Over the past six months, HCI Group’s shares (currently trading at $151.50) have posted a disappointing 16.9% loss while the S&P 500 was flat. This might have investors contemplating their next move.

Following the drawdown, is now an opportune time to buy HCI? Find out in our full research report, it’s free.

Why Are We Positive On HCI Group?

Starting as a Florida "take-out" insurer that assumed policies from the state-backed Citizens Property Insurance Corporation, HCI Group (NYSE: HCI) provides property and casualty insurance, primarily homeowners coverage, while leveraging proprietary technology to improve underwriting and claims processing.

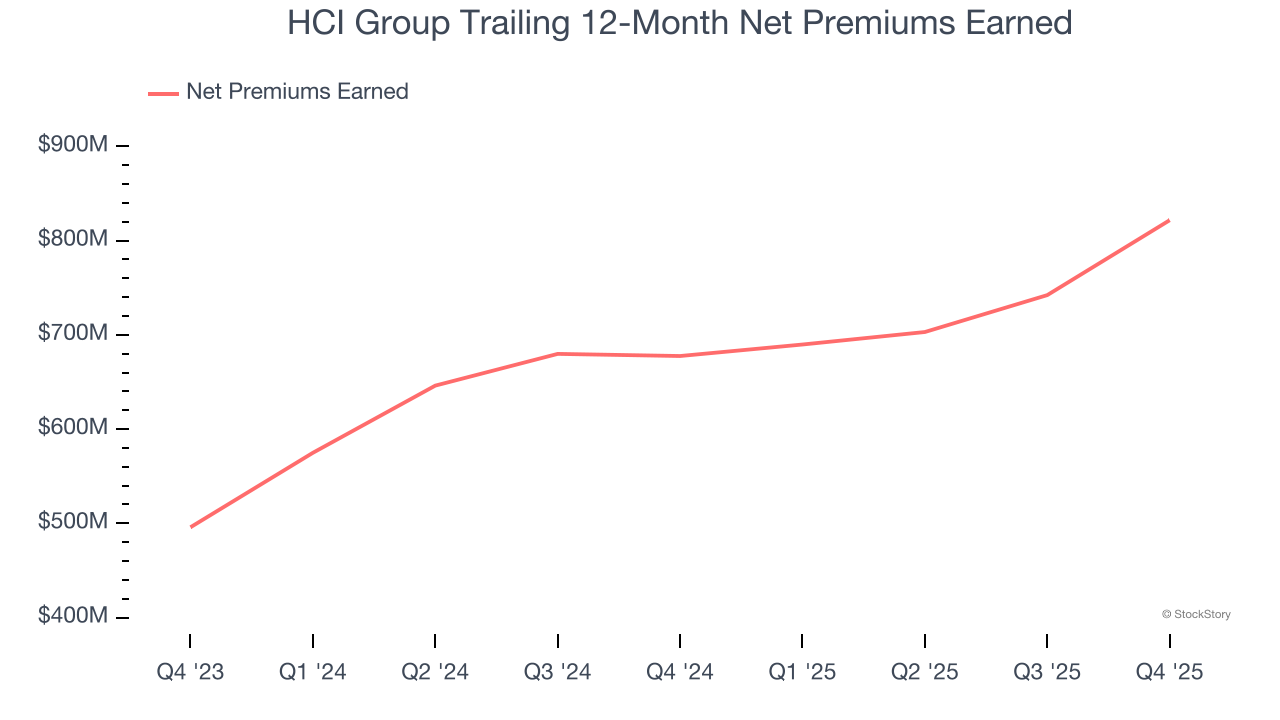

1. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

HCI Group’s net premiums earned has grown at a 28.7% annualized rate over the last two years, much better than the broader insurance industry and in line with its total revenue.

