As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the personal care industry, including Inter Parfums (NASDAQ: IPAR) and its peers.

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

The 11 personal care stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 0.9% while next quarter’s revenue guidance was 2.4% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 9.8% since the latest earnings results.

Inter Parfums (NASDAQ: IPAR)

With licenses to produce colognes and perfumes under brands such as Kate Spade, Van Cleef & Arpels, and Abercrombie & Fitch, Inter Parfums (NASDAQ: IPAR) manufactures and distributes fragrances worldwide.

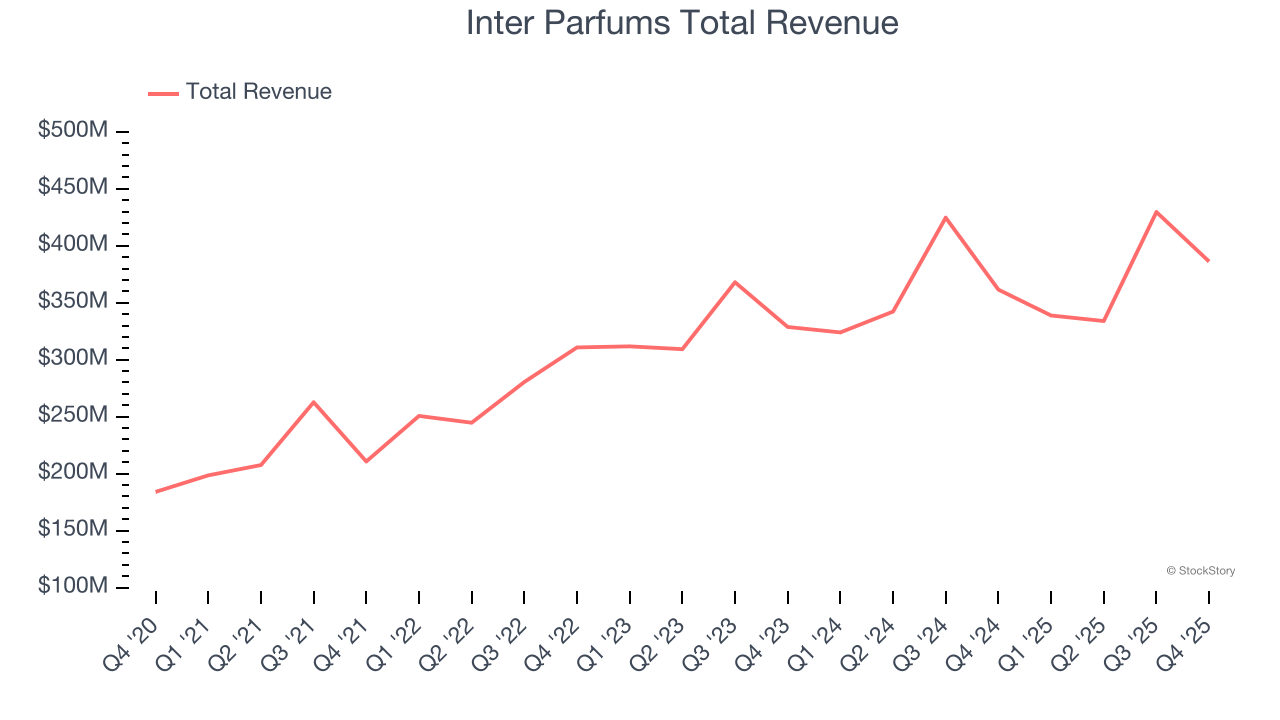

Inter Parfums reported revenues of $386.2 million, up 6.8% year on year. This print exceeded analysts’ expectations by 2.5%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ adjusted operating income estimates.

Inter Parfums delivered the weakest full-year guidance update of the whole group. The stock is down 11.8% since reporting and currently trades at $90.81.

Is now the time to buy Inter Parfums? Access our full analysis of the earnings results here, it’s free.

Best Q4: e.l.f. Beauty (NYSE: ELF)

Short for "eyes, lips, face", e.l.f. Beauty (NYSE: ELF) is a developer of high-quality beauty products at accessible price points.

e.l.f. Beauty reported revenues of $489.5 million, up 37.8% year on year, outperforming analysts’ expectations by 6.4%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

e.l.f. Beauty delivered the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 27.8% since reporting. It currently trades at $61.10.

Is now the time to buy e.l.f. Beauty? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Medifast (NYSE: MED)

Known for its Optavia program that combines portion-controlled meal replacements with coaching, Medifast (NYSE: MED) has a broad product portfolio of bars, snacks, drinks, and desserts for those looking to lose weight or consume healthier foods.

Medifast reported revenues of $75.1 million, down 36.9% year on year, exceeding analysts’ expectations by 5.2%. Still, it was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EPS guidance missing analysts’ expectations significantly.

Medifast delivered the highest full-year guidance raise but had the slowest revenue growth in the group. As expected, the stock is down 5.6% since the results and currently trades at $10.20.

Read our full analysis of Medifast’s results here.

Estée Lauder (NYSE: EL)

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE: EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

Estée Lauder reported revenues of $4.23 billion, up 5.6% year on year. This print met analysts’ expectations. Overall, it was a strong quarter as it also logged an impressive beat of analysts’ EBITDA estimates.

The stock is down 39.9% since reporting and currently trades at $71.91.

Read our full, actionable report on Estée Lauder here, it’s free.

Edgewell Personal Care (NYSE: EPC)

Boasting brands such as Banana Boat, Schick, and Skintimate, Edgewell Personal Care (NYSE: EPC) sells personal care products in the skin and sun care, shave, and feminine care categories.

Edgewell Personal Care reported revenues of $422.8 million, up 1.9% year on year. This result missed analysts’ expectations by 11.6%. Overall, it was a softer quarter as it also logged full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ revenue estimates.

Edgewell Personal Care had the weakest performance against analyst estimates among its peers. The stock is up 2.8% since reporting and currently trades at $21.34.

Read our full, actionable report on Edgewell Personal Care here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.