Since April 2021, the S&P 500 has delivered a total return of 61.3%. But one standout stock has more than doubled the market - over the past five years, Magnolia Oil & Gas has surged 159% to $31 per share. Its momentum hasn’t stopped as it’s also gained 29.7% in the last six months, beating the S&P by 31.6%.

Following the strength, is MGY a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Magnolia Oil & Gas Spark Debate?

Operating over 600,000 net acres primarily in two distinct South Texas regions, Magnolia Oil & Gas (NYSE: MGY) drills and produces oil, natural gas, and natural gas liquids from South Texas formations.

Two Positive Attributes:

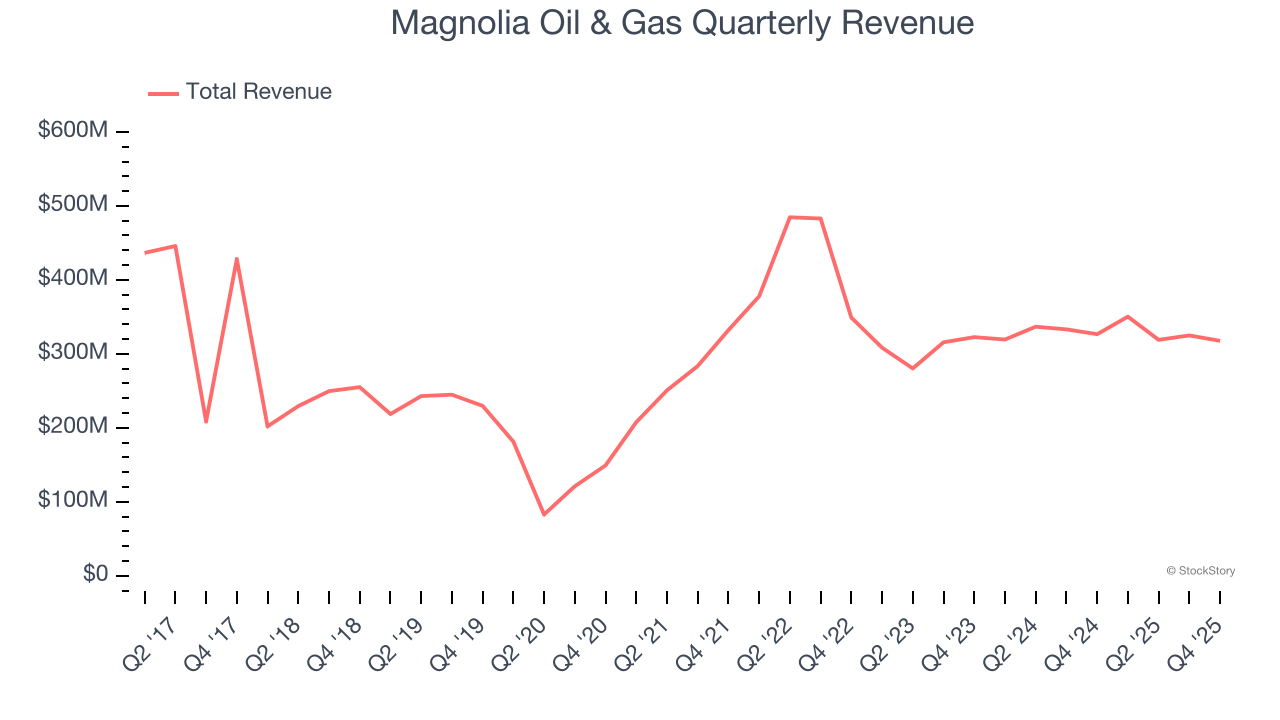

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Thankfully, Magnolia Oil & Gas’s 19.7% annualized revenue growth over the last five years was excellent. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