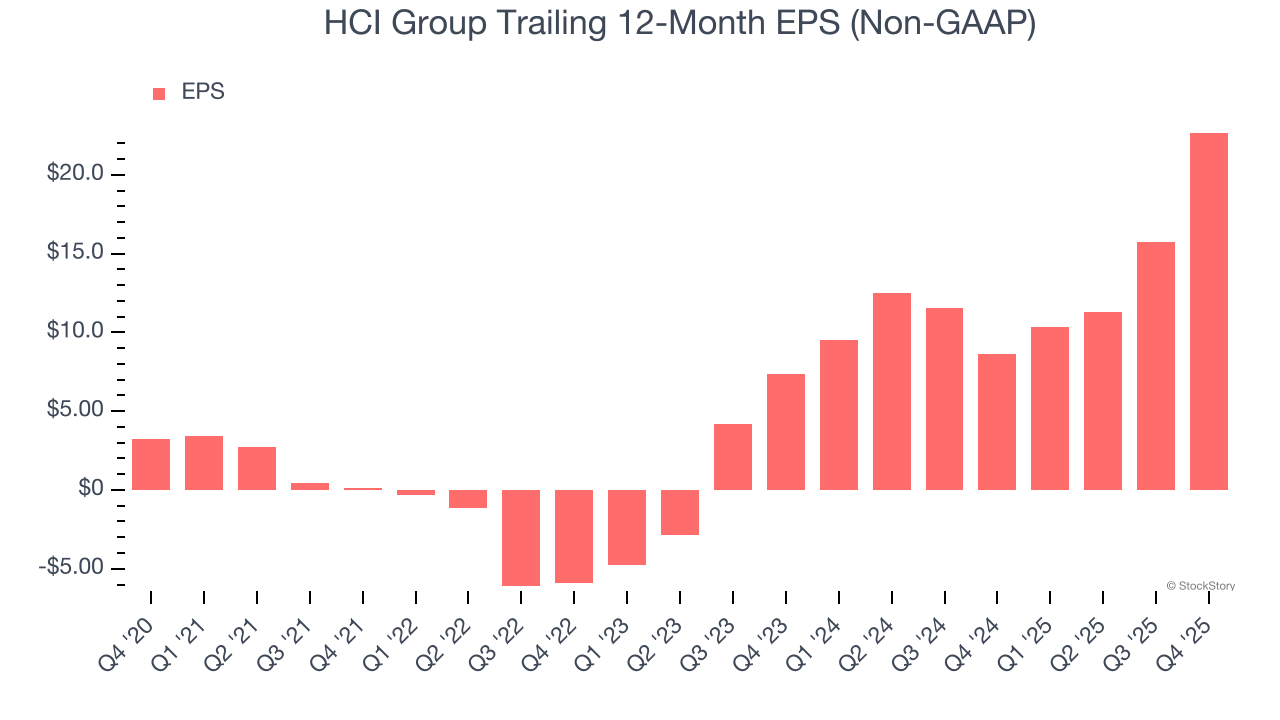

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

HCI Group’s EPS grew at 47.8% compounded annual growth rate over the last five years, higher than its 23.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

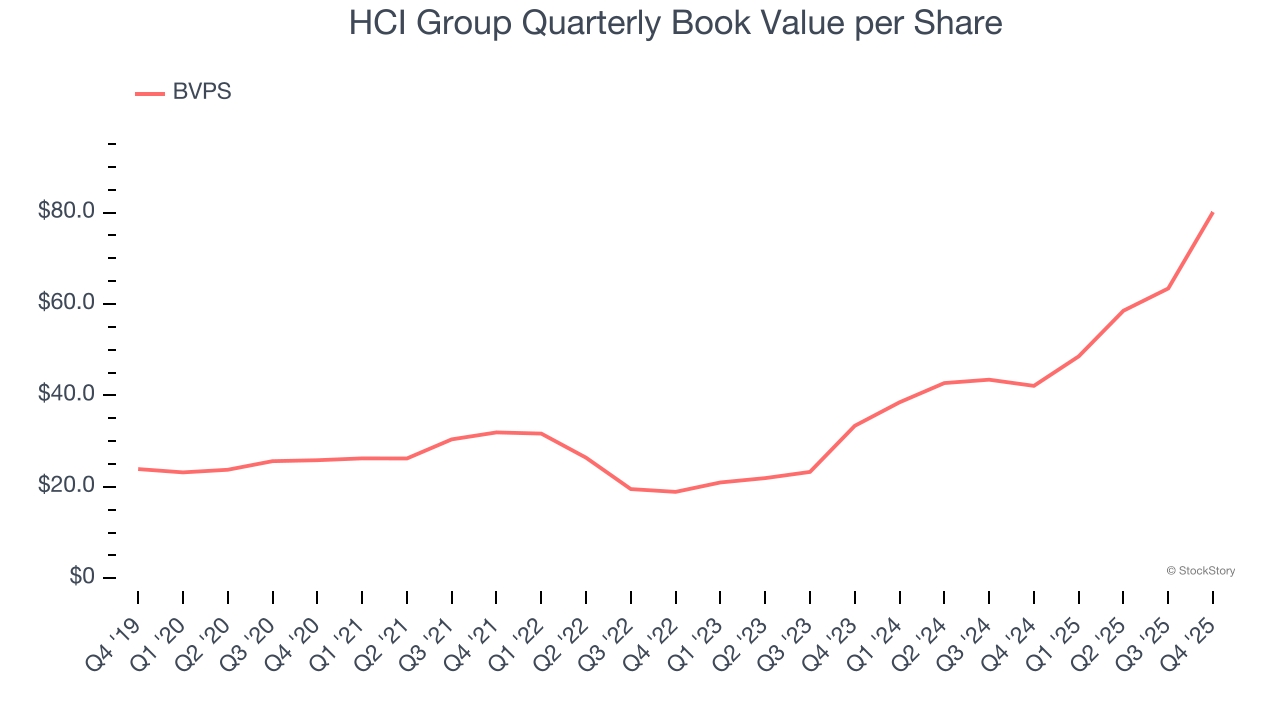

3. Growing BVPS Reflects Strong Asset Base

For insurers, book value per share (BVPS) is a vital measure of financial health, representing the total assets available to shareholders after accounting for all liabilities, including policyholder reserves and claims obligations.

HCI Group’s BVPS increased by 25.4% annually over the last five years, and growth has recently accelerated as BVPS grew at an incredible 55% annual clip over the past two years (from $33.36 to $80.13 per share).

Final Judgment

These are just a few reasons why we think HCI Group is an elite insurance company. After the recent drawdown, the stock trades at 1.7× forward P/B (or $151.50 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than HCI Group

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.