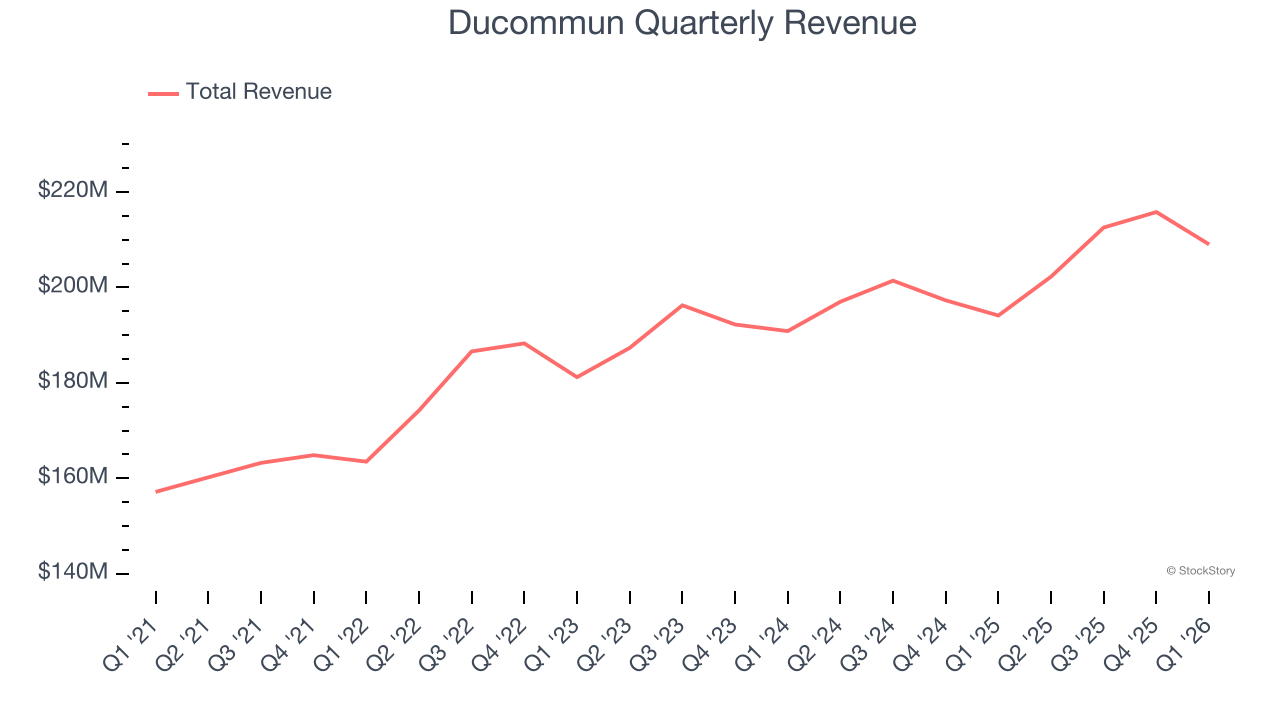

Aerospace and defense company Ducommun (NYSE: DCO) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 7.7% year on year to $209 million. Its non-GAAP profit of $0.75 per share was 4% above analysts’ consensus estimates.

Is now the time to buy Ducommun? Find out by accessing our full research report, it’s free.

Ducommun (DCO) Q1 CY2026 Highlights:

- Revenue: $209 million vs analyst estimates of $199.4 million (7.7% year-on-year growth, 4.8% beat)

- Adjusted EPS: $0.75 vs analyst estimates of $0.72 (4% beat)

- Adjusted EBITDA: $35.38 million vs analyst estimates of $31.44 million (16.9% margin, 12.5% beat)

