As the Q4 earnings season wraps, let’s dig into this quarter’s best and worst performers in the healthcare providers & services industry, including The Ensign Group (NASDAQ: ENSG) and its peers.

The healthcare providers and services sector, from insurers to hospitals, benefits from consistent demand, generating stable revenue through premiums and patient services. However, it faces challenges from high operational and labor costs, reimbursement pressures that squeeze margins, and regulatory uncertainty. Looking ahead, an aging population with more chronic diseases and a shift toward value-based care create tailwinds. Digitization via telehealth, data analytics, and personalized medicine offers new revenue streams. Nonetheless, headwinds persist, including clinical labor shortages, ongoing reimbursement cuts, and regulatory scrutiny over pricing and quality.

The 40 healthcare providers & services stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.6% since the latest earnings results.

The Ensign Group (NASDAQ: ENSG)

Founded in 1999 and named after a naval term for a flag-bearing ship, The Ensign Group (NASDAQ: ENSG) operates skilled nursing facilities, senior living communities, and rehabilitation services across 15 states, primarily serving high-acuity patients recovering from various medical conditions.

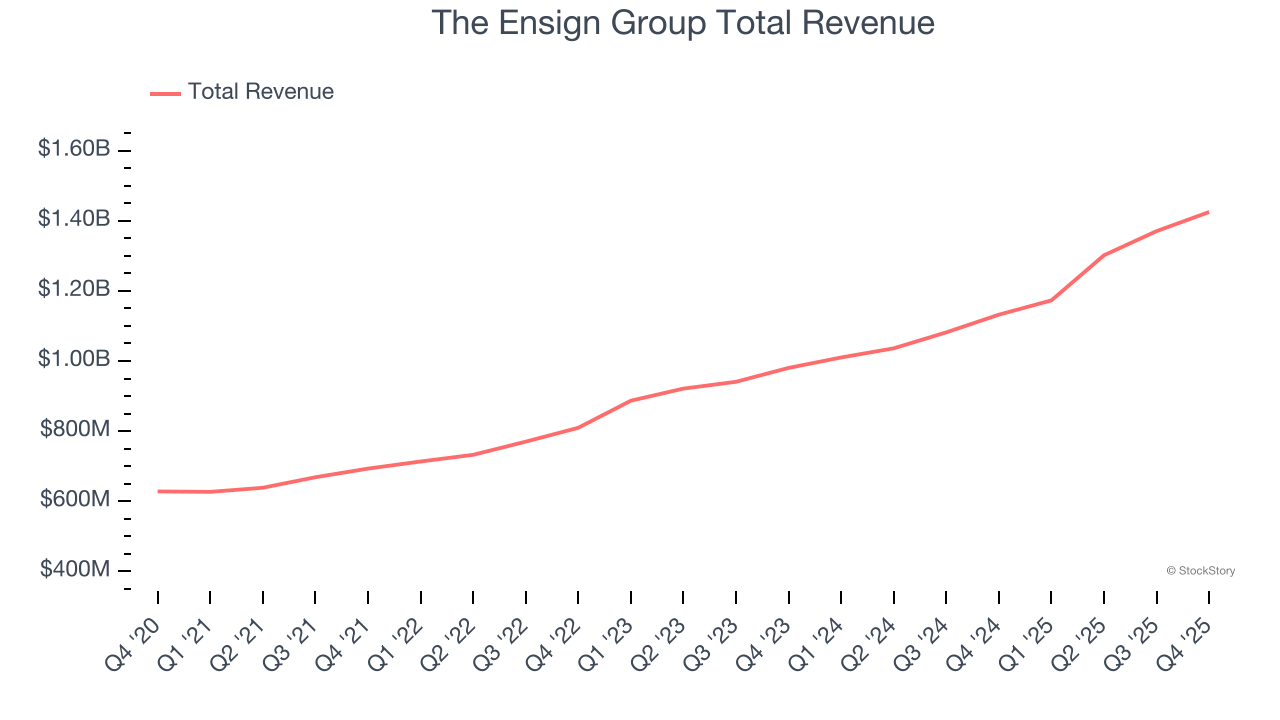

The Ensign Group reported revenues of $1.43 billion, up 25.9% year on year. This print fell short of analysts’ expectations by 4.8%. Overall, it was a mixed quarter for the company with an impressive beat of analysts’ full-year EPS guidance estimates but a significant miss of analysts’ revenue estimates.

“We are excited to report another record year and record quarter in several key areas. It’s difficult to convey in words how so many individuals work so hard and achieve such amazing outcomes through so many small moments of selfless service. None of the results are possible without the outstanding work being done by these amazing nurses, therapists, dieticians, food service professionals, activities coordinators and the many others whose unwavering commitment shapes the daily care experience for thousands of patients across our portfolio,” said Barry Port, Ensign’s Chief Executive Officer.

Interestingly, the stock is up 15.6% since reporting and currently trades at $200.16.

Is now the time to buy The Ensign Group? Access our full analysis of the earnings results here, it’s free.

Best Q4: RadNet (NASDAQ: RDNT)

With over 350 imaging facilities across seven states and a growing artificial intelligence division, RadNet (NASDAQ: RDNT) operates a network of outpatient diagnostic imaging centers across the United States, offering services like MRI, CT scans, PET scans, mammography, and X-rays.

