In a sliding market, Rivian has defied the odds, trading up to $15.14 per share. Its 15.3% gain since October 2025 has outpaced the S&P 500’s 2.1% drop. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Rivian, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Rivian Not Exciting?

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons why RIVN doesn't excite us and a stock we'd rather own.

1. Demand Slips as Sales Volumes Slide

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Automobile Manufacturing company because there’s a ceiling to what customers will pay.

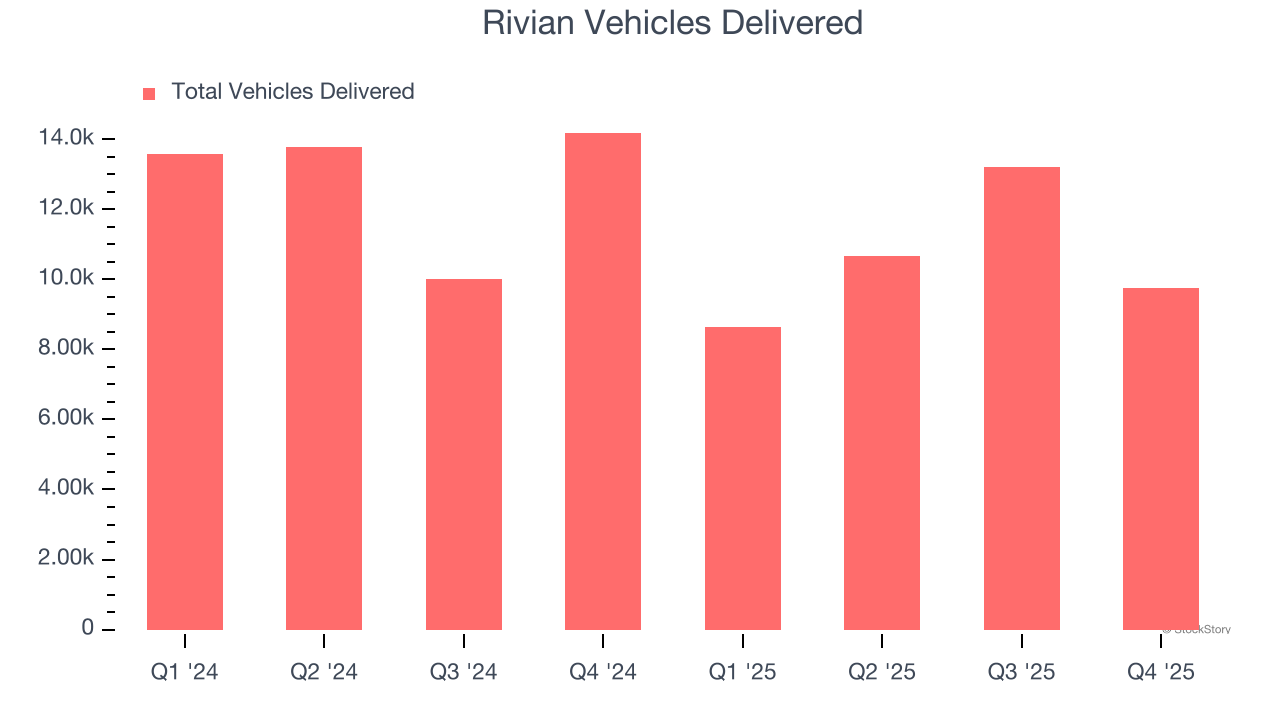

Rivian’s vehicles delivered came in at 9,745 in the latest quarter, and they declined by 29.5% annually over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Rivian might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

