Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Carnival (NYSE: CCL) and the best and worst performers in the consumer discretionary - travel and vacation providers industry.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Travel and vacation providers operate tour packages, cruise lines, online travel agencies, and vacation rental platforms, connecting consumers with leisure and business travel experiences. Tailwinds include robust post-pandemic travel demand, a consumer preference shift toward experiences over goods, and technology-enabled personalization improving conversion and loyalty. However, headwinds are significant: the industry is acutely sensitive to macroeconomic cycles, geopolitical instability, and fuel price volatility. Low switching costs mean fierce price competition, while capacity additions in segments like cruises can lead to oversupply. Regulatory burdens, weather disruptions, and public health risks further create episodic but potentially severe demand shocks.

The 19 consumer discretionary - travel and vacation providers stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.7% while next quarter’s revenue guidance was 0.6% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.3% since the latest earnings results.

Carnival (NYSE: CCL)

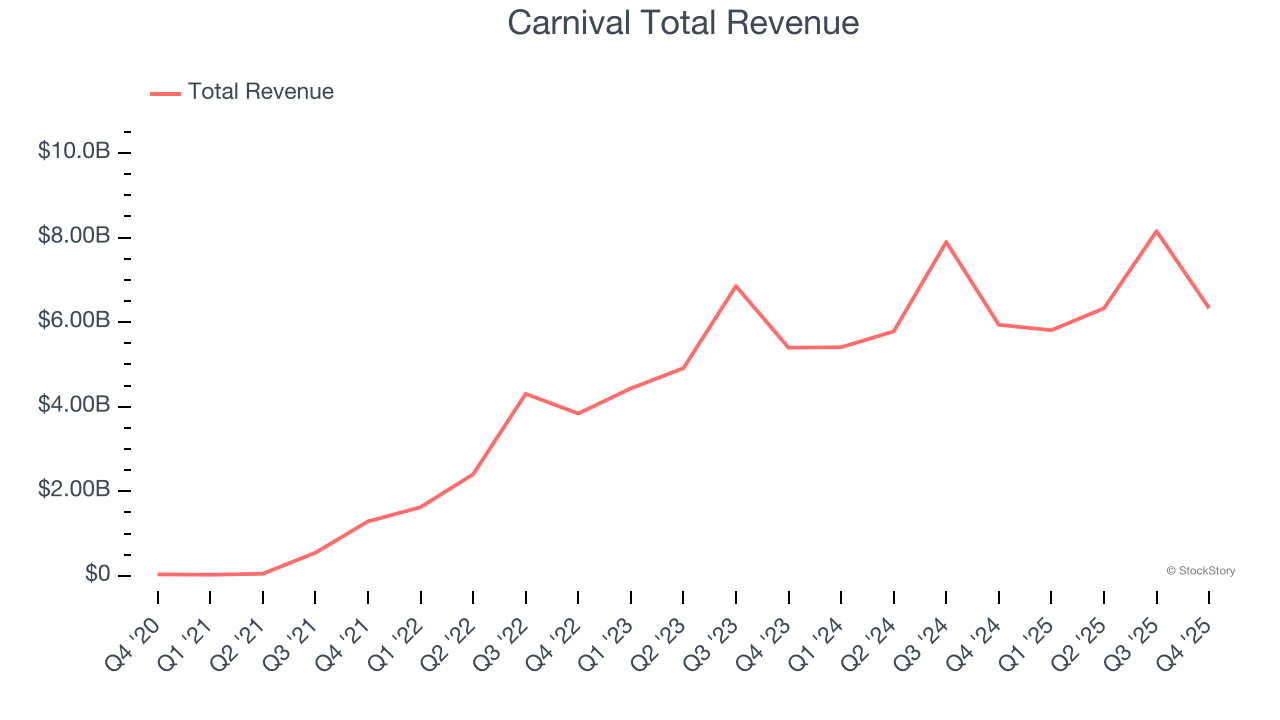

Boasting outrageous amenities like a planetarium on board its ships, Carnival (NYSE: CCL) is one of the world's largest leisure travel companies and a prominent player in the cruise industry.

Carnival reported revenues of $6.33 billion, up 6.6% year on year. This print fell short of analysts’ expectations by 0.6%, but it was still a strong quarter for the company with a beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

"2025 was a truly phenomenal year. We set new records across our business, achieved investment grade leverage metrics and, as announced just today, reinstated our dividend. These milestones reflect the collective strength of our cruise line portfolio and confidence in our long-term future," said Carnival Corporation & plc's Chief Executive Officer Josh Weinstein.

Unsurprisingly, the stock is down 13.6% since reporting and currently trades at $24.50.

Is now the time to buy Carnival? Access our full analysis of the earnings results here, it’s free.

Best Q4: Viking (NYSE: VIK)

From a single river cruise offering to a fleet of 96 vessels across multiple continents, Viking (NYSE: VIK) operates a fleet of small luxury cruise ships offering river, ocean, and expedition voyages focused on cultural enrichment and destination immersion.

Viking reported revenues of $1.72 billion, up 27.8% year on year, outperforming analysts’ expectations by 6.6%. The business had an exceptional quarter with a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Viking pulled off the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 7.3% since reporting. It currently trades at $68.60.

Is now the time to buy Viking? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Hilton Grand Vacations (NYSE: HGV)

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE: HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

Hilton Grand Vacations reported revenues of $1.33 billion, up 3.8% year on year, falling short of analysts’ expectations by 2.9%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates and a miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 17.2% since the results and currently trades at $40.24.

Read our full analysis of Hilton Grand Vacations’s results here.

Travel + Leisure (NYSE: TNL)

Formerly known as Wyndham Destinations, Travel + Leisure (NYSE: TNL) is a global vacation company that provides travelers with vacation ownership, exchange, and travel services.

Travel + Leisure reported revenues of $1.03 billion, up 5.7% year on year. This print beat analysts’ expectations by 3%. It was a strong quarter as it also produced EBITDA guidance for next quarter beating analysts’ expectations and a decent beat of analysts’ revenue estimates.

The stock is down 5.7% since reporting and currently trades at $68.73.

Read our full, actionable report on Travel + Leisure here, it’s free.

Marriott Vacations (NYSE: VAC)

Spun off from Marriott International in 1984, Marriott Vacations (NYSE: VAC) is a vacation company providing leisure experiences for travelers around the world.

Marriott Vacations reported revenues of $1.32 billion, flat year on year. This number surpassed analysts’ expectations by 2.1%. Taking a step back, it was a mixed quarter as it also recorded full-year EBITDA guidance topping analysts’ expectations but a significant miss of analysts’ adjusted operating income estimates.

The stock is up 22.6% since reporting and currently trades at $71.13.

Read our full, actionable report on Marriott Vacations here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.