Packaging and materials company International Paper (NYSE: IP) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 1.2% year on year to $5.97 billion. Its non-GAAP profit of $0.15 per share was in line with analysts’ consensus estimates.

Is now the time to buy International Paper? Find out by accessing our full research report, it’s free.

International Paper (IP) Q1 CY2026 Highlights:

- Revenue: $5.97 billion vs analyst estimates of $5.93 billion (1.2% year-on-year growth, 0.7% beat)

- Adjusted EPS: $0.15 vs analyst estimates of $0.14 (in line)

- Adjusted EBITDA: $582 million vs analyst estimates of $686.7 million (9.7% margin, 15.2% miss)

- Operating Margin: 1.6%, up from -0.6% in the same quarter last year

- Free Cash Flow was $94 million, up from -$618 million in the same quarter last year

- Market Capitalization: $17.78 billion

Company Overview

Established in 1898, International Paper (NYSE: IP) produces containerboard, pulp, paper, and materials used in packaging and printing applications.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, International Paper’s 3.9% annualized revenue growth over the last five years was sluggish. This was below our standard for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. International Paper’s annualized revenue growth of 16.1% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

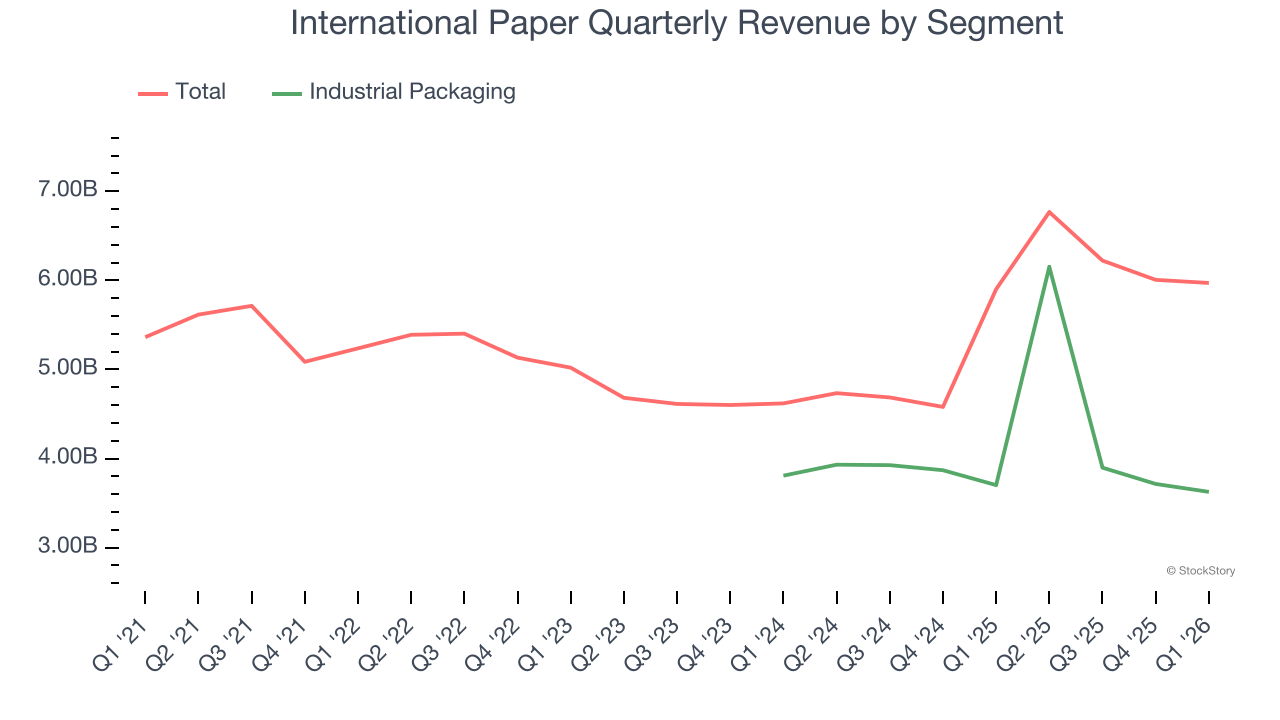

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Industrial Packaging. Over the last two years, International Paper’s Industrial Packaging revenue (containers, displays, bins) averaged 9.4% year-on-year growth. This segment has lagged the company’s overall sales.

This quarter, International Paper reported modest year-on-year revenue growth of 1.2% but beat Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

