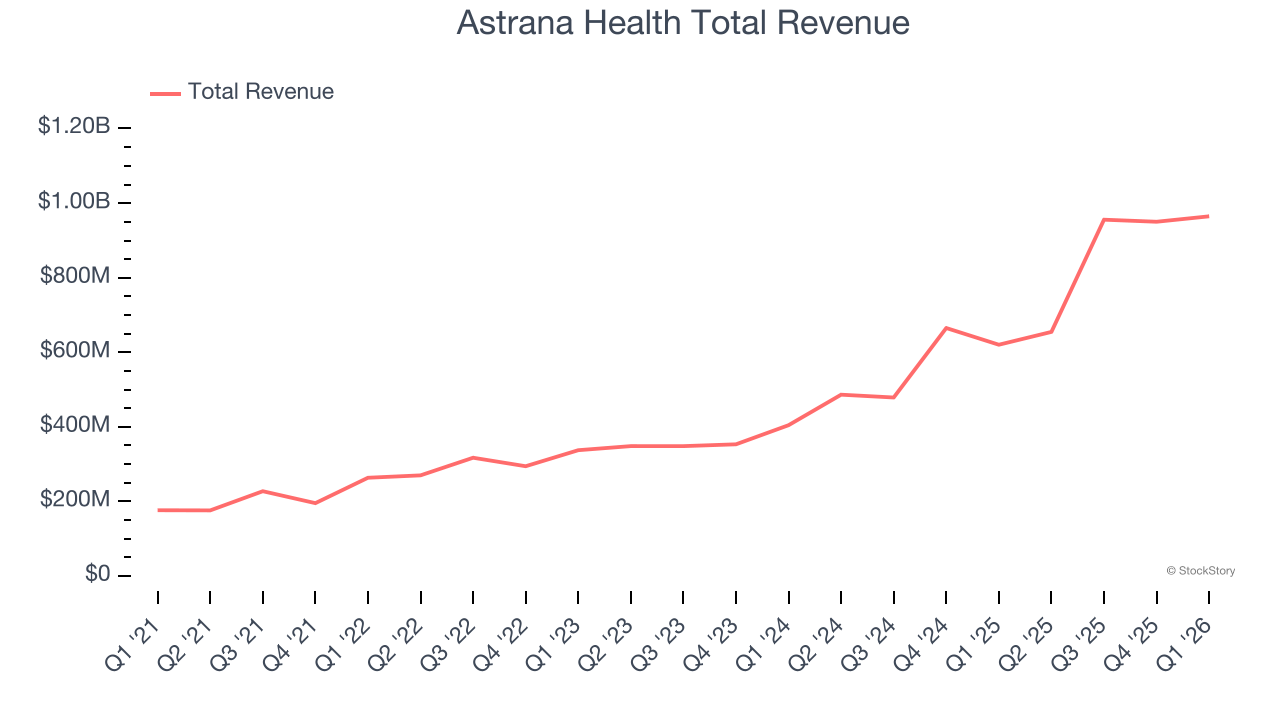

Astrana Health (NASDAQ: ASTH)

Formerly known as Apollo Medical Holdings until early 2024, Astrana Health (NASDAQ: ASTH) operates a technology-powered healthcare platform that enables physicians to deliver coordinated care while successfully participating in value-based payment models.

Astrana Health reported revenues of $965.1 million, up 55.6% year on year, outperforming analysts’ expectations by 1.9%. The business had a satisfactory quarter with a beat of analysts’ EPS estimates but full-year revenue guidance slightly missing analysts’ expectations.

Astrana Health delivered the fastest revenue growth among its peers. The market seems content with the results as the stock is up 3.5% since reporting. It currently trades at $37.36.

Is now the time to buy Astrana Health? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Evolent Health (NYSE: EVH)

Founded in 2011 to transform how healthcare is delivered to patients with complex needs, Evolent Health (NYSE: EVH) provides specialty care management services and technology solutions that help health plans and providers deliver better care for patients with complex conditions.

Evolent Health reported revenues of $496.2 million, up 2.6% year on year, falling short of analysts’ expectations by 6.9%. It was a mixed quarter as it posted a beat of analysts’ EPS estimates but a significant miss of analysts’ revenue estimates.

Evolent Health delivered the highest full-year guidance raise but had the weakest performance against analyst estimates and slowest revenue growth in the group. The stock is flat since the results and currently trades at $3.84.

Read our full analysis of Evolent Health’s results here.

Privia Health (NASDAQ: PRVA)

Operating in 13 states and the District of Columbia with over 4,300 providers serving more than 4.8 million patients, Privia Health (NASDAQ: PRVA) is a technology-driven company that helps physicians optimize their practices, improve patient experiences, and transition to value-based care models.

Privia Health reported revenues of $603.8 million, up 25.8% year on year. This result surpassed analysts’ expectations by 7.4%. Aside from that, it was a mixed quarter as it also recorded a solid beat of analysts’ revenue estimates but a significant miss of analysts’ EPS estimates.

Privia Health achieved the biggest analyst estimates beat among its peers. The stock is down 5.6% since reporting and currently trades at $22.64.

Read our full, actionable report on Privia Health here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.