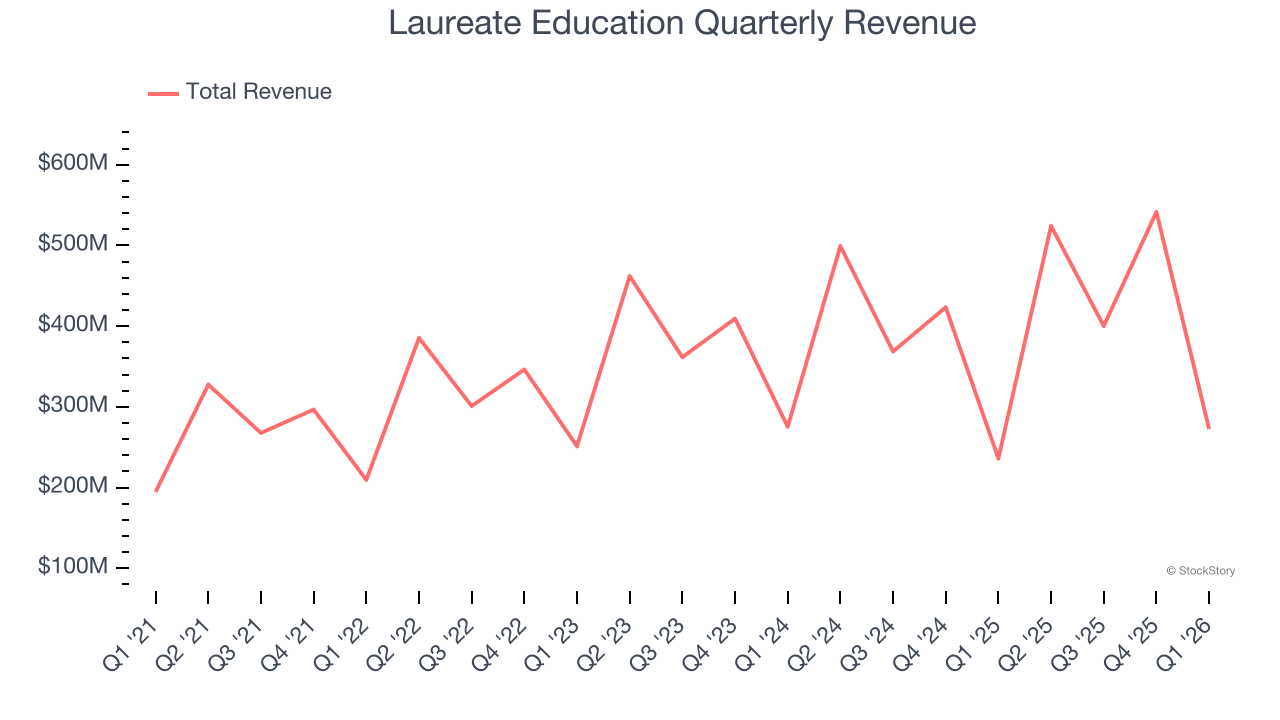

Higher education company Laureate Education (NASDAQ: LAUR) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 15.4% year on year to $272.6 million. On the other hand, the company’s full-year revenue guidance of $1.90 billion at the midpoint came in 0.7% below analysts’ estimates. Its GAAP loss of $0.15 per share was 39.2% above analysts’ consensus estimates.

Is now the time to buy Laureate Education? Find out by accessing our full research report, it’s free.

Laureate Education (LAUR) Q1 CY2026 Highlights:

- Revenue: $272.6 million vs analyst estimates of $266.7 million (15.4% year-on-year growth, 2.2% beat)

- EPS (GAAP): -$0.15 vs analyst estimates of -$0.25 (39.2% beat)

- Adjusted EBITDA: -$2.3 million (-0.8% margin, 143% year-on-year decline)

- The company reconfirmed its revenue guidance for the full year of $1.90 billion at the midpoint

- EBITDA guidance for the full year is $588 million at the midpoint, in line with analyst expectations

