Student loan servicer Navient (NASDAQ: NAVI) announced better-than-expected revenue in Q1 CY2026, but sales fell by 22.1% year on year to $152 million. Its GAAP profit of $0.18 per share was 17.4% above analysts’ consensus estimates.

Is now the time to buy Navient? Find out by accessing our full research report, it’s free.

Navient (NAVI) Q1 CY2026 Highlights:

- Net Interest Income: $131 million vs analyst estimates of $129 million

- Revenue: $152 million vs analyst estimates of $138.7 million (22.1% year-on-year decline, 9.6% beat)

- Pre-tax Profit: $32 million (21.1% margin)

- EPS (GAAP): $0.18 vs analyst estimates of $0.15 (17.4% beat)

- Market Capitalization: $861.9 million

Company Overview

Spun off from Sallie Mae in 2014 to handle the company's loan servicing and collection operations, Navient (NASDAQ: NAVI) provides education loan servicing and business processing solutions that help manage federal student loans, private education loans, and government services.

Revenue Growth

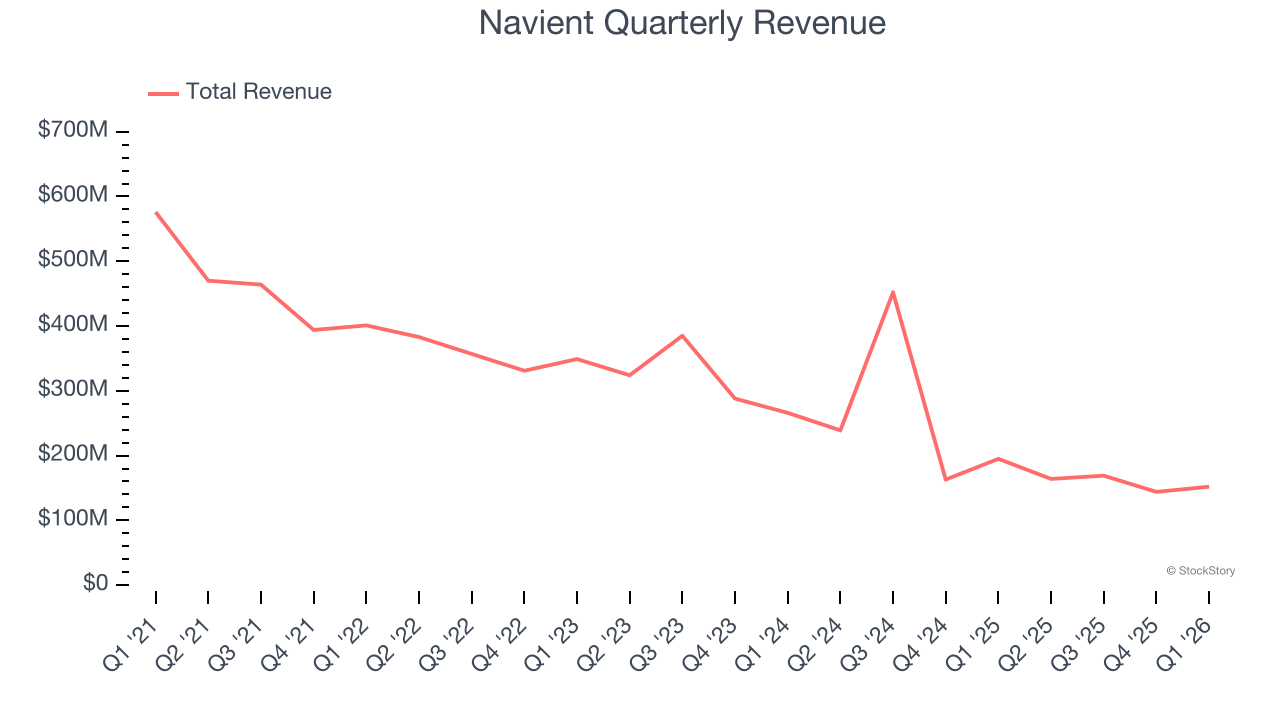

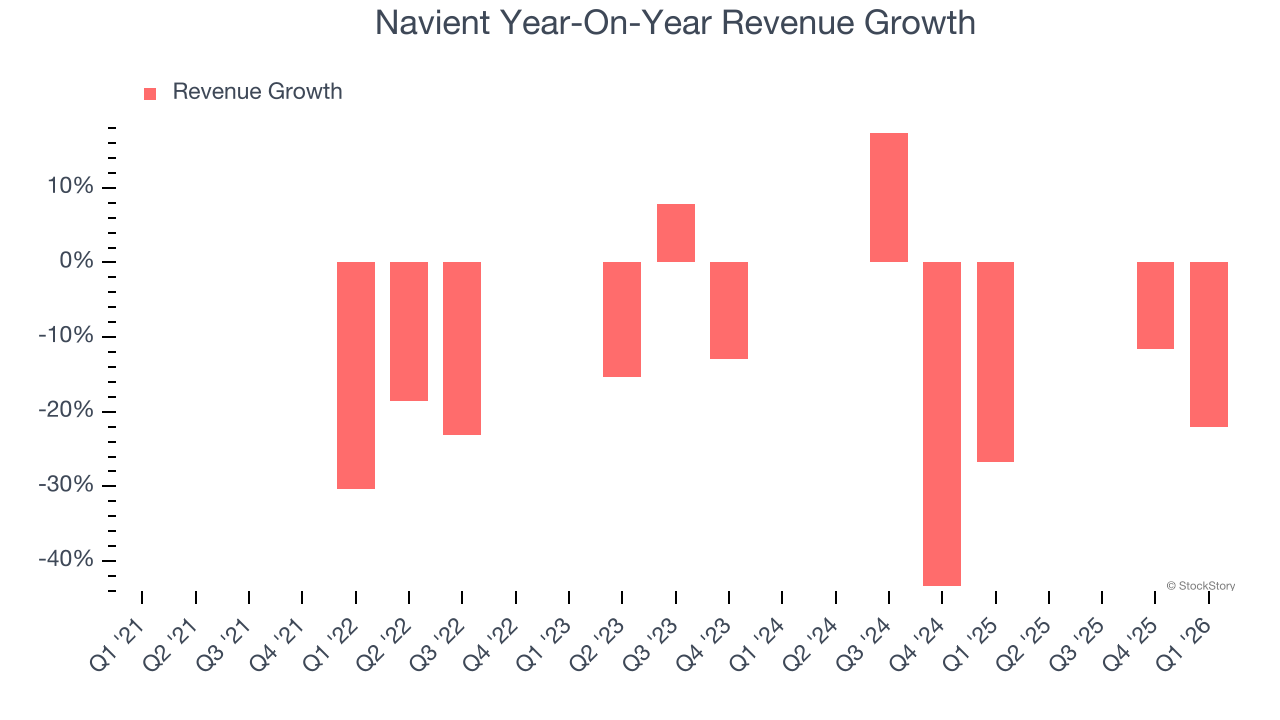

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Navient’s demand was weak over the last five years as its revenue fell at a 21.1% annual rate. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Navient’s recent performance shows its demand remained suppressed as its revenue has declined by 29.4% annually over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Navient’s revenue fell by 22.1% year on year to $152 million but beat Wall Street’s estimates by 9.6%.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Key Takeaways from Navient’s Q1 Results

We were impressed by how significantly Navient blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 3.3% to $9.48 immediately after reporting.

Navient may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).