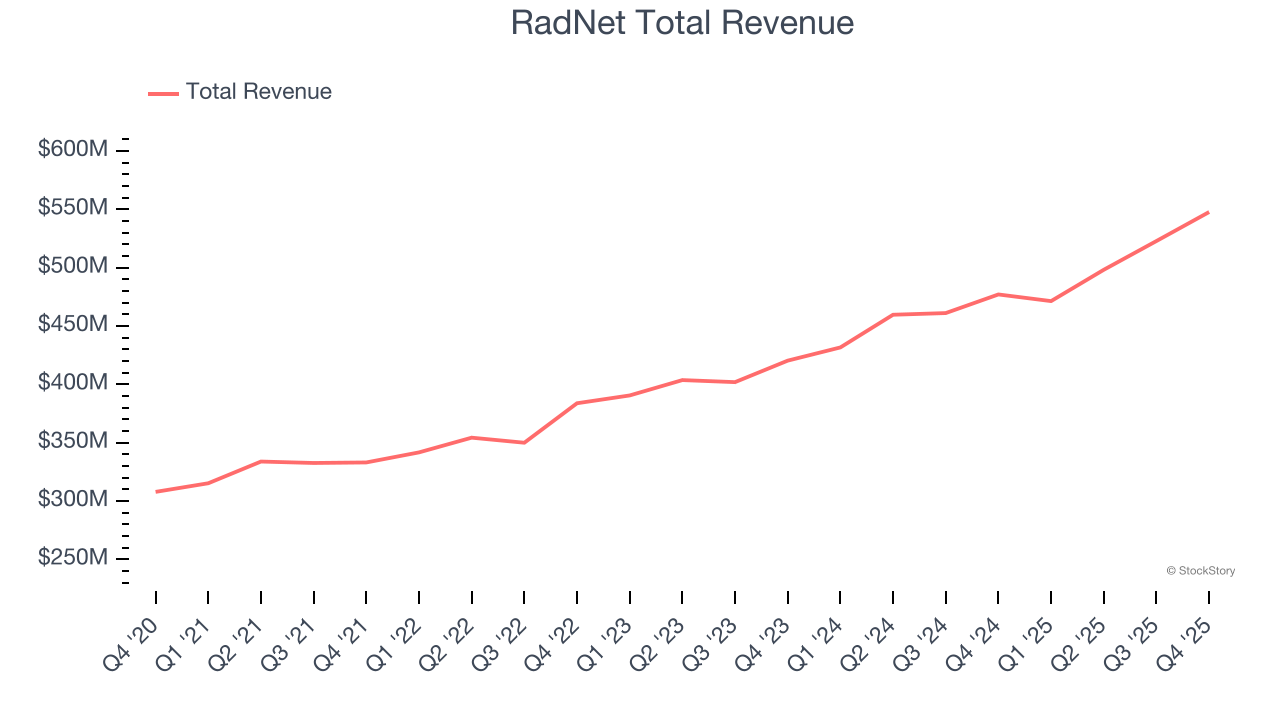

RadNet reported revenues of $547.7 million, up 14.8% year on year, outperforming analysts’ expectations by 5.8%. The business had an exceptional quarter with a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 12% since reporting. It currently trades at $61.41.

Is now the time to buy RadNet? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Chemed (NYSE: CHE)

With a unique business model combining end-of-life care and household services, Chemed (NYSE: CHE) operates two distinct businesses: VITAS, which provides hospice care for terminally ill patients, and Roto-Rooter, which offers plumbing and water restoration services.

Chemed reported revenues of $639.3 million, flat year on year, falling short of analysts’ expectations by 3%. It was a disappointing quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates and a significant miss of analysts’ revenue estimates.

As expected, the stock is down 19% since the results and currently trades at $377.95.

Read our full analysis of Chemed’s results here.

U.S. Physical Therapy (NYSE: USPH)

With a nationwide footprint spanning 671 clinics across 42 states, U.S. Physical Therapy (NYSE: USPH) operates a network of outpatient physical therapy clinics and provides industrial injury prevention services to employers across the United States.

U.S. Physical Therapy reported revenues of $202.7 million, up 12.3% year on year. This number beat analysts’ expectations by 1.7%. More broadly, it was a satisfactory quarter as it also recorded a decent beat of analysts’ revenue estimates but EPS in line with analysts’ estimates.

The stock is down 9.6% since reporting and currently trades at $73.83.

Read our full, actionable report on U.S. Physical Therapy here, it’s free.

Centene (NYSE: CNC)

Serving nearly 1 in 15 Americans through its government healthcare programs, Centene (NYSE: CNC) is a healthcare company that manages government-sponsored health insurance programs like Medicaid and Medicare for low-income and complex-needs populations.

Centene reported revenues of $49.73 billion, up 21.9% year on year. This print topped analysts’ expectations by 3%. Zooming out, it was a mixed quarter as it also produced a solid beat of analysts’ revenue estimates but full-year revenue guidance missing analysts’ expectations.

The company lost 334,600 customers and ended up with a total of 27.63 million. The stock is down 13.8% since reporting and currently trades at $34.42.

Read our full, actionable report on Centene here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.