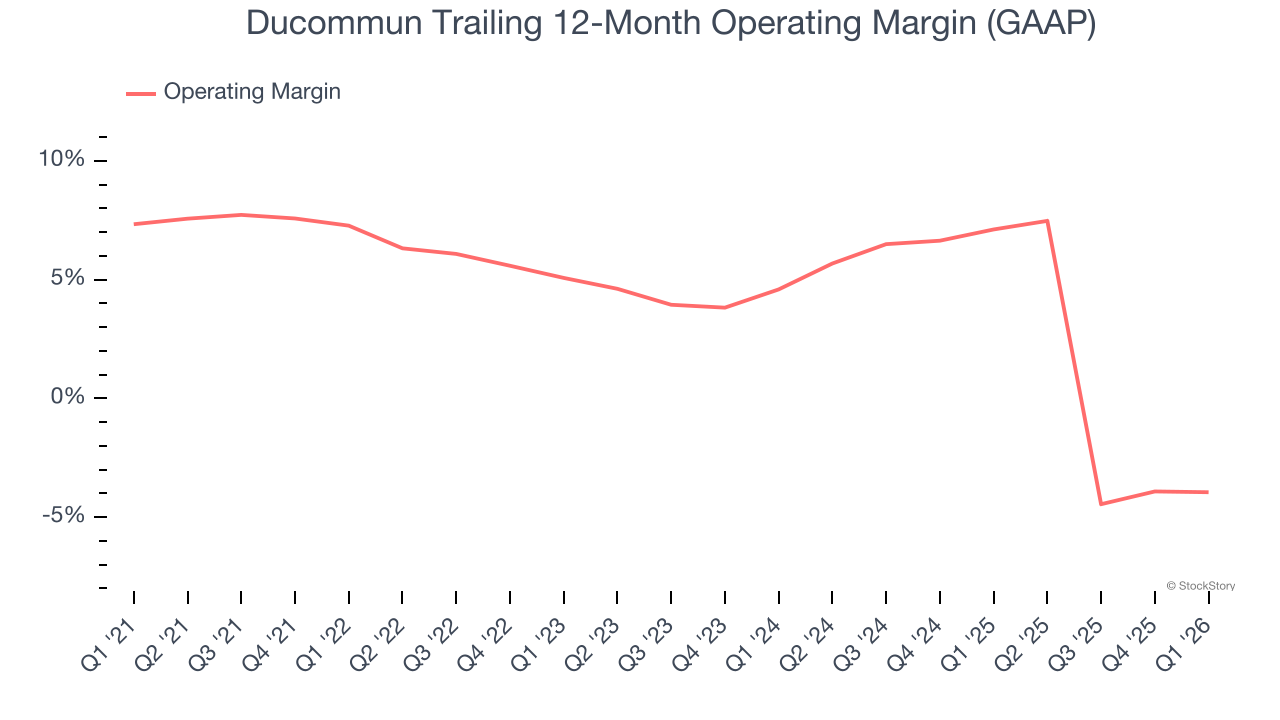

- Operating Margin: 7.5%, down from 8.5% in the same quarter last year

- Market Capitalization: $2.12 billion

“An excellent quarter and strong start to 2026 for Ducommun. Our team continued to make great progress towards our VISION 2027 goals with another record for revenue during the first quarter along with strong gross margin and Adjusted EBITDA margins. Net revenue grew a very healthy 9%, led by strength in commercial aerospace which we have been waiting for, along with gains in our defense business,” said Stephen G. Oswald, chairman, president and chief executive officer.

Company Overview

California’s oldest company, Ducommun (NYSE: DCO) is a provider of engineering and manufacturing services for high-performance products primarily within the aerospace and defense industries.