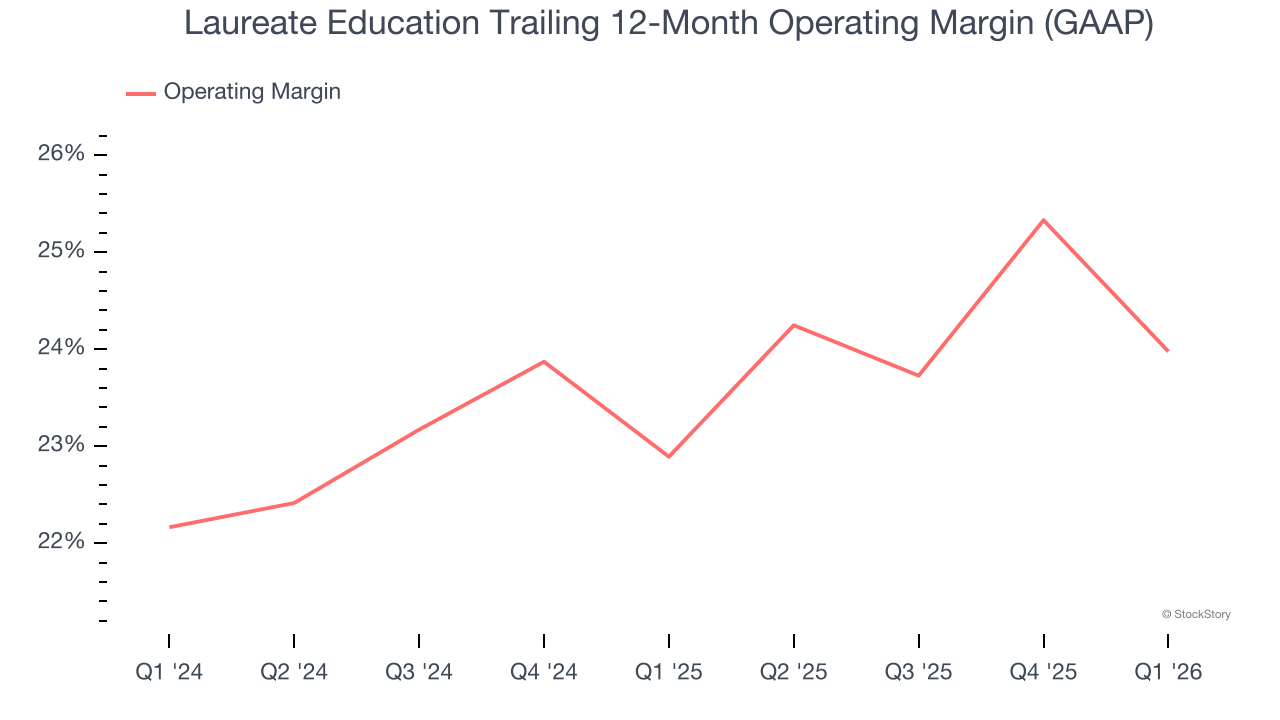

- Operating Margin: -10.1%, down from -5.6% in the same quarter last year

- Free Cash Flow Margin: 19.7%, down from 22.5% in the same quarter last year

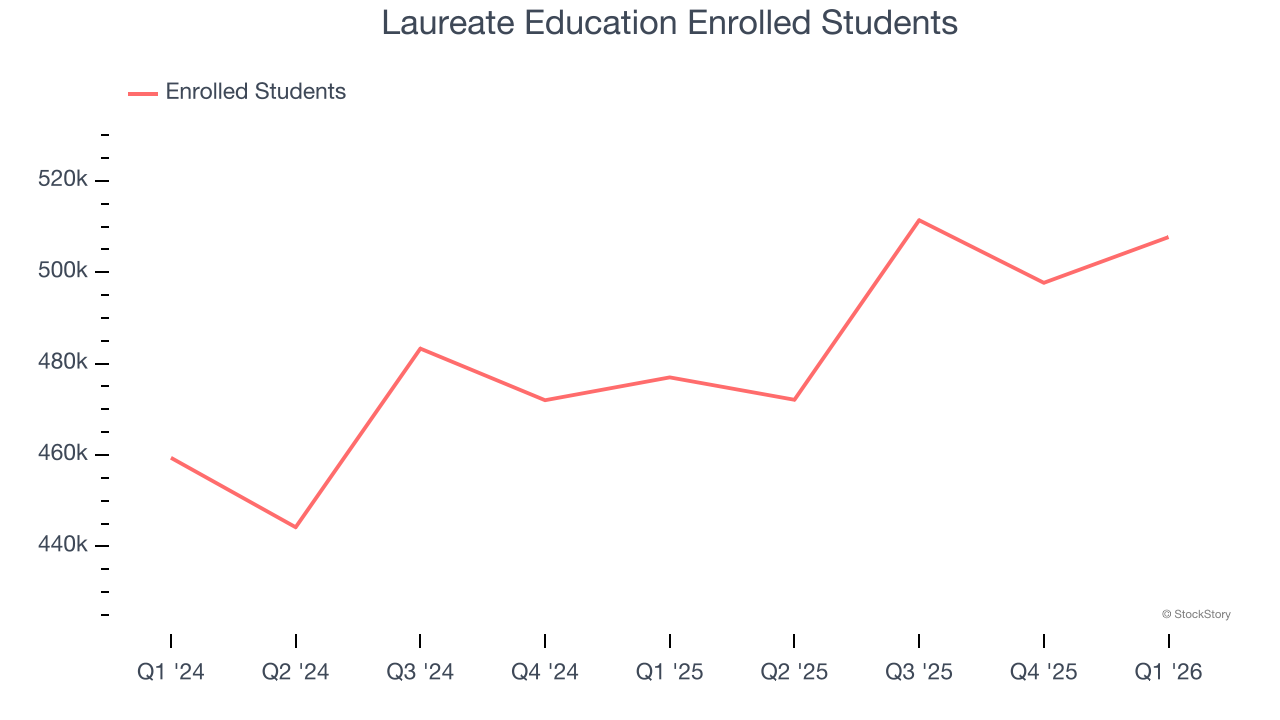

- Enrolled Students: up 30,700 year on year

- Market Capitalization: $4.42 billion

Eilif Serck-Hanssen, President and Chief Executive Officer, said “We are pleased to report favorable new enrollment results from the recently completed primary intake cycle in Peru and the secondary intake cycle in Mexico. Our operating trends remain on track with our expectations for the year. Additionally, we continue to return excess capital to shareholders, having completed approximately $105 million in share repurchases during the first quarter. As a result, we are increasing our full-year Adjusted Earnings Per Share guidance.”

Company Overview

Founded in 1998 by Douglas L. Becker and based in Miami, Laureate Education (NASDAQ: LAUR) is a global network of higher education institutions.