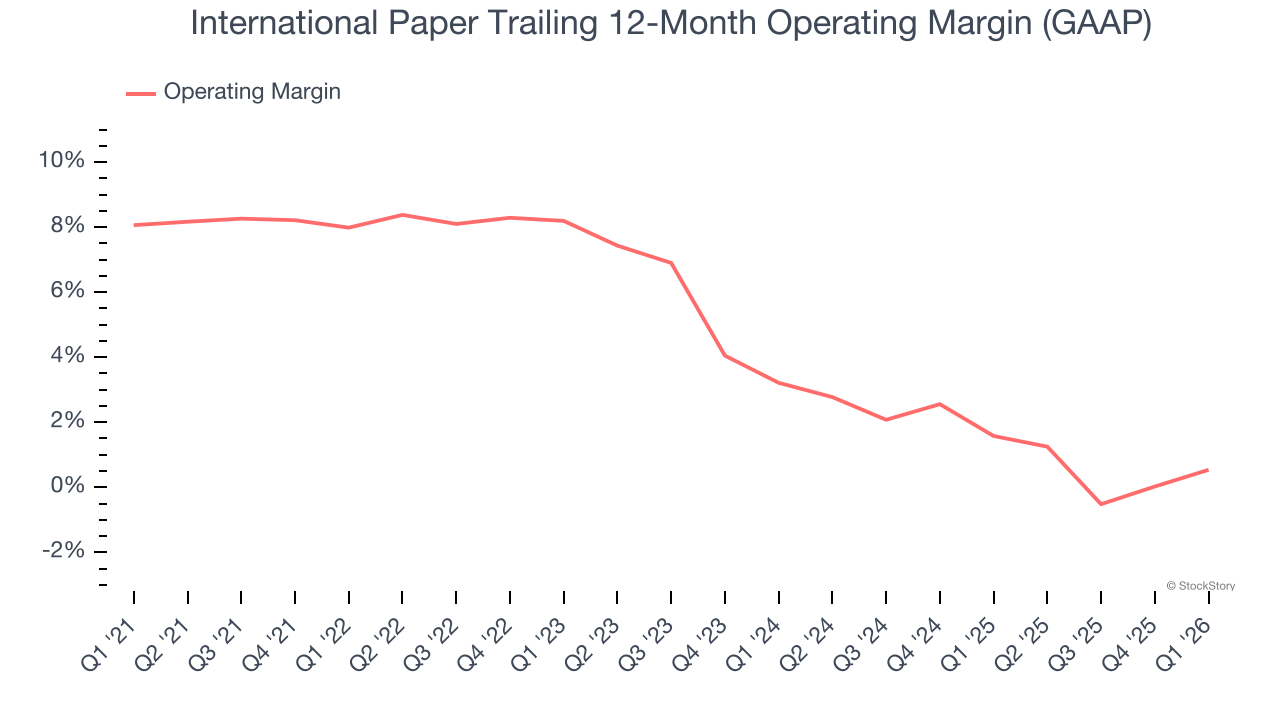

International Paper was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.2% was weak for an industrials business.

Analyzing the trend in its profitability, International Paper’s operating margin decreased by 7.4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. International Paper’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, International Paper generated an operating margin profit margin of 1.6%, up 2.2 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

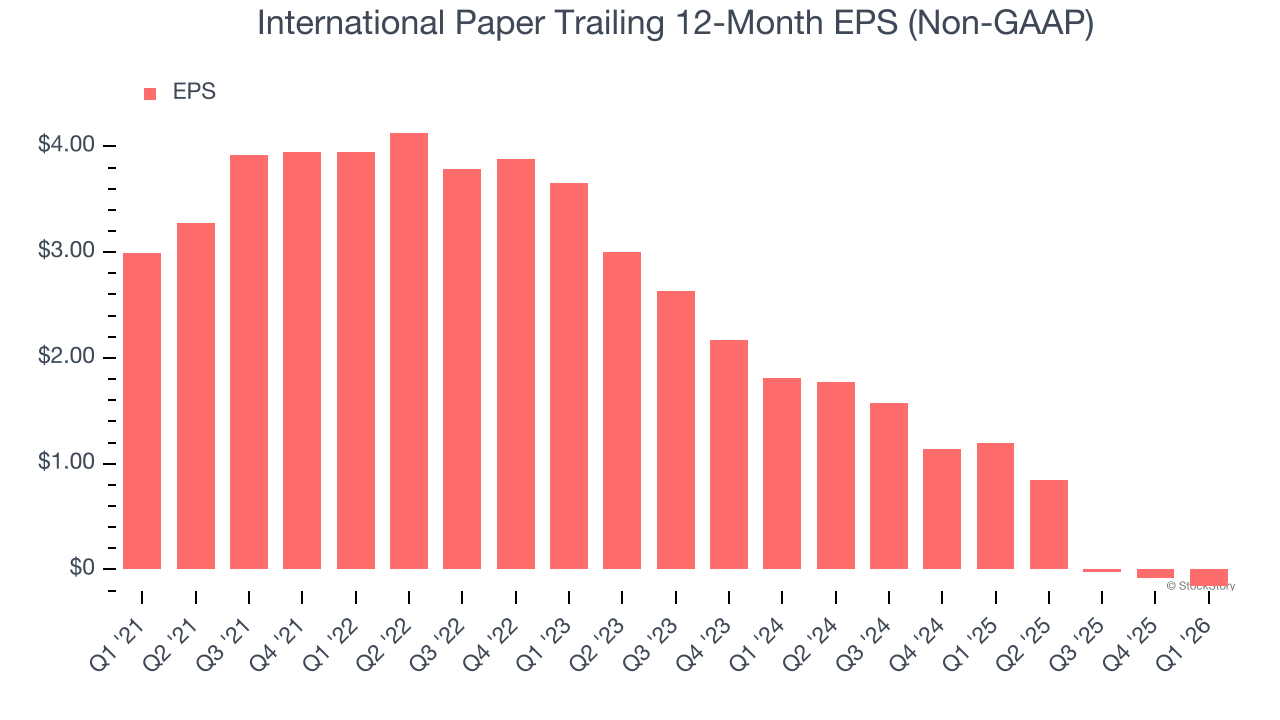

Sadly for International Paper, its EPS declined by 15.5% annually over the last five years while its revenue grew by 3.9%. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into International Paper’s earnings to better understand the drivers of its performance. As we mentioned earlier, International Paper’s operating margin expanded this quarter but declined by 7.4 percentage points over the last five years. Its share count also grew by 34.7%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For International Paper, its two-year annual EPS declines of 44.5% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q1, International Paper reported adjusted EPS of $0.15, down from $0.23 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 5.4%. Over the next 12 months, Wall Street is optimistic. Analysts forecast International Paper’s full-year EPS of negative $0.16 will flip to positive $1.93.

Key Takeaways from International Paper’s Q1 Results

It was encouraging to see International Paper meet analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.3% to $31.79 immediately after reporting.

International Paper may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).