What a brutal six months it’s been for UnitedHealth. The stock has dropped 22.7% and now trades at $277.17, rattling many shareholders. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy UNH? Find out in our full research report, it’s free.

Why Does UnitedHealth Spark Debate?

With over 100 million people served across its various businesses and a workforce of more than 400,000, UnitedHealth Group (NYSE: UNH) operates a health insurance business and Optum, a healthcare services division that provides everything from pharmacy benefits to primary care.

Two Things to Like:

1. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $447.6 billion in revenue over the past 12 months, UnitedHealth is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

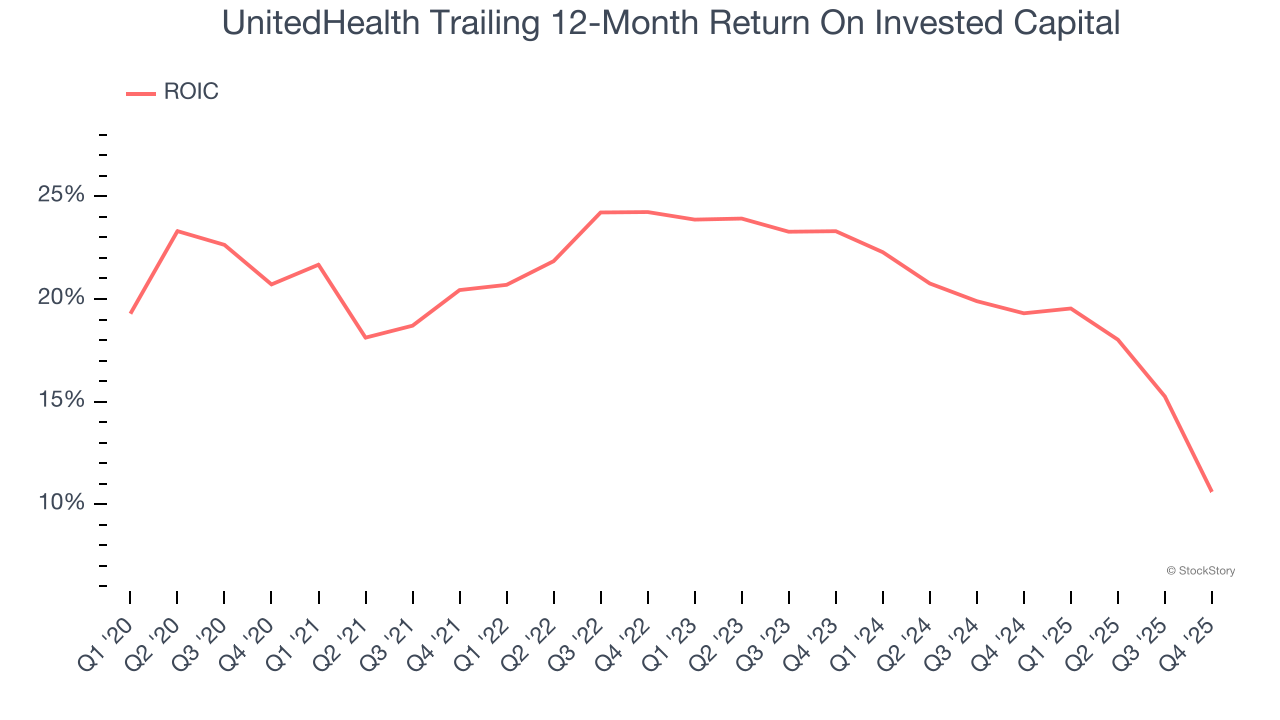

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

UnitedHealth’s five-year average ROIC was 19.6%, beating other healthcare companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

One Reason to be Careful:

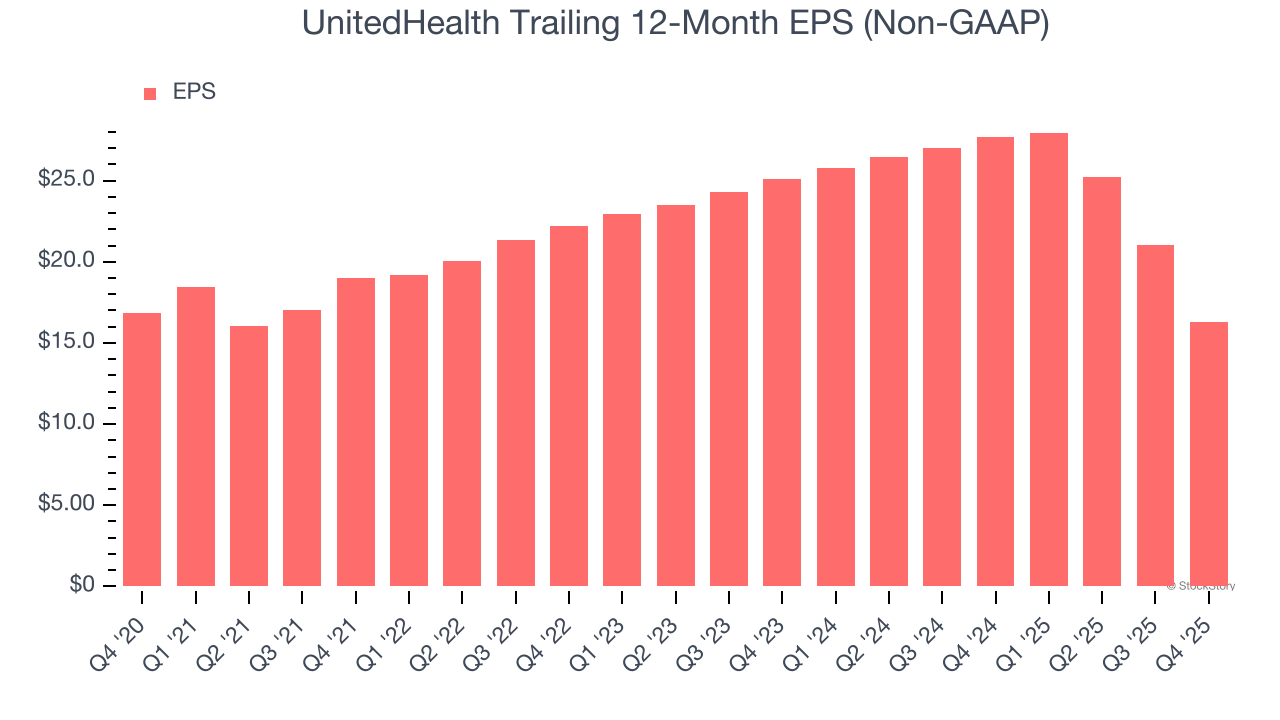

EPS Growth Has Stalled

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

UnitedHealth’s flat EPS over the last five years was below its 11.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

UnitedHealth has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 15.5× forward P/E (or $277.17 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than UnitedHealth

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.