Revenue Growth

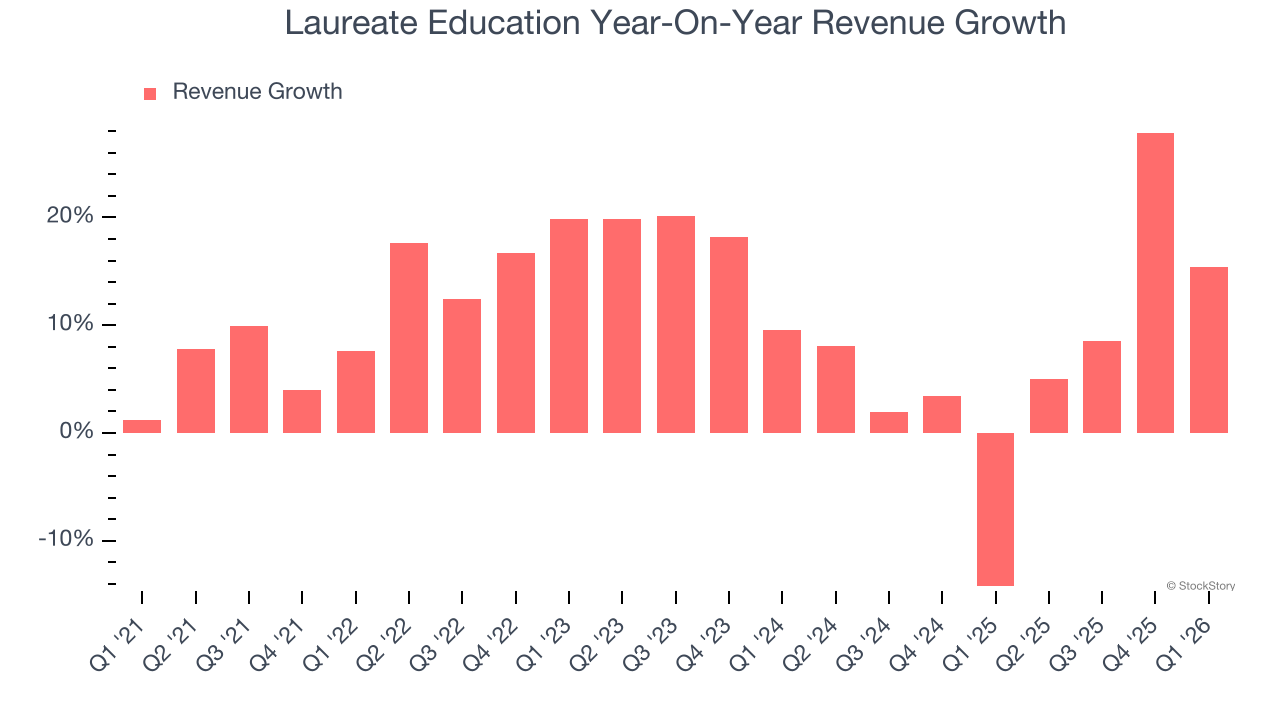

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Laureate Education grew its sales at a 11.1% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Laureate Education’s recent performance shows its demand has slowed as its annualized revenue growth of 7.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can dig further into the company’s revenue dynamics by analyzing its number of enrolled students, which reached 507,700 in the latest quarter. Over the last two years, Laureate Education’s enrolled students averaged 5.6% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Laureate Education reported year-on-year revenue growth of 15.4%, and its $272.6 million of revenue exceeded Wall Street’s estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 10.4% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Laureate Education’s operating margin has been trending up over the last 12 months and averaged 23.5% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