2. Cash Burn Ignites Concerns

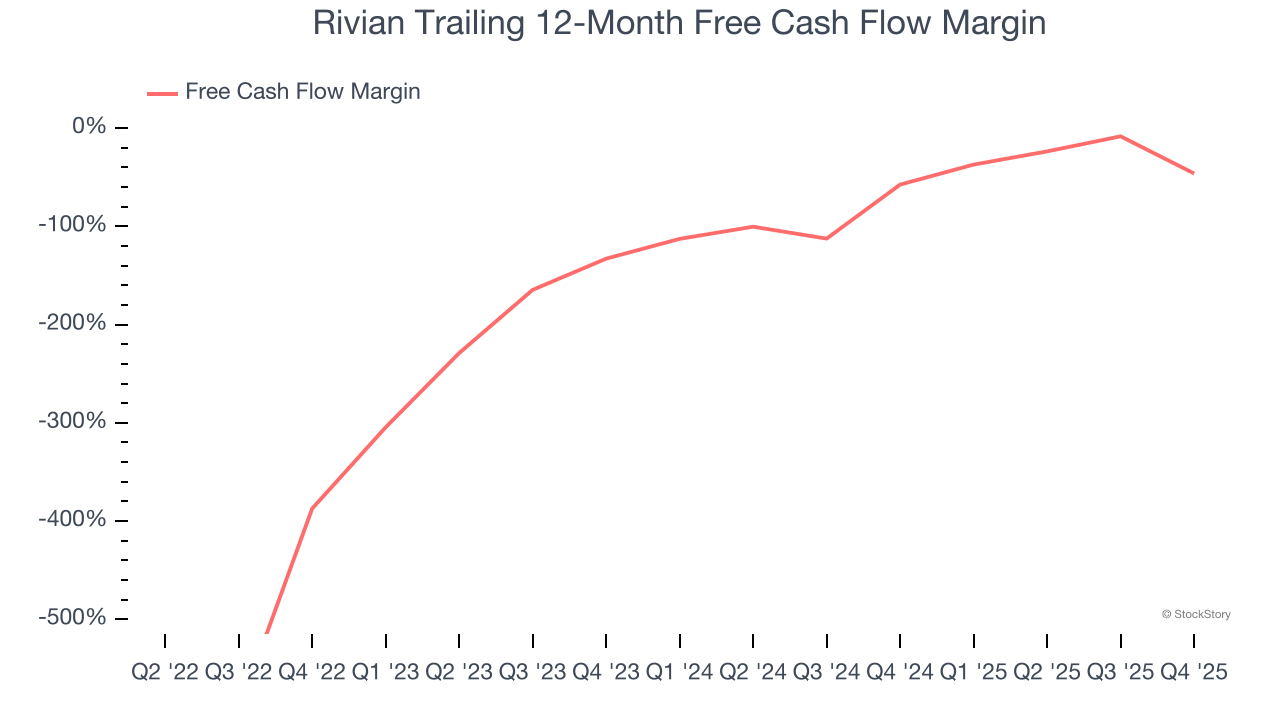

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Rivian’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 123%, meaning it lit $123.32 of cash on fire for every $100 in revenue.

3. Restricted Access to Capital Increases Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

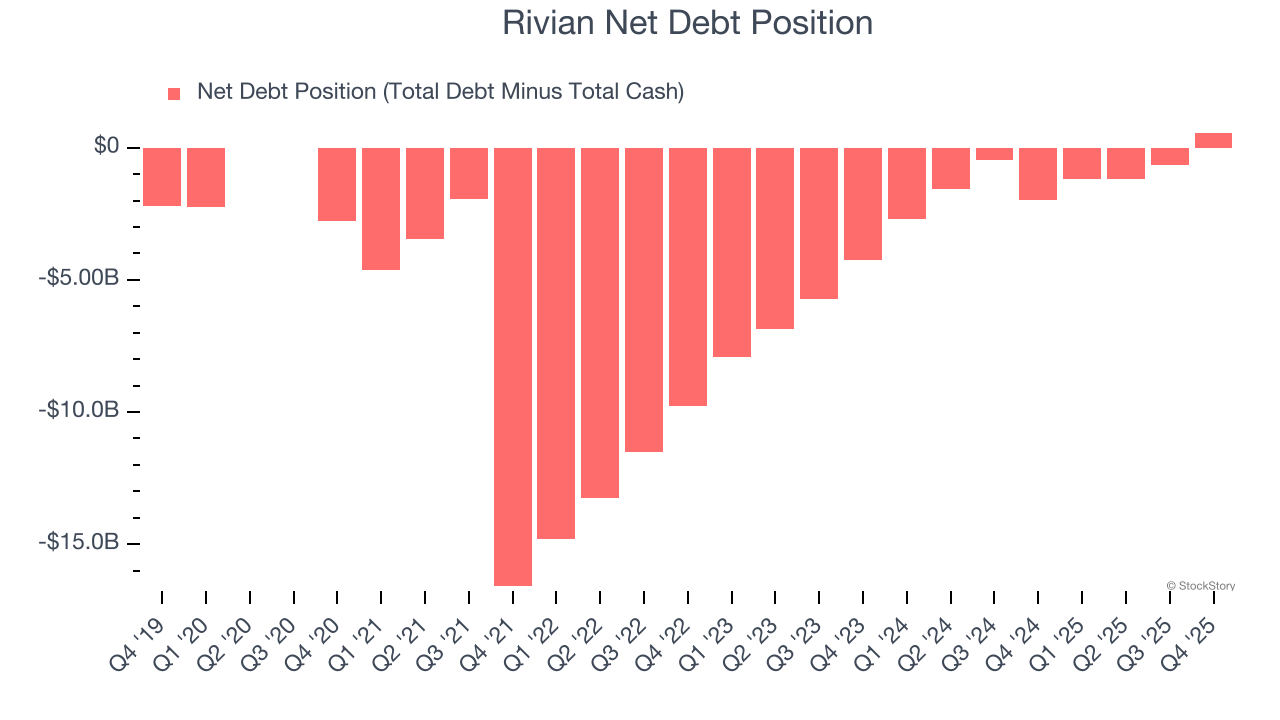

Rivian posted negative $2.06 billion of EBITDA over the last 12 months, and its $6.65 billion of debt exceeds the $6.08 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Rivian if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Rivian can improve its profitability and remain cautious until then.

Final Judgment

Rivian isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at $15.14 per share (or a forward price-to-sales ratio of 2.7×). The market typically values companies like Rivian based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. Let us point you toward one of our top software and edge computing picks.

Stocks We Like More Than Rivian

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.