Revenue Growth

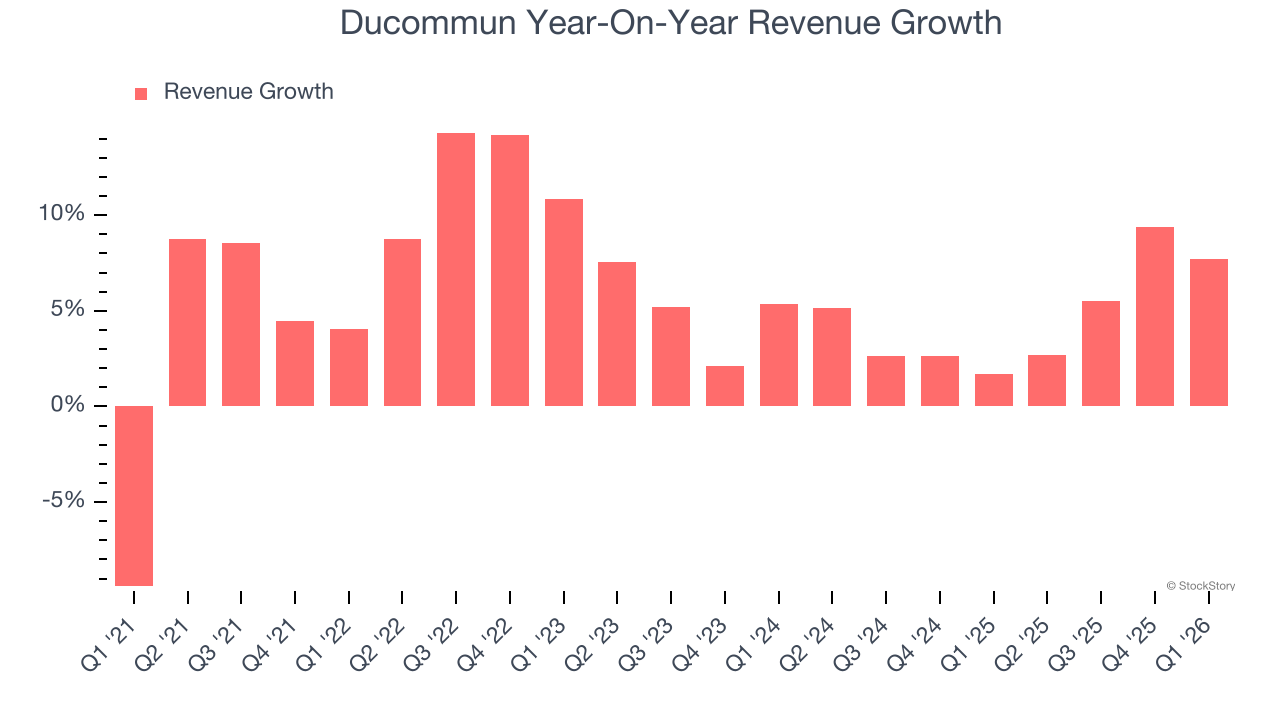

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Ducommun’s sales grew at a mediocre 6.5% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Ducommun’s recent performance shows its demand has slowed as its annualized revenue growth of 4.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Ducommun reported year-on-year revenue growth of 7.7%, and its $209 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 7.9% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and suggests its newer products and services will catalyze better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Ducommun was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.8% was weak for an industrials business.

Analyzing the trend in its profitability, Ducommun’s operating margin decreased by 11.2 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Ducommun’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, Ducommun generated an operating margin profit margin of 7.5%, down 1 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

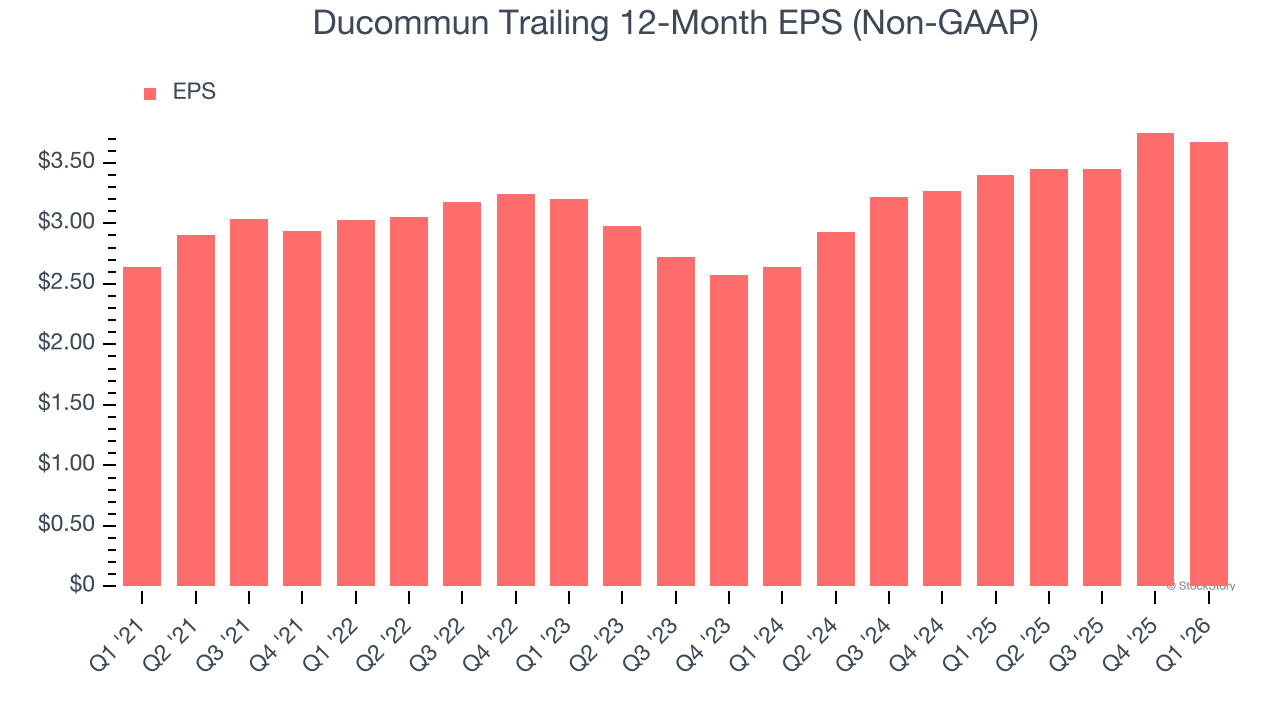

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Ducommun’s unimpressive 6.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Ducommun, its two-year annual EPS growth of 17.9% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Ducommun reported adjusted EPS of $0.75, down from $0.83 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4%. Over the next 12 months, Wall Street expects Ducommun’s full-year EPS of $3.67 to grow 25%.

Key Takeaways from Ducommun’s Q1 Results

We were impressed by how significantly Ducommun blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $140.68 immediately following the results.

So should you invest in Ducommun right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).