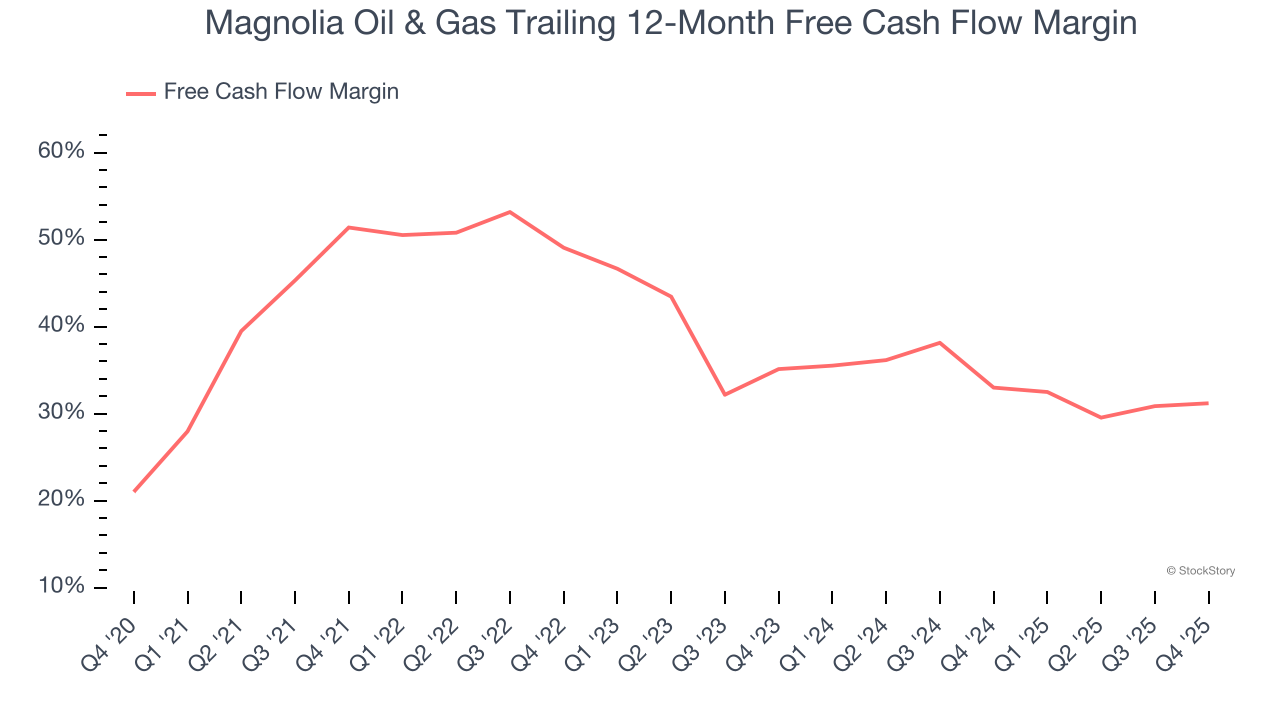

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Magnolia Oil & Gas has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging an eye-popping 40.1% over the last five years.

One Reason to be Careful:

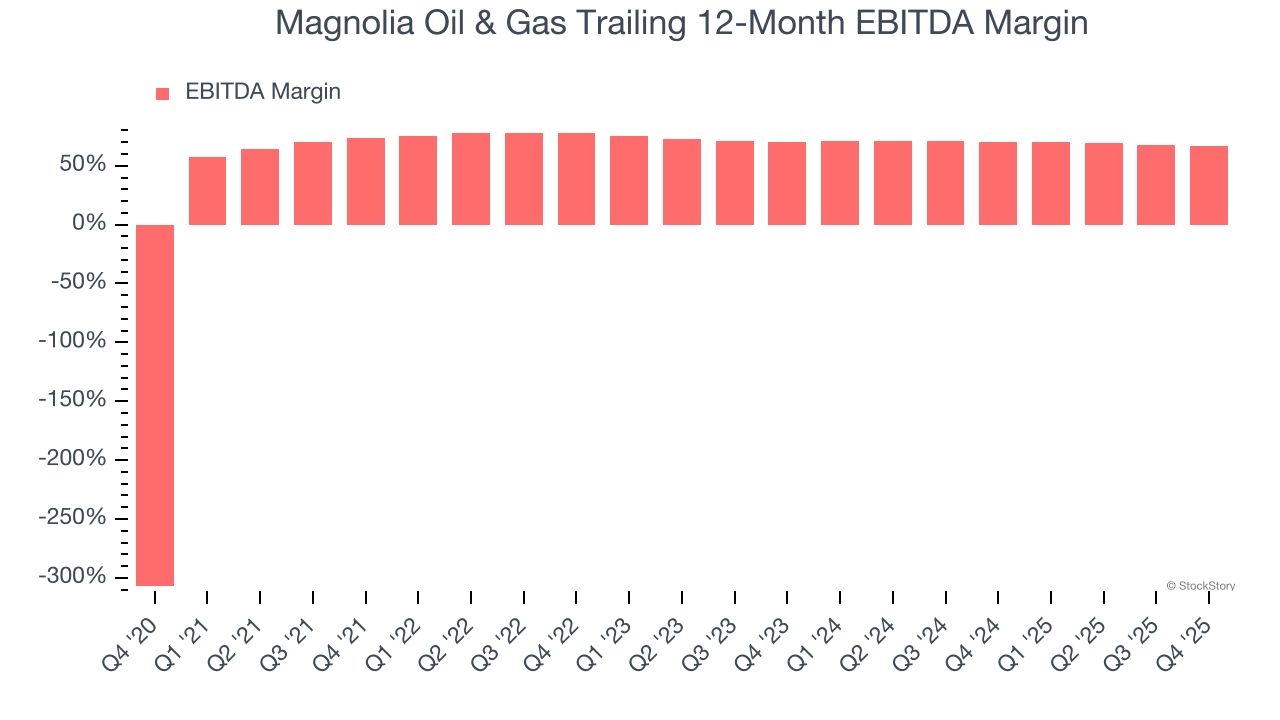

Shrinking EBITDA Margin

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Looking at the trend in its profitability, Magnolia Oil & Gas’s EBITDA margin decreased by 6.7 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Magnolia Oil & Gas become more profitable in the future. Its EBITDA margin for the trailing 12 months was 66.8%.

Final Judgment

Magnolia Oil & Gas’s merits more than compensate for its flaws, and with its shares topping the market in recent months, the stock trades at 12.3× forward P/E (or $31 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.