This quarter, Laureate Education generated an operating margin profit margin of negative 10.1%, down 4.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

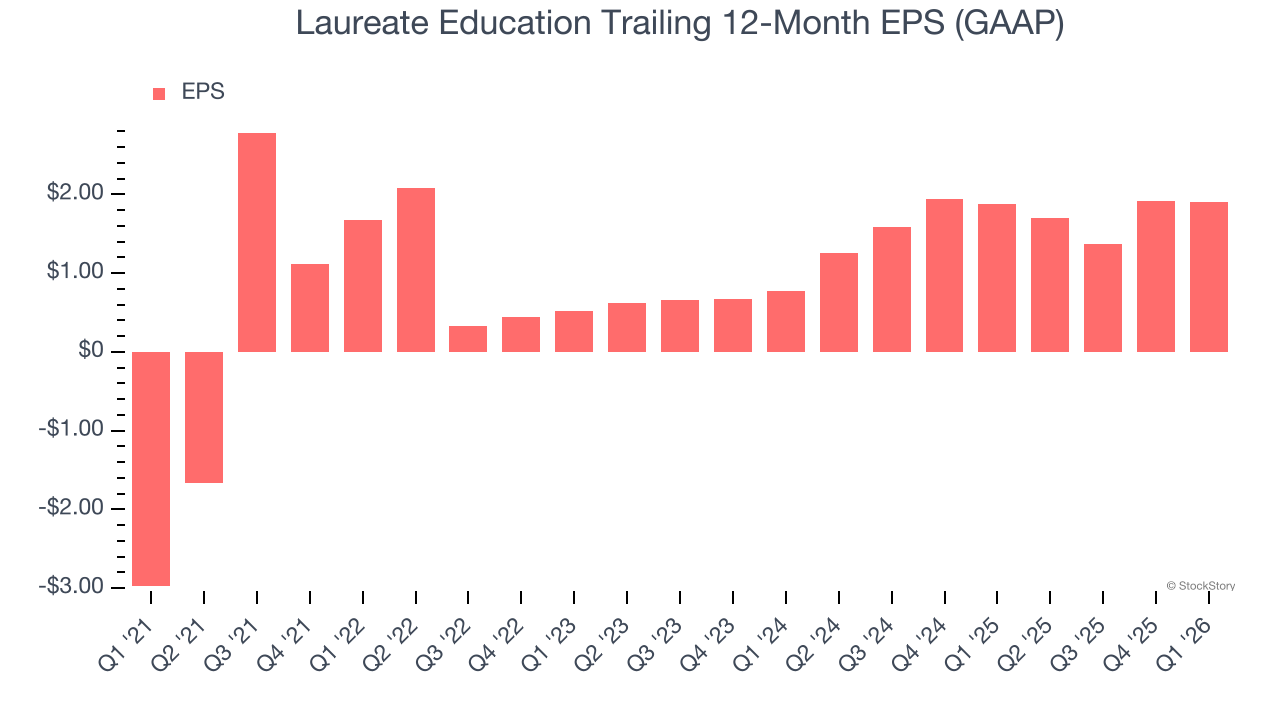

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Laureate Education’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Laureate Education reported EPS of negative $0.15, down from negative $0.13 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Laureate Education’s full-year EPS of $1.90 to grow 7.4%.

Key Takeaways from Laureate Education’s Q1 Results

It was good to see Laureate Education beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $31.59 immediately after reporting.

Is Laureate Education an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).